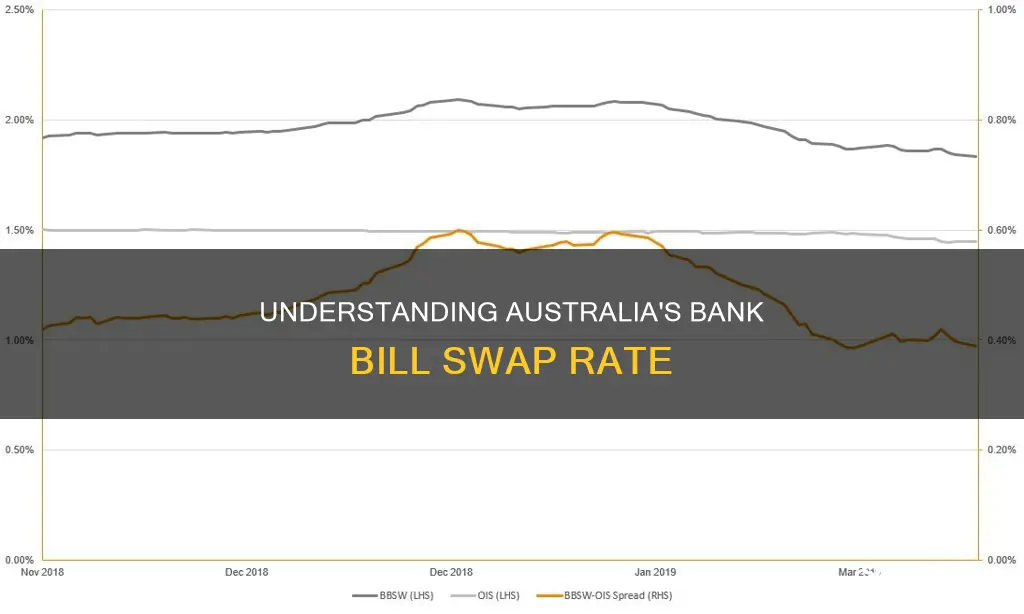

The Bank Bill Swap Bid Rate (BBSY) is an Australian benchmark interest rate quoted and dispersed by Thompson Reuters Information Service. The BBSY is used by financial institutions and corporations engaging in interest rate swaps and related transactions. The Bank Bill Swap Rate (BBSW) is a short-term interest rate used as a benchmark for the pricing of Australian dollar derivatives and securities, most notably floating-rate bonds. The BBSW is calculated and published by the Australian Securities Exchange (ASX).

| Characteristics | Values |

|---|---|

| Full Form | BBSY or Bank Bill Swap Bid Rate |

| Governing Body | ASX Ltd |

| Publishing Time | 10:15 a.m. daily |

| Publishing Platform | Thomson Reuters and Bloomberg LLP |

| Usage | Used by financial institutions and corporations engaging in interest rate swaps and related transactions |

| Usage | Used as the base rate for debt financing |

| Calculation | Calculated as the average of the national best bid and best offer (NBBO), rounded to four decimal places |

| Calculation | Calculated as the average of bank bill rates supplied by banks for various maturities |

| Calculation | Calculated as the average of the year's interest rates for bank bills plus any risk premium |

| Similarity | Similar to London Interbank Offered Rate (LIBOR) |

Explore related products

What You'll Learn

![]()

Bank Bill Swap Bid Rate (BBSY)

The Bank Bill Swap Bid Rate (BBSY) is an Australian benchmark interest rate quoted and disseminated by the data provider Thomson Reuters Information Service. BBSY is used as a base rate for debt financing. It is similar to the London Interbank Offer Rate (LIBOR). BBSY is derived from the BBSW (Bank Bill Swap Rate), which is calculated as the average of the national best bid and best offer (NBBO), rounded to four decimal places. BBSY is calculated in a similar manner, but instead of the mid-price, the average bid-price is used.

BBSY is commonly used by banks, financial institutions, and investors as it determines short-term floating interest rates. It is used to price and value Australian dollar securities, and banks use it to borrow money. BBSY is used in plain vanilla interest rate swap agreements, where two counterparties agree to swap interest payments for a predetermined period. For example, one party might pay a fixed interest rate and receive a floating rate of BBSY + 0.35%.

BBSY is used to determine rates all over the world, not just in Australia, and is a simple instrument but can have powerful repercussions when it adjusts.

Are Australian Government Pensions Taxable?

You may want to see also

Explore related products

![]()

BBSY and interest rate swaps

The Bank Bill Swap Bid Rate (BBSY) is a benchmark interest rate in Australia that is used as a reference rate in interest rate swaps. BBSY is derived from the Bank Bill Swap Rate (BBSW), which is calculated as the average of the national best bid and best offer (NBBO), rounded to four decimal places. The BBSY is the average bid price, while the BBSW is the average mid-price.

BBSY is published daily at 10:15 a.m. on Thomson Reuters and Bloomberg LLP. It is used by financial institutions and corporations in Australia to calculate interest rates on financial contracts and determine short-term floating interest rates. BBSY is also used as the base rate for debt financing, similar to the London Interbank Offer Rate (LIBOR).

In an interest rate swap, two counterparties agree to exchange streams of interest payments for a predetermined period. One party pays a fixed interest rate and receives a floating interest rate that is dependent on the movement of BBSY. For example, one company may pay a 2% fixed interest rate and receive a floating rate of BBSY + 0.35%. If BBSY is 1.90%, the first company pays $10,000, while the second company pays $11,250, calculated on a notional principal amount of $1 million.

BBSY plays a crucial role in interest rate swaps by providing transparency and efficiency in the financial system. It allows for risk management and facilitates the efficient pricing and valuation of securities. However, it is subject to market fluctuations and relies on data from multiple financial institutions, which can introduce potential inaccuracies.

Understanding Weekend Work: Australia's Saturday Penalty Rates

You may want to see also

Explore related products

![]()

BBSY and Australian dollar securities

In Australia, the Bank Bill Swap Bid Rate (BBSY) is the interest rate used in the financial markets for the pricing and valuation of Australian dollar securities. It is also used by banks to borrow money and to determine short-term floating interest rates. The BBSY is managed and published daily at 10:15 a.m. by ASX Ltd, which operates Australia's primary national stock exchange and equity derivatives market. The published rates are used by financial institutions to calculate interest rates on financial contracts, promoting transparency and efficiency in the country's financial system.

The BBSY is derived from the Bank Bill Swap Rate (BBSW), which is calculated as the average of the national best bid and best offer (NBBO), rounded to four decimal places. The BBSW is an independent reference rate used for pricing securities, particularly floating-rate bonds. It is a short-term interest rate that serves as a benchmark for the pricing of Australian dollar derivatives and securities. A risk premium is added to the BBSW to compensate for the risk of the securities compared to the risk-free rate, which is usually based on government bonds.

The BBSY is used as the base rate for debt financing and is similar to the London Interbank Offered Rate (LIBOR). It is a floating rate that can be used in interest rate swaps, where two counterparties agree to exchange streams of interest payments for a predetermined period. In these agreements, the BBSY is agreed upon as the reference rate to determine the payment amounts. The floating rate used in interest rate swaps is BBSY plus or minus a margin, for example, BBSY + 35 basis points.

The BBSY is a crucial tool for banks, financial institutions, and investors in determining short-term floating interest rates and pricing Australian dollar securities. It provides a transparent and efficient mechanism for calculating interest rates and managing debt financing in Australia.

Bacon Lovers in Australia: Can You Eat Raw Bacon?

You may want to see also

Explore related products

![]()

Bank Bill Swap Rate (BBSW)

The Bank Bill Swap Rate (BBSW) is a short-term interest rate used as a benchmark for pricing Australian dollar derivatives and securities, most notably floating-rate bonds. It is Australia's equivalent of the London Interbank Offered Rate (LIBOR), used as a reference rate on an institutional level.

The BBSW is calculated as the average of the bank bill rates supplied by banks for various maturities. It is published daily by the Australian Securities Exchange (ASX), which maintains this rate. The BBSW is an independent reference rate used for pricing securities. Fixed-income investors use the BBSW as a benchmark to price floating-rate bonds and other securities.

A risk premium is added to the BBSW to compensate for the risk of the securities as compared to the risk-free rate, which is usually based on government bonds. The credit premium added is typically small, ranging from five to ten basis points. However, it exceeded 300 basis points during the 2008 financial crisis.

The BBSW is used in interest rate swaps, where two counterparties agree to swap streams of interest payments for a predetermined period. One party swaps fixed-interest payments and receives floating interest payments dependent on the movement of the BBSW.

Australia's Plan to Reduce Food Waste

You may want to see also

Explore related products

![]()

BBSW and LIBOR

The Bank Bill Swap Rate (BBSW) is a short-term interest rate used as a benchmark for the pricing of Australian dollar derivatives and securities, most notably floating-rate bonds. BBSW is quoted by prime Australian banks and is based on the price of a discounted security. It is considered a midpoint of all interest rates. BBSW is Australia's local credit-benchmark and is expected to continue.

BBSW is independent of other retail lending indexes, so its impact in these areas is minimal. However, a risk premium is added to compensate for the risk of the securities, which can be substantial during financial crises.

LIBOR, the London Inter-bank Offered Rate, was a globally accepted key benchmark interest rate for financial markets for over 40 years. It was published in five currencies and seven tenors and comprised daily estimates of borrowing costs in the unsecured market provided by major banks. LIBOR was commonly used in financial arrangements, including loans, derivative arrangements, internal pricing, and other financial arrangements.

However, LIBOR's demise was predicted after the 2007-2008 financial crisis, as it was no longer anchored in a robust underlying market, making it unsuitable as a widely used reference rate. As a result, major financial markets, including Australia, adopted alternative reference rates, such as BBSW, which is now the equivalent interest rate benchmark for the Australian dollar.

While BBSW and LIBOR are both interest rate benchmarks, the critical difference is that BBSW has enough transactions in the local bank bill market each day to calculate a robust benchmark, whereas LIBOR does not due to a lack of transactions in the short-term wholesale funding market.

Exploring Australia's Unique System of Government

You may want to see also

Frequently asked questions

The Bank Bill Swap Bid Rate (BBSY) is an Australian benchmark interest rate quoted and dispersed by the data provider Thomson Reuters Information Service. It is used by financial institutions or corporations engaging in interest rate swaps and related transactions.

The BBSY is derived from the BBSW (Bank Bill Swap Rate), which is calculated as the average of the national best bid and best offer (NBBO), rounded to four decimal places. This average mid-price is made available by independent authorities using a transparent algorithm based on information from numerous financial institutions.

The Bank Bill Swap Rate (BBSW) is a short-term interest rate used as a benchmark for the pricing of Australian dollar derivatives and securities, most notably floating-rate bonds. It is calculated and published by the Australian Securities Exchange (ASX).