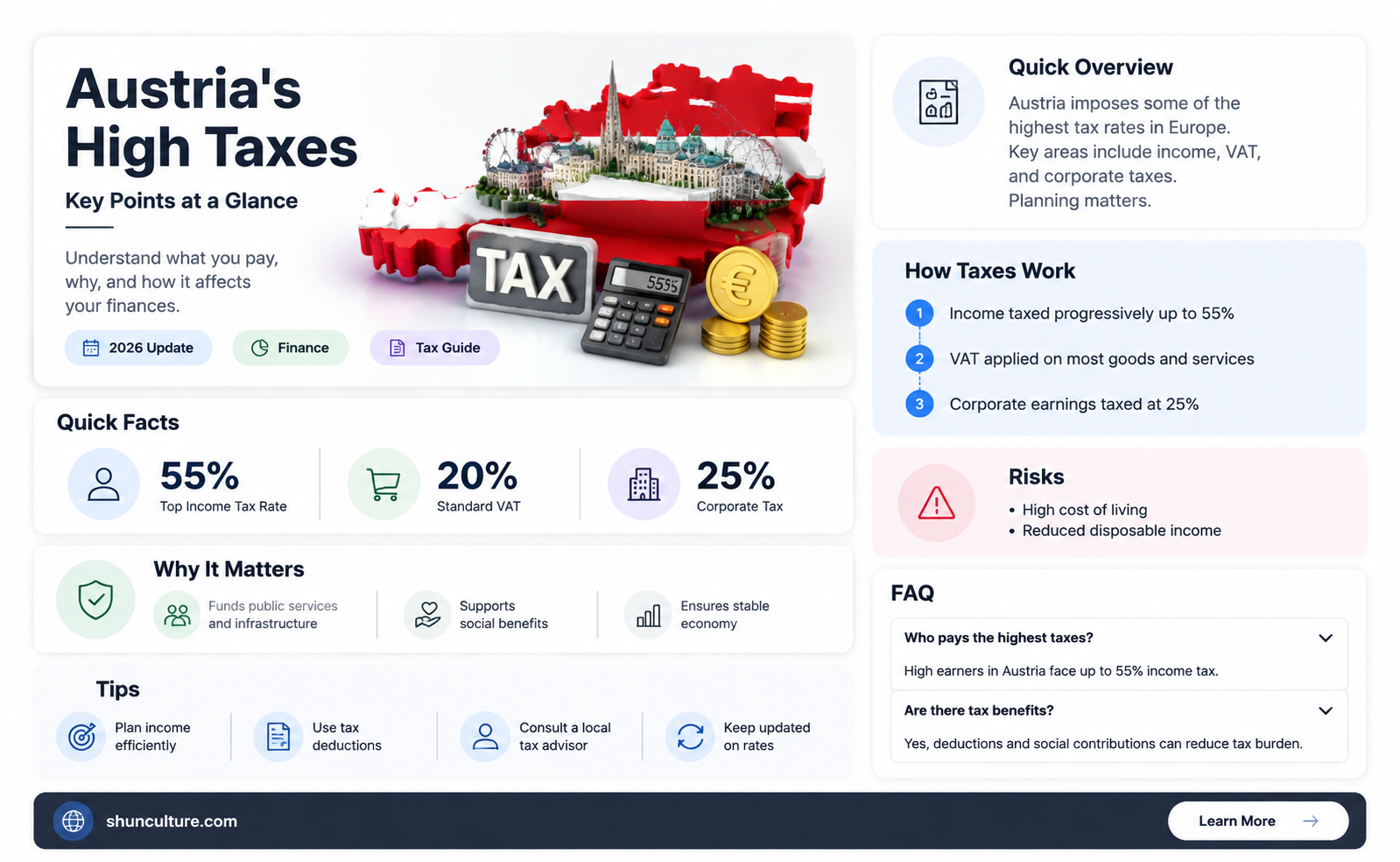

Austria has a progressive tax system, with rates ranging from 20% to 55% of earnings. The country has one of the highest personal income tax rates in Europe, with a marginal income tax rate of 55% for earnings over €1 million. This high marginal tax rate can disincentivize individuals from earning more or cause them to relocate to lower-tax regions. Austria's tax system includes income tax, corporate tax, value-added tax, and various other specific taxes. Understanding the country's tax system is crucial for individuals and businesses to ensure compliance and effectively manage their tax obligations.

| Characteristics | Values |

|---|---|

| Income tax | 20-55% of earnings |

| Corporate tax | 24% in 2023, 23% in 2024 |

| Value-added tax | 20% standard rate, 10% or 13% reduced rate |

| Municipal tax | 3% of employees' gross salary |

| Capital gains tax | 25% |

| Real estate transfer tax | 3.5% of the acquisition price or property value |

| Vehicle tax | Based on vehicle weight and type |

| Inheritance and gift tax | Abolished in 2008 |

| Digital services tax | 5% on revenues exceeding €25 million from online advertising services |

Explore related products

What You'll Learn

![]()

Income tax

Austria has a progressive income tax system, with rates ranging from 20% to 55% of taxable income. The more you earn, the higher the rate of taxation. Austria's income tax system has seven fare zones, and those who earn less than €11,000 annually are exempt from paying any tax. The highest marginal tax rate of 55% is for individuals with an annual income of over €1 million. This is one of the highest top marginal income tax rates in Europe.

The income tax in Austria is based on worldwide income. This means that individuals with residence or habitual residence in Austria are taxed on all of their income, whether it is from sources inside or outside the country. Even some income can be taxed if the person is not a resident of Austria.

The 13th and 14th-month salaries are considered 'special payments' and are subject to social security deductions. The first €620 is tax-exempt, and the remaining amount is taxed at a graduated rate between 6% and 55%.

It is important to note that income tax liability in Austria is not dependent on whether an individual is self-employed or an employee. Employees have income tax automatically deducted and paid by their employer to the tax authority every month. On the other hand, self-employed individuals pay income tax themselves as part of their annual income tax return.

In Austria, salaried employees and pensioners pay wage tax (Lohnsteuer), while self-employed workers fall under income tax (Einkommensteuer). However, the tax brackets for both groups are the same. As a freelancer, individuals can expect to pay a tax rate of about 25% if their income surpasses the tax-free threshold of €12,465.

Austria's income tax system is intended to fund public expenses, such as new roads, swimming pools, and social services. The tax revenue is distributed to public and social services to create a high standard of living for residents.

English in Austria: Is It Widely Spoken?

You may want to see also

Explore related products

![]()

Corporate tax

Corporate income tax (CIT) in Austria is levied on the profits of corporations. The tax rate for corporate income tax in Austria is currently 24% of taxable income, regardless of the amount of income. This rate has been reduced from 25% in 2022, and the Austrian government plans to further reduce it to 23% in 2024. Austrian limited liability companies (GmbH) and stock companies (AG) are subject to this corporate income tax.

Corporations with their management or registered office in Austria are subject to unlimited corporate income tax. This means their total income, regardless of whether it is obtained in Austria or abroad, is taxable. On the other hand, corporations without either their management or registered office in Austria are subject to limited corporate income tax, which covers only certain domestic revenues.

There is a minimum corporate income tax that must be paid. For companies with share capital subject to unlimited tax liability, the minimum tax level is five per cent of one quarter of the statutory minimum level of the nominal or share capital for each full calendar quarter. Additionally, there is a minimum CIT payable by companies in a tax-loss position, which can be carried forward without time limitation and credited against future CIT burdens.

Dividends, interest income, and capital gains are treated differently for corporate income tax purposes in Austria. Dividends from certain types of companies, such as Austrian, EU, and comparable foreign companies, are generally exempt from corporate income tax unless specific conditions are met. Interest income is subject to a 25% corporate income tax, while interest expenses are deductible with certain limitations. Capital gains from the sale of participations in specific companies may also be exempt from corporate income tax if certain conditions are met.

Overall, Austria's corporate income tax rate is relatively standard when compared to other countries, and the country ranks 15th overall on the 2024 International Tax Competitiveness Index.

Austria: Safe Haven for American Tourists?

You may want to see also

Explore related products

![]()

Value-added tax

In Austria, all companies with an annual turnover of more than €35,000 are subject to VAT. Small businesses with an annual turnover of less than €35,000 are exempt from VAT and do not have to charge it on their goods and services. However, they also cannot claim input tax deductions.

The ultimate burden of VAT falls on the final retail consumer. Exports and certain services for foreign customers are exempt from VAT. Import transactions from non-EC countries are subject to an import turnover tax at the same rate as VAT.

Businesses that are VAT-registered in Austria must use the correct VAT rates when supplying goods and services and are held liable for any unbilled VAT. This includes invoicing customers correctly according to Austrian time of supply VAT rules. The tax point (time of supply) rules in Austria determine when the VAT is due, which is then payable to the tax authorities 10 days after the VAT reporting period ends (monthly or quarterly).

Central Powers: Germany and Austria-Hungary's Alliance Legacy

You may want to see also

Explore related products

![]()

Municipal tax

In Austria, municipal tax is an exclusively local levy. Businesses pay municipal tax to the municipality in which they are located. The municipal tax amounts to 3% of the tax base, which is the total wages paid to employees of a permanent business establishment in a calendar month.

Enterprises that pay wages to employees at a permanent business establishment located in Austria are subject to municipal tax in any municipality in which the company has a permanent business establishment. In this context, enterprises are defined as those who independently carry out commercial or professional activity.

Public bodies are only considered commercial or professionally active in the context of their commercial operations and their agricultural and forestry operations.

Some organisations are exempt from municipal tax. These include:

- Austrian Federal Railways and private railways (with 66% tax base)

- Corporations, associations of persons or assets, provided that they are run for charitable and/or not-for-profit purposes in the healthcare sector, or for the benefit of children, young people, families, the sick, the disabled, the blind or the elderly.

In Vienna, an employer tax must also be paid in addition to the municipal tax charge.

Earthquakes in Austria: A Rare Occurrence?

You may want to see also

Explore related products

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)

![]()

Real-estate tax

Austria's real-estate tax is an object tax on property in Austria. It is collected by municipalities in accordance with federal law, who keep the revenue from this tax in its entirety. The real-estate tax base is determined by the Tax Authority Austria, which applies a tax measurement figure to the unit value. This is then transmitted to the municipalities, who apply assessment rates to calculate the annual amount of real estate tax.

The owner of the property is liable for the real estate tax, but it can be charged (pro rata) to renters as part of the running costs of a house. The tax is collected in four instalments on 15 February, 15 May, 15 August, and 15 November if it exceeds 75 Euros per year. Amounts up to 75 Euros must be paid once a year on 15 May.

The real-estate tax distinguishes between agricultural and forestry assets and real estate assets. There are also exemptions for public transport routes, watercourses, and properties belonging to public authorities for public service or public use. Temporary exemptions can also be granted by municipalities for newly created (subsidised) residential properties.

When buying a house or apartment in Austria, various taxes, fees, and commissions must be paid. This includes a real estate transfer tax, a real estate title registration duty, and a land acquisition tax. The value-added tax on real estate is 20%.

Austria also imposes a land tax called "Grundsteuer", which is quite low for apartments (100 Euros per year) and is included in the monthly bills. For houses, this tax depends on the cadastral purpose and actual use of the land.

Merry Christmas in Austria: Unique Ways to Celebrate and Greet

You may want to see also

Frequently asked questions

Income tax rates in Austria are progressive, ranging from 20% to 55% of taxable income. The more you earn, the higher the rate of taxation.

Austria has one of the highest personal income tax rates in Europe.

The corporate tax rate in Austria is 24% as of 2023, down from 25% in 2022.

There are several other types of taxes in Austria, including value-added tax (VAT), municipal tax, real estate tax, vehicle insurance tax, and property tax.