Australia's major banks have been quick to pass on interest rate hikes to their customers, but they have not passed on all the cuts since June 2019. This has resulted in increased profits for the banks and higher revenues, driven by the difference between the interest they earn on loans and the amount they pay to depositors. While the RBA's cash rate increases have been passed on to borrowers, the banks have not matched all the decreases, impacting households with large mortgages and causing them to pay a larger proportion of their income on debt servicing. With the cost of living and housing affordability becoming significant concerns, major banks are under pressure to pass on the RBA's rate cuts in full.

| Characteristics | Values |

|---|---|

| Big Australian banks passing on rate hikes | Yes |

| Big Australian banks passing on rate cuts | No |

| Number of big banks in Australia | 4 |

| Names of the big banks | ANZ, CBA, NAB, Westpac |

| Bank with the highest half-yearly net profit | National Australia Bank |

| Bank with the highest full-year net profit | Westpac |

| Average time taken to pass on rate hikes | 10-14 days |

| Average time taken to pass on rate cuts | Longer than rate hikes |

Explore related products

What You'll Learn

![]()

Banks are quick to pass on rate hikes

Australia's major banks have been quick to pass on interest rate hikes to their customers. Within minutes of the Reserve Bank of Australia (RBA) announcing interest rate cuts, the big banks were swift to declare that they would follow suit. However, it is important to note that the monthly savings on mortgage repayments were not immediate, and the big four banks took a more conservative approach, implementing the changes within a few weeks.

The big four Australian banks, including ANZ, CBA, NAB, and Westpac, have been in step with the RBA in raising interest rates. They have passed on all the rate hikes to their loan customers, contributing to their increasing revenues and profit margins. For instance, the net interest margin (NIM) has increased for both CBA and NAB, capturing the difference between interest earned on loans and the amount paid to depositors.

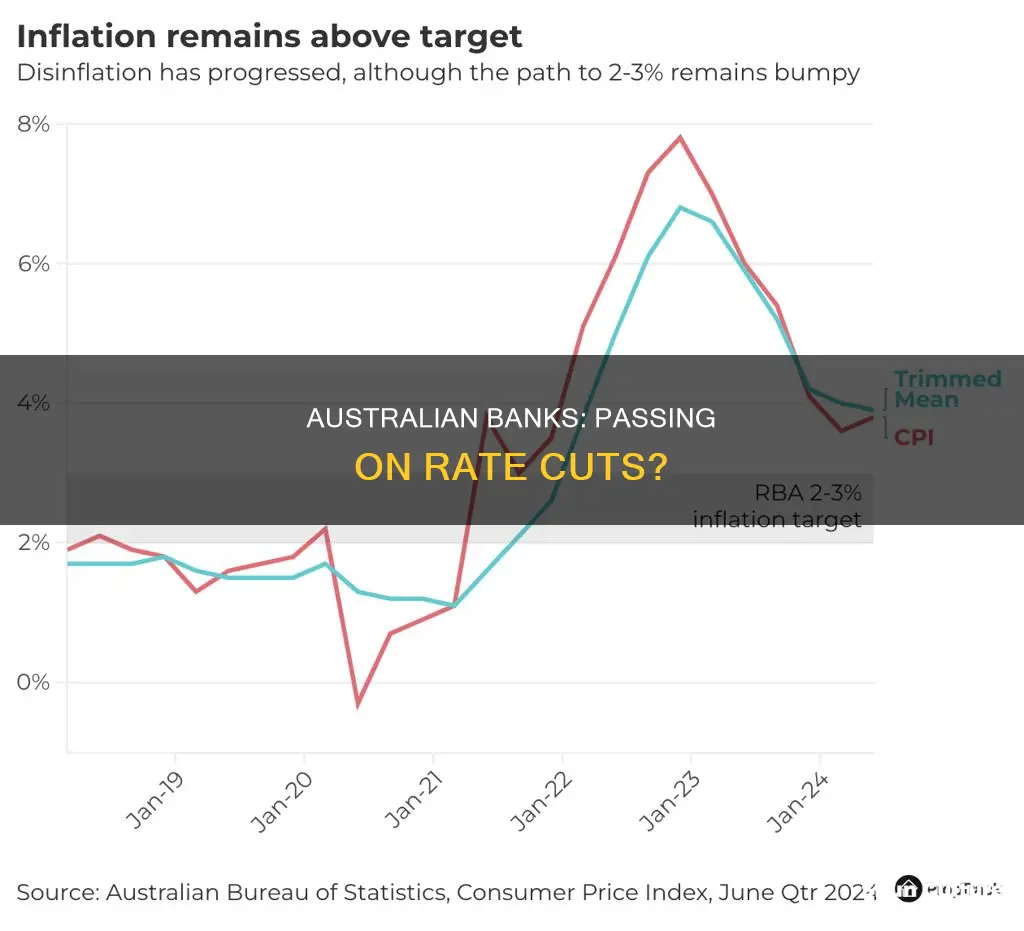

While the banks have promptly passed on the RBA's rate hikes, they have not matched all the decreases since June 2019. The RBA's cash rate has risen by 400 basis points, while the increase for deposits is around 300 basis points. This indicates that banks have only passed on three-quarters of the interest rate rises to depositors.

The delay in passing on rate cuts can be attributed to various factors, including the competition among banks and the impact on their profits. Banks are aware that customers will leave if they do not offer competitive lower rates in a timely manner. Additionally, when the cash rate decreases, banks have to pay less interest when borrowing from other banks, and they may delay passing on these savings to their customers for their own financial gain.

The full impact of rate increases on credit quality and the potential for renewed competition in the mortgage market are yet to be fully understood. While banks have profited from rapid interest rate hikes, many households have faced challenges due to rising mortgage rates, inflation-fuelled costs, and higher debt repayments.

Australian Dollars: 9 Pounds Conversion Mystery Explained

You may want to see also

Explore related products

![]()

But they don't pass on all cuts

Australia's big banks have been quick to pass on the Reserve Bank of Australia's rate increases, but they have not passed on all the cuts since June 2019. For instance, ANZ was the only major retail bank to cut its variable home loan rate in March 2020 as part of its Covid support package, but it did not pass on the full cut.

Data shows that the big banks do not automatically pass on reductions when the official rate is cut. The Australian Competition and Consumer Commission has launched an inquiry into how banks set interest rates for savers, as the recent rate rises have not been passed on in full to deposit accounts.

Banks are profiting from a period of rapid interest rate increases, with margins getting fatter and share prices rising. The difference between the interest they earn on loans and the amount they pay depositors, captured by the net interest margin, has increased.

While the RBA's cash rate has risen by 400 basis points, the increase for deposits is roughly 300 basis points. This is in line with previous phases of interest rate rises and compares favourably with New Zealand and the US, where the proportion passed by banks has been 50% and 35% respectively.

The delay in passing on rate cuts is not unusual, and historically, banks have taken even longer to implement lower rates, especially for mortgage borrowers. Banks have to pay less interest to borrow from other banks when the cash rate goes down, and they can pass those savings on to their customers. However, the process of rate cuts being passed on takes time, especially for bigger lenders.

US Dollars to Australian: How Much is 800 Bucks?

You may want to see also

Explore related products

![]()

The RBA's rate cuts are not passed on immediately

While the major banks in Australia have been quick to pass on the RBA's rate increases, they have not been as prompt with the decreases. Data from Canstar shows that the big banks do not automatically pass on reductions when the official rate is cut. ANZ was the only major retail bank to cut its variable home loan rate in March 2020 as part of its Covid support package, but even it did not pass on the full cut.

When the RBA announced a rate cut in February 2025, the major banks were quick to share that they would follow suit. However, the big four banks (ANZ, CBA, NAB, and Westpac) took a more conservative approach, stating that the changes would come into effect within a few weeks. This delay is not unusual, and historically, banks have taken even longer to implement lower rates, especially for mortgage borrowers.

The process of rate cuts being passed on takes time to flow through, especially for bigger lenders. Banks have to pay less interest when borrowing from other banks, and they can then pass those savings on to their customers. However, there is no requirement for banks to pass on interest rate cuts to their customers at all. The competitive nature of the industry does incentivize them to offer lower rates in a timely manner, or else customers may leave for another bank.

The RBA's next rate cut is expected to come after the federal election, and banks may be more reluctant to pass on any changes at that time.

Cheese Varieties Popular in Australia: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Banks' profits are impacted by rate cuts

Interest rate changes can significantly impact the profitability of banks. When interest rates rise, banks tend to profit more, as they can earn a higher yield on every dollar they invest. This is because banks make money by accepting cash deposits from customers and paying them interest, then investing that money elsewhere. The bank's profit is the difference between the interest they pay depositors and the yield they make through investing, so higher interest rates increase the yield on their investments.

However, interest rates can also go too high, causing businesses and consumers to hesitate to borrow, which negatively impacts the lending side of banking. Similarly, when interest rates are cut, banks' profits can be impacted as the profit from each loan will be lower, along with the amount the bank makes by investing in short-term debt securities.

Banks have massive cash holdings, and they invest a large portion of this cash in short-term Treasury securities. Even the very low interest rates that short-term Treasury notes yield are greater than the interest the banks pay to their customers. As rates fall, banks are seeing a decline in unrealized losses on their securities books. For example, when the Fed began hiking interest rates in 2022, U.S. banks' unrealized losses hit a peak of $690 billion, but as losses declined and the Fed cut rates in September, big banks sold low-rate securities and reinvested in higher-rate ones.

In Australia, the big banks have passed on all the interest rate hikes but not the cuts since June 2019. This has resulted in higher revenues and increased margins for the banks, while many households have felt the strain of rising mortgage rates and inflation-fuelled costs for food and electricity.

The Founding of Melbourne, Australia: A Historical Overview

You may want to see also

Explore related products

![]()

Household finances are squeezed by higher rates

Household finances in Australia are being squeezed by higher interest rates. The country's big banks have been in step with the Reserve Bank in raising interest rates, but they have not passed on all the cuts since June 2019. This has resulted in higher revenues for the banks, with margins getting fatter and share prices rising.

The share of household disposable income going towards debt repayments has increased from 7% to almost 10% in the past 17 months. This has been driven by rising mortgage rates and inflation-fuelled costs for food and electricity. Many borrowers have had to cut back on spending to meet higher mortgage payments, while also dealing with rising living costs.

The impact of higher interest rates on household finances is twofold. Firstly, higher interest rates increase the cost of borrowing, which reduces household spending. Secondly, higher interest rates can slow demand in the economy, which can help lower inflation. However, it is still unclear whether inflation is falling fast enough to get back to the Reserve Bank of Australia's target band within a tolerable timeframe.

While banks are not required to pass on interest rate cuts to their customers, they have been quick to pass on rate hikes to their variable mortgage customers. This has resulted in higher mortgage rates for borrowers, contributing to the squeeze on household finances. Overall, the combination of higher interest rates, rising living costs, and slow wage growth has put a strain on household finances in Australia.

Best Stopover Cities for Your Australia Trip

You may want to see also

Frequently asked questions

No, major Australian banks are not passing on all the rate cuts. While they have been quick to pass on the RBA's rate increases, they have not matched all the decreases since June 2019.

The delay in passing on rate cuts is not unusual, and historically, banks have taken even longer to implement lower rates, especially to mortgage borrowers. Banks are not obligated to pass on interest rate cuts to their customers. However, if they don't offer competitive lower rates, they risk losing customers to other banks.

The "big four" Australian banks, ANZ, CBA, NAB, and Westpac, have been criticized for delaying the passing on of rate cuts to their customers.