Planning for retirement is a crucial aspect of financial management, and determining the income required for a comfortable retirement in Australia is a common concern. While some sources suggest a figure of $1 million, the reality is that most Australians will not have this amount saved up by the time they retire. Various factors influence the income needed, including life expectancy, desired lifestyle, home ownership status, and potential government support. Retirement projection tools and calculators can assist individuals in estimating their unique financial goals and planning accordingly. This process involves considering pre-retirement income, expenses, and the potential impact of investments or casual work during retirement. Understanding these factors can help Australians make the most of their retirement years and achieve financial comfort.

| Characteristics | Values |

|---|---|

| Median super balance for men aged 60-64 | $211,996 |

| Median super balance for women aged 60-64 | $158,806 |

| Average lifespan in Australia | 84.18 years |

| Average number of years a person retiring at 60 will need money for | 25 years |

| Maximum Age Pension for singles | $30,000 per year |

| Maximum Age Pension for couples | $45,000 per year |

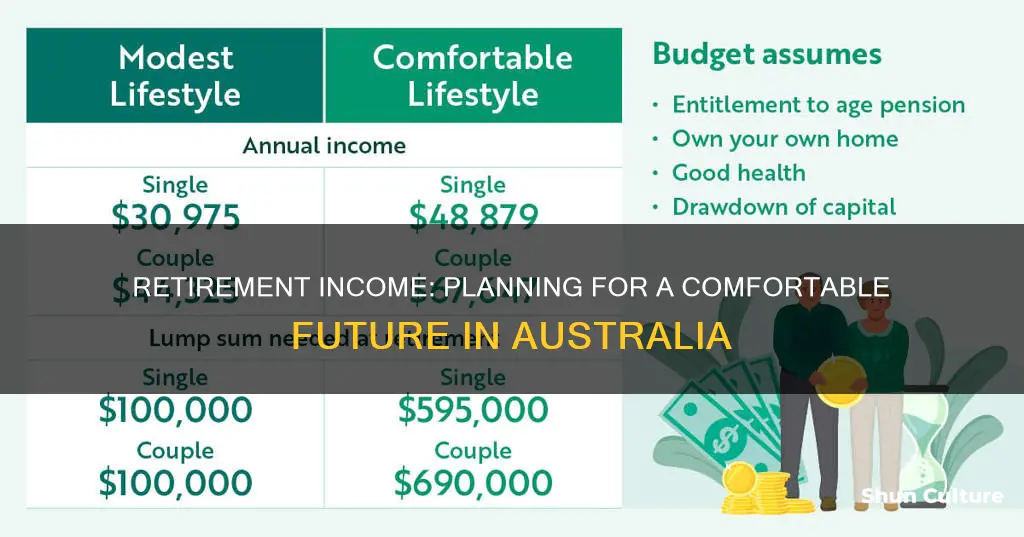

| Modest retirement income for singles aged 67 | $32,897 per year |

| Modest retirement income for couples aged 67 | $47,470 per year |

| Comfortable retirement income for singles aged 67 | $51,805 per year |

| Comfortable retirement income for couples aged 67 | $73,077 per year |

| Super balance required for a retirement income of $60,000 per year for singles | $76,000 |

| Super balance required for a retirement income of $84,000 per year for couples | $95,000 |

| Super balance required for a comfortable retirement income of $52,000 per year for singles | $595,000 |

| Super balance required for a comfortable retirement income of $73,000 per year for couples | $690,000 |

Explore related products

What You'll Learn

![]()

Retirement income calculators

One important consideration when using a retirement income calculator is whether it is specifically designed for Australian retirees. Australia has a unique superannuation system, and calculators tailored to the Australian market will also consider domestic costs of living, tax benefits, life expectancy, and way of life. For example, the Industry Super retirement calculator takes into account all the expenses you are likely to encounter as a retiree in Australia, including the cost of living, life expectancy, and the Age Pension. It then estimates the level of income you will need to cover these expenses and how much superannuation you will require to achieve that.

Another factor to consider is whether the calculator provides a generic or tailored estimate. Some calculators use a generic approach, suggesting you withdraw a certain percentage of your superannuation and investments in the first year and adjust for inflation thereafter. In contrast, more comprehensive calculators will require more input, such as your preferred retirement age, annual income, and expenses, to provide a more tailored answer. For example, the Moneysmart.gov.au retirement planner considers factors such as your eligibility for the Age Pension, your income needs, and the impact of fees and investment choices on your retirement income.

It is important to remember that retirement income calculators provide estimates and cannot predict your final superannuation benefit or level of retirement income with certainty. Your personal circumstances, unexpected life events, investment earnings, tax, and inflation can all impact your retirement income. Therefore, it is recommended to regularly update your projections and consider seeking financial advice to ensure you are making the most of your retirement savings.

In addition to using retirement income calculators, there are other methods to estimate how much income you will need in retirement. One approach is to consider your pre-retirement income and assume you will need a percentage of that amount during retirement. For example, you may estimate that you will need 70% of your pre-retirement income to maintain your current standard of living. Another method is to plan a yearly budget and calculate the lump sum required to cover your expenses during retirement.

Criterion's Shipping to Australia: What's the Deal?

You may want to see also

Explore related products

$14.87 $19.99

![]()

Average retirement income

The average retirement income in Australia depends on two factors: the type of lifestyle one leads and whether they are single or a couple. There is no data available on the average income of retirees in Australia, as superannuation pensions and lump sums from age 60 do not need to be recorded on tax returns. However, the Association of Superannuation Funds of Australia (ASFA) provides a breakdown of retirement expenditure for singles and couples, which can be used to calculate an average retirement income.

The average retirement income for single people in Australia is approximately $33,000 per year for a modest lifestyle and $52,000 per year for a comfortable lifestyle. For married couples, the average retirement income is approximately $47,000 per year for a modest lifestyle and $73,000 per year for a comfortable lifestyle. These figures assume that retirees own their homes outright and are relatively healthy.

The cost of living varies across Australia, with cities like Sydney and Melbourne being more expensive than small regional towns. Therefore, it is important to consider personal needs and objectives when planning for retirement. The main source of retirement income for Australians is the Government Age Pension, followed by superannuation income streams. The amount of Age Pension received depends on factors such as assets, superannuation amounts, and other sources of income.

Retirement income can be maximised through various strategies to grow retirement income, including superannuation contributions, investments, rental income, and annuities. It is recommended to seek expert financial advice to determine the optimal strategies for an individual's circumstances. Retirement income calculators can also be utilised to estimate the required retirement income, taking into account factors such as taxation, investment returns, and life expectancy.

Germany vs Australia: A Size Comparison

You may want to see also

Explore related products

$140 $139.99

![]()

Retirement income by age

Retirement income needs vary depending on age, gender, and lifestyle choices. According to the Australian Tax Office, men aged 60-64 have a median super balance of $211,996, while women in the same age group have a median balance of $158,806. However, most people heading into retirement won't have seven-figure superannuation balances.

The Association of Superannuation Funds of Australia (ASFA) provides quarterly estimates of the income required for a modest or comfortable retirement, assuming individuals own their homes. As of July 2025, a single person aged 67 needs an annual income of $32,897 for a modest retirement and $51,805 for a comfortable one. For a couple of the same age, these figures rise to $47,470 and $73,077, respectively. A modest retirement assumes basic activities are affordable, while a comfortable retirement enables a broader range of leisure activities, higher-quality health cover, and occasional restaurant meals.

Retirement income sources vary and may include the Age Pension, superannuation pensions, lump sums, personal investments, rental income, annuities, and casual work. The Age Pension is a government payment acting as a 'safety net' for those who meet the age and residency requirements. Around 2.6 million Australians over 65 receive a full or partial Age Pension, with the amount depending on assets, superannuation balances, and other income sources.

To estimate retirement income needs, individuals can use a super projection calculator to factor in current super savings, retirement goals, and potential changes. Another approach is considering a percentage of pre-retirement income needed, assuming 70% as a starting point. For example, if an individual earns $50,000 before retirement, they might need $32,500 annually during retirement.

Additionally, planning a yearly budget or using ASFA's yearly spending figures as a guide can be helpful. Individuals should also be prepared for unexpected costs, such as health issues or caring for a loved one, and consider the potential impact of inflation and investment returns on their retirement income goals.

Applying for an Australian PR Card: A Step-by-Step Guide

You may want to see also

Explore related products

$25.62 $29.99

![]()

Retirement income and housing

Understanding Retirement Income Needs

The Association of Superannuation Funds of Australia (ASFA) provides a trusted benchmark with its Retirement Standard, offering a breakdown of estimated expenses for both comfortable and modest lifestyles. The latest figures indicate that a single person aged 67 requires an annual income of $32,897 for a modest retirement and $51,805 for a comfortable one. For a couple of the same age, these figures rise to $47,470 and $73,077, respectively. These estimates assume homeownership and the ability to afford a range of activities and services, from basic to recreational.

The Age Pension and Other Considerations

The Age Pension serves as a crucial safety net for retirees, with around 2.6 million Australians over 65 receiving full or partial support. The amount received depends on factors like assets, superannuation balances, and other income sources. Additionally, life expectancy plays a role in retirement planning, and it's advisable to estimate living longer than the average when calculating your needs. Other considerations include the potential for casual work or income from investments, as well as unexpected health costs.

Housing in Retirement

Housing is a significant factor in retirement planning. While some individuals may aim to own their homes outright by retirement, others may consider downsizing or renting. However, renting in retirement can be challenging, as many retirees who rent in the private market live in poverty due to insufficient savings and inadequate Rent Assistance from the government. As a result, retirees may struggle to afford rent in major cities, highlighting the importance of planning and considering various housing options.

Planning for Retirement

Planning for retirement income and housing is essential, and there are various strategies to consider. One approach is to start with your pre-retirement income and estimate how much of it you'll need during retirement, typically around 70%. Another method involves calculating a lump sum based on current annual expenses and the number of years between retirement age and life expectancy. Exploring different strategies to grow your retirement income, such as extra super contributions, can also help ensure a comfortable retirement.

Free Calling in Australia: Understanding 1300 Numbers

You may want to see also

Explore related products

![]()

Retirement income and lifestyle

The Association of Superannuation Funds of Australia (ASFA) provides guidelines for the level of income required for a modest or comfortable retirement, assuming individuals own their homes. According to ASFA, a single person aged 67 needs an annual income of $32,897 for a modest retirement and $51,805 for a comfortable retirement. For a couple of the same age, these figures rise to $47,470 and $73,077, respectively. A modest retirement lifestyle allows for basic activities, while a comfortable retirement enables retirees to engage in a broader range of leisure activities, purchase household goods, afford private health insurance, and travel.

Retirement projection tools, such as the TelstraSuper Retirement Lifestyle Planner or the Mercer Retirement Income Simulator, can help individuals estimate their retirement income needs based on their circumstances. It is recommended to consider factors like investments outside superannuation and adjust assumptions accordingly. Additionally, the Australian Government's Age Pension acts as a safety net for those who need additional income during retirement, with the amount depending on assets, superannuation, and other sources of income.

It is worth noting that the income required in retirement may decrease over time as retirees tend to spend less as their health deteriorates and their discretionary spending reduces. Downsizing and budgeting can also help manage retirement expenses. Planning for retirement income involves considering pre-retirement income, life expectancy, investment returns, inflation, and personal expenses. Starting retirement planning early increases the chances of achieving one's retirement income goals.

In summary, a "good" retirement income in Australia varies depending on individual circumstances and lifestyle choices. Tools and guidelines are available to help estimate income needs, and government support is also provided through the Age Pension. Early planning and consideration of various factors can help ensure a comfortable retirement lifestyle.

Cannibal Holocaust: Australia's Ban Explored

You may want to see also

Frequently asked questions

The amount of money you will need to retire in Australia depends on your desired retirement lifestyle and where you want to live. According to the ASFA Retirement Standard, a single person can enjoy a "comfortable lifestyle" on around $52,000 a year, while a couple would need $73,000. However, if you want to take part in a wider range of leisure activities and travel more frequently, you may need a higher income, such as $60,000 a year for a single person or $84,000 a year for a couple.

A "comfortable retirement" in Australia is typically defined as being able to afford a wide range of activities and services, including leisure and recreational activities, household goods, private health insurance, a reasonable car, good clothes, electronic equipment, and travel within Australia and overseas.

The average retirement age in Australia is 65 years old. However, some people may choose to retire earlier or later depending on their financial situation and personal preferences.

The Age Pension is a government payment that acts as a safety net for Australians who meet the age and residency requirements. It is designed to provide additional income to those who don't have enough financial resources to fund their retirement. The amount received depends on various factors, including assets, superannuation, and other sources of income. Around 2.6 million Australians over the age of 65 receive a full or partial government pension.