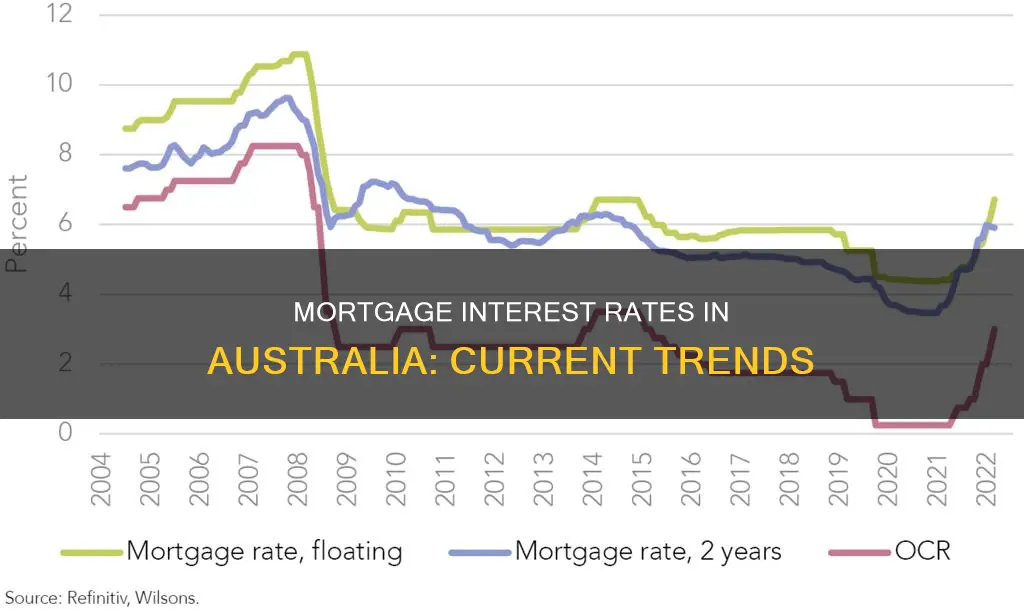

The interest rate on a mortgage loan in Australia can vary depending on the lender and market conditions. The Reserve Bank of Australia (RBA) influences the cash rate and other economic factors that impact variable interest rates offered by banks and other lenders. When the RBA adjusts the cash rate, lenders tend to pass on the change to borrowers, affecting their loan repayments. As of 2025, the RBA cut rates, creating uncertainty about future adjustments. Comparison rates, which consider fees and charges, offer a more accurate representation of the loan's interest rate. Canstar, a prominent Australian comparison website, provides a mortgage repayment calculator to estimate interest payments based on the borrowed amount and interest rate.

| Characteristics | Values |

|---|---|

| Type of Interest Rate | Variable Interest Rate, Comparison Rate |

| Factors Affecting Interest Rate | Reserve Bank of Australia's (RBA) cash rate, economic factors |

| Comparison Rate | Includes annual interest rate and most upfront and ongoing fees and charges |

| Comparison Rate Calculation | Based on a $150,000 loan over 25 years |

| Variable Interest Rate | Can fluctuate according to the lender's wishes and economic factors |

| Current RBA Cash Rate | Unclear, RBA cut rates in February 2025 |

Explore related products

What You'll Learn

![]()

Variable interest rates

When the RBA raises the cash rate, banks and lenders tend to be quick to pass the change on to home loan borrowers, with most major financial institutions passing the hike on in full. Similarly, when the cash rate falls, lenders drop their rates. Variable rates can offer more flexibility than fixed rates, but they come with the risk of rate increases. A home loan comparison rate helps show the true cost of the loan by combining the interest rate with certain fees and charges. It is expressed as a single percentage to make it easier to compare different loans. This way, you can see the overall cost, not just the advertised interest rate.

A comparison rate is a rate that all lenders by law must display next to their advertised interest rates. It represents the total annual cost of the loan, including its annual interest rate and most ongoing and upfront fees and charges. Under Australian law, all comparison rates for home loans are based on a $150,000 loan over 25 years. However, it is important to note that this comparison rate may not include all fees and charges, and different terms, fees, or loan amounts might result in a different comparison rate.

Variable-rate loans generally allow for greater flexibility and more features than fixed-rate loans, although their interest rates can sometimes be higher as well. If you're considering a variable interest rate for your home loan, it's important to carefully weigh the pros and cons and compare rates from different lenders to find the best option for your needs.

Suicide Rates: Australia's Darkest City

You may want to see also

Explore related products

![]()

Comparison rates

When comparing mortgage rates, it's important to consider not just the interest rate but also the comparison rate, which takes into account certain fees and charges associated with the loan. This gives borrowers a more accurate representation of the loan's interest rate after accounting for these costs. By law, lenders must display the comparison rate alongside the advertised interest rate.

Variable interest rates can fluctuate over time, influenced by the Reserve Bank of Australia's (RBA) cash rate and other economic factors. These rates offer more flexibility but come with the risk of rate increases. On the other hand, fixed-rate loans have a set interest rate for a specified period, usually between one and five years. While less than 3% of borrowers choose fixed rates, these loans may be attractive to those seeking stability in their repayments.

When comparing mortgages, it's essential to consider your personal circumstances, preferences, and financial priorities. The best mortgage for you is one that meets your specific needs and financial goals. This may include considering factors such as the loan's interest rate, repayment type, and loan purpose. Additionally, shopping around and comparing a wide range of options can help you find the most competitive rates and features that align with your requirements.

Converting $19,000 to Australian Dollars: How Much Is It?

You may want to see also

Explore related products

![]()

Official cash rate target

The Reserve Bank of Australia (RBA) sets a target cash rate, also known as the official cash rate, which influences interest rates in the economy, including lending and deposit rates. Banks can deposit funds with the RBA overnight and earn a little below the target cash rate, and they can also borrow funds from the RBA at a little above the target rate. The RBA can also transact in Australia's money markets to affect the supply and demand for cash, steering the cash rate towards the target.

The RBA's Monetary Policy Board decides whether to change or maintain the cash rate target. The Board is made up of the Governor, Deputy Governor, Secretary to the Australian Treasury, and six other members appointed by the Treasurer. They meet eight times a year to consider monetary policy settings, following the release of key economic data on inflation and economic activity.

The RBA's primary objectives are to keep consumer price inflation between 2% and 3% and to achieve sustained full employment. These objectives help maximise the economic prosperity and welfare of Australians.

The RBA rate indicator provides market participants and commentators with a market monitor for official cash rate expectations. The Target Rate Tracker uses the 30-day cash rate futures implied yields to calculate the probability of changes to the Overnight Cash Rate. While the Overnight Cash Rate is generally the same as the Official Cash Rate, there may be times when it differs due to prevailing market conditions.

Fly Screen Maintenance: Re-Installation Guide for Australians

You may want to see also

Explore related products

![]()

Fixed-rate loans

The certainty of a fixed-rate loan can be beneficial for those who want to know they can afford their repayments, especially if they are expecting a change in circumstances, such as starting a family. It can also protect borrowers from sudden increases in interest rates. However, if interest rates were to decrease, those with a fixed-rate loan would still be required to pay the same rate of monthly repayments until the loan period concluded.

After the fixed-rate period expires, the borrower's loan may move to a variable rate, or they may be able to negotiate another fixed-rate term, depending on the home loan provider. Variable rates can be influenced by the Reserve Bank of Australia's (RBA) cash rate and other economic factors. They offer more flexibility but come with the risk of rate increases.

While fixed-rate loans can provide peace of mind, they may not be the best option for everyone. They do not allow for additional repayments to be made, and they can make it more difficult to refinance or break the loan early. Most Australians choose variable loans, and only 4% of home loans that went through mortgage brokerage AFG in the last three months of 2024 were fixed-rate loans.

If you are considering a fixed-rate loan, it is important to do your research and speak to a mortgage broker about what rate and term period is best for your financial situation.

Free Apple TV Channels in Australia: The Ultimate Guide

You may want to see also

Explore related products

![]()

Lenders and institutions

Lenders and financial institutions play a crucial role in the Australian mortgage market, offering a range of home loan options with varying interest rates. The interest rate offered by lenders is influenced by several factors, including the borrower's credit rating, the loan-to-value ratio, and the purpose of the loan.

When assessing a borrower's eligibility for a loan, lenders consider their financial situation and credit profile. A strong credit rating can lead to more favourable interest rates and loan terms. Additionally, having a higher deposit or more equity in the home can result in a lower interest rate, as a lower loan-to-value ratio reduces the lender's risk.

The purpose of the loan also impacts the interest rate. Investment and interest-only loans tend to have higher interest rates compared to residential owner-occupier loans. This is because owner-occupier loans are considered less risky by lenders.

Australia's mortgage interest rates can be either fixed or variable. Fixed-rate loans offer stability and predictability, locking in the interest rate for a set period, typically between one and five years. On the other hand, variable-rate loans fluctuate over time, influenced by the Reserve Bank of Australia's (RBA) cash rate and economic factors. While variable rates offer flexibility, they come with the risk of unexpected rate increases.

It is worth noting that borrowers have the option to negotiate with their lender for a more competitive interest rate. Additionally, features like offset accounts and extra repayment options can help reduce interest costs over time. Comparing multiple lenders and utilising a mortgage broker can assist borrowers in finding the most suitable loan for their needs.

As of April 2025, home loan interest rates in Australia start from 4.94%average owner-occupier interest rate at the end of December 2023 being around 5.85%. These rates are subject to change and vary depending on the lender and the borrower's circumstances.

Copper Mining in Australia: A Comprehensive Overview

You may want to see also

Frequently asked questions

As of March 24, 2025, the average mortgage interest rate in Australia is 5.23%. However, rates are updated daily and can vary depending on the lender and economic factors.

The Reserve Bank of Australia (RBA) determines the official cash rate target, which serves as a benchmark interest rate for the cost of borrowing money. When the cash rate increases, lenders tend to pass on the higher costs to borrowers, and when it decreases, lenders drop their rates. The RBA considers various economic factors when setting the cash rate, such as economic growth, inflation, and debt.

Variable interest rates can change at any time, and these fluctuations are influenced by the RBA's cash rate and other economic factors. In contrast, fixed-rate loans offer more predictability with a set interest rate over the loan's life.

You can compare current home loan interest rates from different lenders to find the most competitive offer. A home loan comparison rate is a useful tool that combines the interest rate with associated fees and charges to provide a single percentage for easier comparison. Online tools and calculators can assist in estimating monthly repayments and total costs.

![Apple Watch SE 3 [GPS + Cellular 44mm] Smartwatch with Starlight Aluminum Case with Starlight Sport Band - M/L. Fitness and Sleep Trackers, Heart Rate Monitor, Always-On Display, Water Resistant](https://m.media-amazon.com/images/I/619GFuR9-fL._AC_UY218_.jpg)