Australia has been experiencing a series of interest rate hikes, with the Reserve Bank of Australia (RBA) announcing 13 rate rises since May 2022, bringing the cash rate to 4.35%. The RBA meets monthly, except in January, to decide on interest rate changes. While the RBA has not specified when the next rate rise will occur, Australia's big four banks have made predictions. ANZ and CommBank foresee one further hike of 25 basis points in August, while NAB expects two more hikes this year. Westpac predicts hikes in both August and September, bringing the cash rate to a peak of 4.60%. High inflation and the resulting pressure on the economy have been driving factors in the RBA's decisions. However, it is acknowledged that high interest rates place a burden on households and companies, making it unlikely for rates to continue rising indefinitely.

| Characteristics | Values |

|---|---|

| Date of next interest rate rise | Unknown, but predicted to be in August or September 2023 |

| Interest rate | Expected to peak at 4.35% or 4.60% |

| RBA monthly board meeting | First Tuesday of every month (except January) |

| RBA's priority | Return inflation to the target range of 2-3% |

| RBA's next meeting | 4 July 2023 |

| RBA's previous decision | 25 basis point rise in March 2023 |

| ANZ's prediction | One further hike of 25 basis points, peaking at 4.35% in August |

| CommBank's prediction | One further rise of 25 basis points, likely in August, peaking at 4.35% |

| NAB's prediction | Two further cash rate hikes in 2023, peaking at 4.60% |

| Westpac's prediction | Cash rate rises in August and September, peaking at 4.60% |

Explore related products

What You'll Learn

![]()

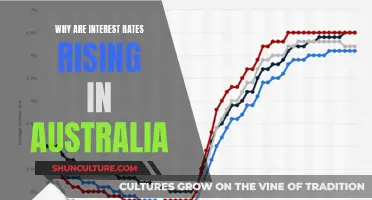

The Reserve Bank of Australia's (RBA) next steps

The RBA has been raising interest rates to tackle high inflation, which currently stands at 7.8% as of December 2022. The RBA's priority is to return inflation to the 2-3% target range. Governor Philip Lowe has stated that high inflation hurts the economy and makes life difficult for people. The RBA is determined to bring inflation under control and will do what is necessary to achieve that.

The RBA meets on the first Tuesday of every month (except January) to decide on interest rate changes. In 2022, the RBA implemented eight consecutive cash rate hikes, totalling 200 basis points. The RBA has continued to raise rates in 2023, with a 25-basis point increase in March. The big four banks in Australia predict that the RBA will continue to raise rates in 2023, with ANZ, CommBank, and NAB forecasting a peak rate of 4.35% in August, while Westpac predicts a higher peak of 4.6% by September.

The RBA's actions are aimed at curbing inflation without causing significant economic damage. However, high interest rates can be unsustainable, placing a burden on households with higher loan repayments and increasing borrowing costs for companies, which may lead to layoffs and higher unemployment. Therefore, the RBA must carefully assess the impact of its rate hikes and make adjustments as needed to avoid a "toxic" economic state.

Looking ahead, the RBA is expected to cut interest rates in 2024 to provide relief to households and businesses. The exact timing and magnitude of these cuts will depend on various factors, including global economic developments, household spending trends, and the inflation and labour market outlook. While interest rates may stabilise around the end of 2024, it is challenging to predict their future with certainty.

Converting 300 Euros: How Much Australian Dollars?

You may want to see also

Explore related products

![]()

Predictions from Australia's big four banks

As of July 2023, Australia's big four banks have made predictions about the movements of the RBA cash rate. ANZ predicts one further hike of 25 basis points, bringing the cash rate to a peak of 4.35% in August. CommBank also predicts one further rise of 25 basis points, likely in August, bringing the cash rate to a peak of 4.35%. CommBank predicts that there will be cuts beginning in the first quarter of 2024, bringing the rate to 3.10% by the end of the year. NAB expects that there will be two further cash rate hikes in 2023, bringing the rate to a peak of 4.60%. They anticipate that there will be cuts beginning in May 2024. Westpac predicts cash rate rises in August and September, bringing the cash rate to a peak of 4.60%, where they expect it to remain until at least May 2024. They expect cuts of up to 75 basis points to occur throughout 2024.

In March 2025, the RBA cut the cash rate to 4.10%, marking the first reduction since 2020. The big four banks revised their forecasts, expecting further cuts, with variation in the timing, pace, and extent of these reductions. CBA predicts the cash rate will drop to 3.35% by December 2025, with a further decline to approximately 3.1% by mid-2026. NAB predicts four cuts post-May 2025, reaching 3.1%. ANZ anticipates the cash rate falling from 4.35% to 3.85% by August 2025, then to 3.6% by December 2026.

Applying to be an Au Pair in Australia: A Guide

You may want to see also

Explore related products

![]()

Impact on home loans and refinancing

The next interest rate rise in Australia is expected to be in August or September 2023, with the cash rate predicted to peak at 4.35% or 4.60%. The Reserve Bank of Australia (RBA) adjusts the official cash rate in response to factors such as inflation, employment, and economic growth. This, in turn, influences the interest rates set by individual lenders for home loans.

When interest rates rise, homeowners typically face increased financial pressure as their mortgage repayments increase. Home loan repayments are often the largest regular expense for mortgage holders, and as interest rates rise, a larger proportion of income is required to meet these repayments. This can result in what is known as "mortgage stress".

In anticipation of or in response to rising interest rates, homeowners have several options to consider:

- Refinancing: Refinancing involves changing loans to take advantage of a different rate or terms, either with the same or a different lender. It allows borrowers to shift to a lower-rate loan, potentially reducing their repayments. However, refinancing is rarely free and may incur costs such as break fees, so it is important to carefully weigh these costs against potential savings.

- Fixed-rate loans: Homeowners can opt for a fixed-rate loan, which locks in a certain interest rate for a set period, usually one to five years. This can safeguard borrowers against higher interest rates during the fixed-rate term. However, fixed-rate borrowers may face restrictions on refinancing or selling their property during this period, and they may miss out on the benefits of potential interest rate cuts.

- Variable-rate loans: Alternatively, borrowers can choose a variable-rate loan, which allows them to take advantage of potential interest rate cuts in the future. However, they also face the risk of higher repayments if rates continue to rise.

- Split home loans: A split home loan offers a combination of fixed and variable rates, providing the benefits of both worlds.

- Fortnightly repayments: Switching to fortnightly repayments instead of monthly can help ease the financial strain by reducing the size of individual repayments.

- Negotiating a lower rate: Homeowners can also simply ask their lender to provide a lower rate of interest, especially if they have been loyal customers with a good track record.

It is important to note that the best course of action depends on the individual's financial circumstances, and seeking advice from a financial specialist is always recommended. Additionally, factors such as spending habits and budget management can also play a crucial role in repositioning finances during periods of high-interest rates.

Galena in Australia: Locations and Sources

You may want to see also

Explore related products

![]()

The effect on the Australian dollar

The Australian dollar has been on a downward trajectory since September 2022, dropping below 62 US cents in January 2025. A combination of factors, including a strong US dollar, instability in the Chinese economy, and higher tariffs imposed by US President Trump, has contributed to the dip in the Australian dollar's value. The value of the Australian dollar is also influenced by commodity prices, which are heavily dependent on China's economy.

In assessing the impact of interest rate rises on the Australian dollar, it's important to consider the relationship between interest rates and the demand for Australian dollars. Typically, when the RBA cash rate rises, borrowing becomes more expensive for Australians, leading to reduced spending on goods and services. However, rising interest rates can make Australian assets, such as government bonds, more attractive to foreign investors, increasing the demand for Australian dollars and driving up its value. This is because these assets offer higher interest rates compared to those available in the investors' home countries.

The RBA's decision-making process considers various factors, including developments in the global economy, household spending trends, inflation, and the labour market. While a weak dollar can be a cause for concern regarding inflation, the RBA aims to balance it with the overall health of the economy.

Looking ahead, Australia's big four banks have made predictions about the movements of the RBA cash rate in 2023. ANZ and CommBank anticipate one further hike of 25 basis points in August, bringing the cash rate to a peak of 4.35%. On the other hand, NAB expects two further cash rate hikes in 2023, resulting in a peak of 4.60%. Westpac aligns with NAB's prediction of a peak cash rate of 4.60% but expects it to be reached through cash rate rises in both August and September. These predictions highlight the potential for further interest rate rises in Australia, which could have a significant impact on the Australian dollar's value.

Heathrow to Australia: Airlines Offering Direct Flights

You may want to see also

Explore related products

![]()

The outlook for inflation and the labour market

In recent years, the increase in hours worked has outpaced the growth in the capital stock, leading to a key driver of weakness in productivity. This is expected to rebalance over the next few years, contributing to a pick-up in productivity. The RBA expects underlying inflation to fall faster than previously expected, with forecasts predicting a return to the target range by 2025 and reaching the midpoint in 2026.

The labour market is also expected to remain tight, with the RBA no longer anticipating a significant loosening. The jobless rate is predicted to tick up slightly but remain relatively stable over the next few years. Labour underutilisation rates are expected to rise as employment growth moderates and average hours worked decline. However, these rates are still expected to be well below the typical rates of the past five decades.

The RBA's forecasts are based on assumptions of a cash rate remaining around the current level until mid-2024. However, there is uncertainty regarding the potential impact of global policy changes, particularly regarding trade policies with the US and China. The RBA's models also consider the possibility of overestimating the labour market's capacity and the potential for a larger decline in inflation than forecast.

Overall, the outlook for inflation and the labour market in Australia involves a delicate balance between managing inflation expectations and ensuring sustainable employment conditions. The RBA's decisions will continue to shape the trajectory of these economic indicators.

Vietjet's Australian Ambitions: Exploring New Routes Down Under

You may want to see also

Frequently asked questions

The next interest rate hike in Australia is expected to be in August 2023.

The peak interest rate is expected to be between 4.35% and 4.60%.

The current interest rate in Australia is 4.10%.

The RBA meets on the first Tuesday of every month, except for January, to decide on interest rates.

The RBA considers developments in the global economy, trends in household spending, and the outlook for inflation and the labour market when setting interest rates.