Interest rates in Australia have been at a record low since 2021. The Reserve Bank of Australia (RBA) has kept the interest rates at 0.1% to address the high rate of unemployment and to provide relief to the economy. The RBA's decision to maintain low-interest rates has been criticised for fuelling a surge in property prices, enriching property owners, and making it difficult for younger generations to enter the property market. While low-interest rates make loans more affordable, they also result in lower yields from savings. The RBA has stated that it will maintain its low-interest rate policy until at least 2024, citing the absence of a rapid bounce-back in wages growth and low consumer confidence.

| Characteristics | Values |

|---|---|

| Interest rates in Australia | All-time low |

| Interest rate | 0.10% |

| Interest rate in September 1990 | 15.50% |

| Interest rate in March 2021 | 2.14% |

| Interest rate in November 2020 | 0.25% |

| Reason for low interest rates | To assist in addressing the high rate of unemployment, to support consumer confidence and to support higher employment |

| Drawback of low-interest rates | Little yield from savings |

| Advantage of low-interest rates | Cheaper loans |

Explore related products

What You'll Learn

![]()

The drawbacks of low-interest rates for savers

Interest rates in Australia are at a record low. The Reserve Bank of Australia decreased interest rates to an all-time low of 0.1% in November 2020. The bank aimed to address the high rate of unemployment and provide relief to the economy. The low-interest rates are expected to persist until at least 2024.

While low-interest rates have benefits, they also present drawbacks for savers. Here are some of the disadvantages of low-interest rates for savers:

- Reduced returns on savings: One of the most significant drawbacks of low-interest rates for savers is the reduced returns on their savings. The lower the interest rate, the less money savers will earn on their deposits. This can be particularly disadvantageous for those who rely on interest income, such as retirees or those with substantial savings. The reduced returns can impact their overall financial stability and ability to maintain or grow their wealth over time.

- Difficulty in finding high-yield savings accounts: In a low-interest-rate environment, it becomes more challenging for savers to find accounts with attractive interest rates. While some banks may still offer relatively higher rates, they often come with complicated terms and conditions. Savers may need to meet specific monthly criteria or deposit a minimum balance to qualify for these rates, making it less accessible for those with lower savings amounts or unpredictable cash flow.

- Encouragement to spend rather than save: Low-interest rates can discourage individuals from saving. With lower returns on savings accounts, people may be incentivized to spend their money on purchases or investments instead of keeping it in a savings account. This shift in behaviour can lead to a decrease in personal savings rates and potentially impact an individual's financial stability in the long run.

- Impact on savings strategies: The low-interest-rate environment may prompt savers to reconsider their savings strategies. Some individuals may choose to redirect a portion of their savings into alternative investment options, such as the stock market or property investments. While this can potentially lead to higher returns, it also carries greater risks. It may not be suitable for everyone, especially those with a low risk tolerance or limited knowledge of other investment options.

- Limited options for conservative investors: Low-interest rates can disproportionately affect conservative investors who prefer low-risk investment options. Traditional low-risk investments, such as savings accounts or fixed deposits, become less attractive due to the reduced returns. As a result, conservative investors may find it challenging to identify suitable investment opportunities that align with their risk appetite and provide satisfactory returns.

It is important to note that while low-interest rates can have drawbacks for savers, they are implemented to stimulate the economy and encourage spending. The Reserve Bank of Australia's decision to lower interest rates aims to address unemployment and support economic growth. Savers can consider seeking professional financial advice to navigate the low-interest-rate environment effectively and explore alternative options to grow their wealth.

Petunia Predators in Australia: Who's Eating My Flowers?

You may want to see also

Explore related products

$9.97 $19.95

![]()

The Reserve Bank of Australia's role in setting rates

The Reserve Bank of Australia (RBA) is Australia's central bank and banknote-issuing authority. It has had this role since 14 January 1960, when the Reserve Bank Act 1959 removed the central banking functions from the Commonwealth Bank. The RBA's primary role is to promote the economic prosperity and welfare of the people of Australia, both now and in the future.

The RBA's main policy role is to control inflation levels within a target range of 2–3%. This is done by controlling the unemployment rate according to the 'non-accelerating inflation rate of unemployment' (NAIRU). The NAIRU has been maintained at a target of 5–6% unemployment. The RBA also provides services to the Government of Australia and services to other central banks and official institutions.

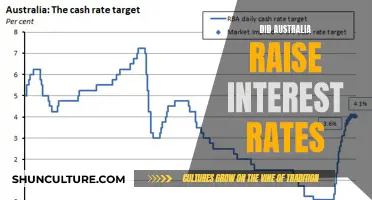

The RBA's interbank overnight cash rate target, which is the major influencer of retail interest rates, has surged from 0.1% in April 2022 to 4.1% in July 2023. The RBA aims to keep inflation low and stable, averaging 2-3%. However, it wants to do this while keeping the level of employment as high as possible. These outcomes are essential for a prosperous economy.

The RBA also contributes to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people. It promotes the efficiency and competitiveness of the payments system and regulates market infrastructure to support financial stability. The RBA works with other regulatory bodies to maintain the stability of the financial system to create favourable conditions to foster economic growth.

USA to Australia: Which Ocean Do Planes Fly Over?

You may want to see also

Explore related products

$9.59 $17.99

$10.32 $16.99

$26.09 $34.99

![]()

How interest rates affect mortgage repayments

Interest rates in Australia are currently at a record low, sitting at 0.1% as of November 2020. The Reserve Bank of Australia has implemented this low-interest rate to address the high rate of unemployment and support the economy in the wake of the pandemic. This low-interest rate environment has fuelled a surge in property prices, with many people taking out home loans to take advantage of the low rates.

In this low-interest rate environment, mortgage repayments are affected in several ways. Firstly, for those with existing variable-rate mortgages, their minimum repayment amounts may decrease. This is because the interest payable on the loan will decrease, resulting in lower monthly payments. However, it is important to note that banks may not always pass on the reduced interest rates to their customers, and some may choose to maintain their current rates.

On the other hand, for those with fixed-rate mortgages, their repayments will remain unchanged until the fixed-rate period ends. At that point, the mortgage will typically switch to the lender's standard variable rate (SVR), which may be higher or lower depending on the market interest rates at that time.

Low-interest rates also impact those considering taking out a new mortgage. With lower rates, the repayments on a home loan are more affordable, and borrowers may be able to pay off their loans faster or save money over time. This can make it an ideal time to buy a home, as borrowers can take advantage of the lower rates to secure a more favourable loan.

However, it is important to remember that interest rates may not stay low indefinitely. The Reserve Bank of Australia has indicated that low rates will likely remain until at least 2024, but economic factors could cause rates to rise sooner. As such, those considering taking out a new mortgage should be cautious and seek professional advice before making any decisions.

Exploring Slow Lorises: Are They Found in Australia?

You may want to see also

Explore related products

![]()

The impact of low-interest rates on the housing market

Interest rates in Australia have been at a record low since 2020, when the Reserve Bank of Australia (RBA) lowered them to 0.1%. The RBA's decision was aimed at addressing the high unemployment rate and providing relief to the economy. Low-interest rates make loans more affordable, encouraging people to borrow and spend, which supports consumer confidence and higher employment.

However, the impact on the housing market also depends on other factors, such as household income growth, population changes through immigration, and preferences for household sizes. Additionally, the supply of housing can be influenced by factors like construction constraints or labour force availability. These factors can lead to stronger demand or weaker supply, causing housing prices and rents to be less responsive to changes in interest rates.

The duration of low-interest rates also plays a role in their impact on housing prices. According to a model cited by the RBA, if interest rates were assumed to be 200 basis points higher forever, housing prices would be approximately 30% lower than if interest rates had remained unchanged. However, in reality, there are various factors influencing housing prices, and interest rates are just one piece of the puzzle.

In the context of Australia's housing market, low-interest rates have contributed to a surge in property prices. This dynamic has benefited existing homeowners, as rising property values increase household wealth. However, it has also made it more challenging for first-time homebuyers to enter the market, particularly if they have put their savings into riskier investments that have underperformed.

Additionally, economic uncertainty, such as that caused by Donald Trump's tariffs, can influence central banks' decisions to cut interest rates. While lower interest rates can support the housing market by making loans more affordable, uncertainty may also keep buyers cautious, especially those on the edge of affordability.

In summary, low-interest rates in Australia have had a significant impact on the housing market, contributing to rising property prices. This has created a two-fold effect, benefiting existing homeowners while making it more difficult for first-time buyers to enter the market. However, the impact of low-interest rates is just one factor influencing the complex dynamics of the housing market.

Virgin Australia Booking: Are Prices in AUD?

You may want to see also

Explore related products

$6.99

![]()

The relationship between interest rates and economic growth

Interest rates in Australia are at a record low as of 2021, with the Reserve Bank of Australia decreasing the interest rates to an all-time low of 0.1%. The reasons behind this decision include addressing high unemployment rates and providing relief to the economy in the face of economic uncertainty caused by the pandemic.

Additionally, interest rates are closely linked to inflation rates. Central banks often target a specific inflation rate, typically around 2%, to encourage economic growth while managing price increases. When inflation rises, central banks may increase interest rates to curb spending and slow down price growth. Conversely, during periods of low inflation or economic downturns, central banks may lower interest rates to stimulate the economy and increase borrowing, potentially leading to higher inflation.

Historically, economic growth has exceeded interest rates in the majority of years, particularly during periods of major wars due to increased government spending. However, there have also been times when interest rates have greatly exceeded economic growth, such as during the Great Depression, where interest rates remained positive even as the economy contracted.

In summary, the relationship between interest rates and economic growth is dynamic and subject to various factors, including consumer behaviour, inflation, business investments, and historical contexts. Interest rates play a crucial role in managing economic growth, with central banks utilising them as a tool to influence spending, borrowing, and inflation to achieve sustainable economic expansion.

Swallows' Diet in Australia: What Do They Eat?

You may want to see also

Frequently asked questions

Yes, interest rates in Australia are at a record low of 0.1% as of 2022. In March 2021, the interest rate was 0.25%, and in March 2020, it was 0.25% down from an already historic low.

The Reserve Bank of Australia (RBA) lowers interest rates to encourage people to borrow and spend, which supports consumer confidence and higher employment. The RBA has also started its own money-printing process (quantitative easing) to provide liquidity to Australian financial markets.

A lower interest rate means less money paid in interest, while a higher rate increases the overall cost of releasing home equity. The interest rate determines how much extra money borrowers must pay on top of the borrowed amount.