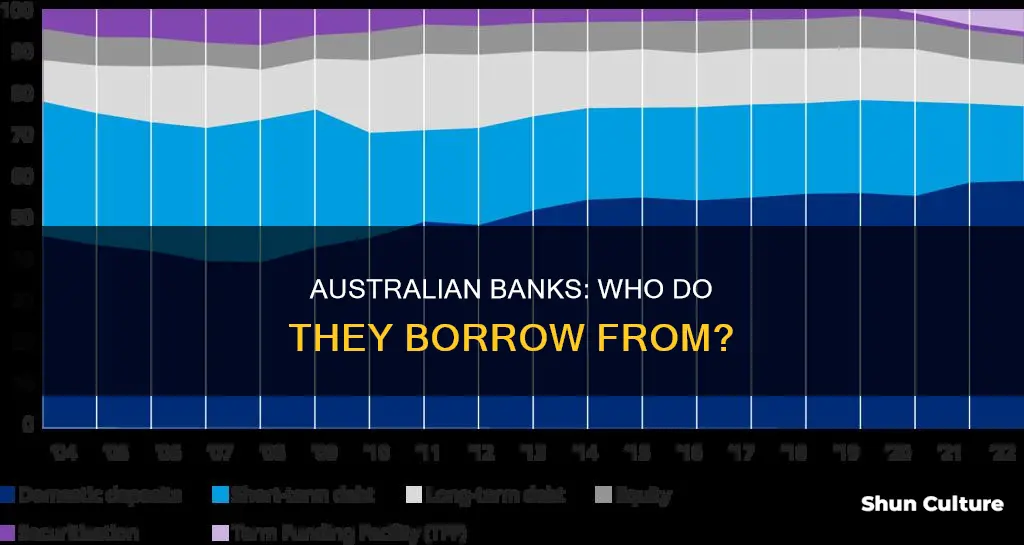

Australian banks get their funding from a variety of sources, including deposits, borrowing from other market players, shareholder equity, and long-term and short-term debt. While over 60% of bank funding in Australia still comes from domestic deposits, banks have increasingly turned to offshore funding markets to access a wider range of investors and diversify their funding sources. In recent years, the Reserve Bank of Australia (RBA) has also provided cheap loans to major banks, totalling $188 billion, to stimulate the economy. Additionally, the Australian Government Securities (bonds) issued by the AOFM, help manage the government's borrowing needs and ensure sufficient funds to meet payment obligations.

| Characteristics | Values |

|---|---|

| Sources of funding | Domestic deposits, long-term debt, short-term debt, equities, securitisation of assets, borrowing from other players in the market, shareholder equity |

| Percentage of funding from domestic deposits | Over 60% |

| Liquidity risk mitigation | Holding liquid assets, maintaining minimum liquid asset requirements, structuring borrowing and lending to minimise liquidity risk |

| Offshore funding markets | Used for access to larger investor base, capacity to absorb bonds of various credit ratings and maturities, and diversification of funding sources |

| Offshore funding risks | Higher rollover risk due to investor tendency to restructure portfolios towards domestic investments during liquidity stress and lack of access to central bank liquidity support |

| Government involvement | Australian Office of Financial Management (AOFM) borrows money on behalf of the government by issuing Australian Government Securities (bonds) |

| Reserve Bank of Australia (RBA) involvement | Introduced the Term Funding Facility in March 2020, offering cheap loans to banks to support lending to businesses |

Explore related products

$15.99

![Borrowing from Your Bank 1923 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

![]()

Banks borrow from customers' deposits

Banks obtain funding from a variety of sources, including deposits, borrowing from other market players, and shareholder equity. In Australia, over 60% of bank funding is financed by domestic deposits, with the remaining sources being long-term debt, short-term debt, equities, and securitization of assets.

When customers deposit money into their savings accounts, banks use this money to fund loans and pay interest to the customers. This process is known as fractional reserve banking, where banks lend a portion of their customers' deposits while maintaining sufficient reserves to meet withdrawal demands. The Federal Reserve sets interest rates based on economic conditions and its dual mandate of maximum employment and price stability.

Through financial intermediation, banks distribute deposits as loans to other customers, charging a higher interest rate on the loans than they pay out to depositors. For example, a customer with a savings account earning 4% annual interest receives $20 in interest on a $500 deposit. The bank may then lend out $400 of that deposit as a personal loan with a 10% annual interest rate, earning $40 in interest. The bank keeps the $20 difference as profit, which is used to pay shareholders.

In addition to customer deposits, banks also borrow from other sources, such as the wholesale market or overnight money markets, to meet their funding needs. However, wholesale market funding tends to be more expensive compared to deposits, making it challenging for banks to rely heavily on this source.

While banks primarily borrow from customer deposits, they also have access to other funding sources, such as borrowing from the market or shareholders, to ensure they can meet their financial obligations.

Virgin Australia's Bangkok Flights: Where, When, and How?

You may want to see also

Explore related products

$5 $16.95

![]()

They also borrow from other players in the market

Australian banks borrow money from a variety of sources, including deposits, borrowing from other players in the market, and shareholder equity. In terms of borrowing from other market players, banks often borrow from other customers or corporate depositors. This is a common practice to fund loans to corporate customers. For example, a bank may borrow $100 from a corporate depositor for three years and then lend that money to another corporate customer for the same period. When the loan is repaid by the borrower, the bank uses those funds to repay the original depositor.

Banks also borrow from other players in the market by issuing bonds. Mortgage-backed securities allow banks to pool mortgages together to support a bond issue and sell the debt to investors. This practice enables banks to provide a larger number of home loans. Additionally, government bonds are another avenue for banks to borrow from the market. The AOFM (Australian Office of Financial Management) borrows money on behalf of the Australian government by issuing Australian Government Securities (bonds). Banks, as registered bidders, can submit bids for these bonds.

Furthermore, Australian banks have historically accessed funding from offshore markets, including countries like the United States, Europe, Japan, and Hong Kong. These offshore funding markets offer advantages such as access to a larger investor base, the ability to absorb bonds of various credit ratings and maturities, and a more diversified funding base. However, borrowing in foreign currencies also carries exchange rate and interest rate risks, which banks hedge using cross-currency swaps.

Overall, borrowing from other players in the market is a significant aspect of how Australian banks secure their funding. By utilising deposits, issuing bonds, accessing offshore markets, and borrowing from customers and corporate depositors, banks are able to meet their funding needs and support their lending activities.

Virgin Australia's LAX Terminal: Where to Fly From

You may want to see also

Explore related products

![]()

Borrowing from shareholder equity

Banks in Australia get their funding from a few sources, including deposits, borrowing from other players in the market, and shareholder equity. Borrowing from shareholder equity can take the form of a shareholder loan, where a shareholder loans money to their company or borrows money from the company. This is also known as "Due to Shareholder" or "Due from Shareholder".

Shareholder loans can be problematic if they are not properly documented. If a dispute arises between shareholders, or if a shareholder wants to exit the company, dies, or becomes incapacitated, the lack of documentation can lead to costly disputes. It is recommended that all private companies with outstanding loans from shareholders review the loan arrangements and ensure that the terms and conditions are set out in a legally binding document, such as a loan agreement.

In Australia, each state and territory has a Statute of Limitation, which means that a loan to a company can expire if no repayments are made or demanded. Shareholder loans can also have tax implications if they are not carefully managed. For example, if a shareholder borrows money from the company, that amount may need to be included in their personal income for the year, resulting in additional personal income tax.

It is important to note that shareholder loans can refer to money loaned by shareholders to the company or money borrowed by shareholders from the company. Proper bookkeeping and accounting practices are essential to avoid tax issues and ensure compliance.

Is Vodka Gluten-Free in Australia?

You may want to see also

Explore related products

![]()

Borrowing from the Reserve Bank of Australia (RBA)

The Reserve Bank of Australia (RBA) is Australia's central bank and is responsible for implementing monetary policy and maintaining a stable financial system. The RBA achieves this by setting a target for the cash rate, which influences interest rates in the economy, including lending and deposit rates. Banks can borrow funds from the RBA at a rate slightly above the target cash rate. This rate is typically higher than the market cash rate, so banks prefer to borrow from each other in the cash market, where funds are lent and borrowed overnight. However, in certain situations, such as when banks experience liquidity issues, borrowing from the RBA becomes more attractive.

The RBA also provides other forms of lending to banks. For example, in 2020, the RBA established a Term Funding Facility (TFF) to lower funding costs across the economy. The TFF offered banks low-cost, fixed-term funding with an interest rate fixed at the cash rate target, which was lower than banks' usual rates. This allowed banks to offer lower interest rates on loans to households and businesses.

Additionally, the RBA is willing to lend Exchange Settlement (ES) balances to banks if required. ES balances are used to settle interbank transactions, and their demand can vary due to changing financial market conditions. Banks have an incentive to borrow ES balances from the RBA when market interest rates for cash balances are below the target cash rate.

The RBA's lending activities are an important aspect of its role in maintaining financial stability and ensuring the smooth flow of money within the economy. By providing access to funds, the RBA helps banks manage their liquidity and continue lending to households and businesses, contributing to economic activity and growth.

Rice Bubbles: Gluten-Free in Australia?

You may want to see also

Explore related products

![]()

Borrowing from offshore funding markets

Australian banks borrow money from a variety of sources, including offshore funding markets. This access to large and deep foreign funding markets supplements their domestic funding. While over 60% of bank funding in Australia is financed by domestic deposits, the composition of funding also includes long-term debt, short-term debt, equities, and securitization of assets.

Offshore funding accounts for about one-third of the major banks' worldwide operations' assets. This funding is raised in multiple ways, across several countries, and by various entities within banking groups. This enables banks to diversify their funding sources, access deeper and more liquid markets, and borrow for longer terms than they often can domestically.

However, offshore funding can be riskier than domestic funding due to the inherent 'rollover risk' in banking. This risk is higher in offshore funding for two main reasons. Firstly, investors tend to reallocate their portfolios towards domestic investments during times of stress in global financial markets, making it harder to roll over offshore funding. Secondly, banks borrowing in foreign currencies often lack access to central bank liquidity support in that currency.

The four major Australian banks obtain a large share of their funding from offshore wholesale markets. These banks' subsidiaries in other countries can also access local deposits and liquidity support, which changes the nature of the liquidity risks they face.

Offshore fund managers are attracted to Australia's large and fast-growing funds management industry, supported by a robust superannuation system and a growing base of long-term investors.

Tasman Guitars: Australian-Made or Not?

You may want to see also

Frequently asked questions

Australian banks borrow money from a variety of sources, including deposits, other players in the market, shareholder equity, and long-term and short-term debt.

Examples include the Reserve Bank of Australia (RBA), which introduced the Term Funding Facility in March 2020, and the Australian Office of Financial Management (AOFM), which borrows money on behalf of the Australian government by issuing Australian Government Securities (bonds).

One risk is liquidity risk, which occurs when banks borrow money for short terms and lend that money to customers for longer terms. If depositors want to withdraw their deposits after a short time, the bank may not be able to immediately get money back from the loan.

Australian banks can mitigate liquidity risk by holding a minimum level of liquid assets (assets that can be easily and quickly converted to cash) and by structuring their borrowing and lending to reduce the opportunity for liquidity risk.

Borrowing money can help Australian banks reduce their funding costs, access a larger investor base, and diversify their funding sources. It can also help stimulate the economy, support small businesses, and provide access to cheaper loans for borrowers.