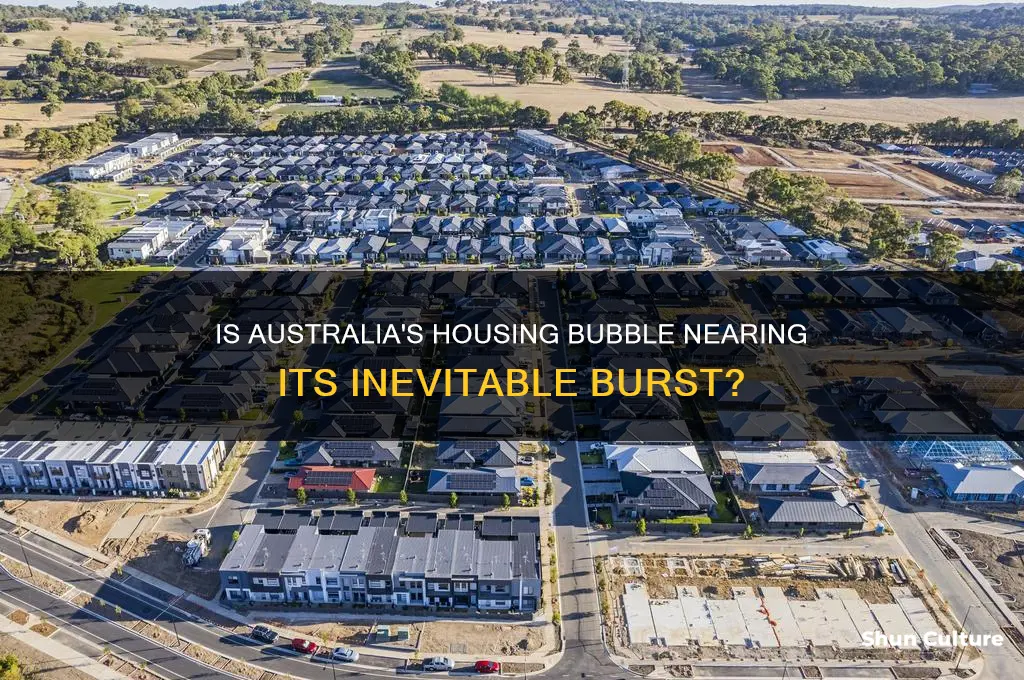

The Australian housing market has long been a subject of intense debate, with many experts and observers questioning whether the rapid price growth seen over the past decades constitutes a bubble. Fueled by low interest rates, high demand, and limited supply, property prices in major cities like Sydney and Melbourne have soared, raising concerns about affordability and sustainability. As global economic conditions shift, with rising interest rates and inflationary pressures, there is growing speculation about when—or if—the Australian housing bubble might burst. Factors such as household debt levels, wage stagnation, and potential oversupply in certain markets further complicate the outlook. While some argue that the market is due for a correction, others believe structural factors like population growth and urbanization will continue to support prices. The question remains: is Australia’s housing market on the brink of a crash, or will it withstand the pressures and maintain its resilience?

| Characteristics | Values |

|---|---|

| Current Housing Market Status | As of October 2023, the Australian housing market remains resilient, with prices in major cities like Sydney and Melbourne showing modest growth despite rising interest rates. |

| Interest Rates | The Reserve Bank of Australia (RBA) has raised the cash rate to 4.10% (as of October 2023), putting pressure on borrowers and potentially cooling demand. |

| Affordability | Housing affordability is at historic lows, with the median house price-to-income ratio exceeding 8:1 in Sydney and Melbourne, far above long-term averages. |

| Household Debt | Australia has one of the highest household debt-to-income ratios globally, at approximately 185% (as of 2023), making households vulnerable to economic shocks. |

| Unemployment Rate | The unemployment rate remains low at 3.7% (as of September 2023), supporting household incomes and mortgage repayments. |

| Economic Growth | Australia’s GDP growth has slowed to 2.1% year-on-year (as of Q2 2023), with inflation at 5.4% (as of August 2023), impacting consumer spending and housing demand. |

| Supply vs. Demand | Housing supply remains constrained, particularly in major cities, with new construction lagging behind population growth, supporting price stability. |

| Investor Activity | Investor lending has declined due to higher interest rates and tighter lending standards, reducing speculative demand in the market. |

| Government Policies | The government has introduced measures like first home buyer grants and tighter lending rules, but no significant interventions to directly address affordability or oversupply. |

| Expert Predictions | Most economists predict a soft landing rather than a burst, with price growth slowing but no major crash expected in 2023-2024, barring a severe economic downturn. |

Explore related products

What You'll Learn

![]()

Economic Indicators Predicting a Burst

The Australian housing market has long been a subject of debate, with many speculating about the possibility of a bubble and its potential burst. While predicting the exact timing of such an event is complex, several economic indicators can provide valuable insights into the market's trajectory and the likelihood of a correction. Here are some key indicators that economists and analysts monitor to assess the risk of a housing bubble burst in Australia.

Housing Affordability and Price-to-Income Ratios: One of the primary indicators of a potential housing bubble is the affordability of homes relative to income. Australia has experienced a significant increase in housing prices over the past decades, outpacing income growth. The price-to-income ratio, which compares median house prices to median household incomes, has been rising steadily. When this ratio becomes excessively high, it suggests that housing prices may be detached from fundamental affordability, indicating a possible bubble. A correction in the market could occur if prices become unsustainable for the average buyer.

Household Debt and Lending Standards: Australia boasts one of the highest household debt-to-income ratios globally, largely driven by mortgage debt. Easy access to credit and low-interest rates have encouraged borrowers to take on larger loans. However, a sudden increase in interest rates or a tightening of lending standards could put pressure on highly indebted households. If a significant number of borrowers struggle to service their debts, it may lead to forced property sales, potentially triggering a downward spiral in prices. Monitoring lending practices and debt levels is crucial in assessing the market's vulnerability.

Rental Yields and Vacancy Rates: The relationship between rental prices and property values is another essential indicator. In a healthy market, rental yields (annual rent as a percentage of the property value) should provide a reasonable return for investors. However, in a bubble, property prices can surge ahead of rents, causing yields to compress. Australia has seen declining rental yields in some major cities, indicating that investment properties may be overvalued. Additionally, vacancy rates can signal market imbalances. High vacancy rates suggest an oversupply of properties, which could lead to price corrections.

Economic Growth and Employment: The overall health of the Australian economy plays a pivotal role in the housing market's stability. Strong economic growth and low unemployment generally support housing demand. However, a slowdown in economic growth or a rise in unemployment rates might reduce buyers' purchasing power and increase the risk of mortgage defaults. A weakening economy could be a precursor to a housing market downturn, especially if it coincides with other indicators mentioned above.

Interest Rates and Monetary Policy: Monetary policy decisions by the Reserve Bank of Australia (RBA) have a direct impact on the housing market. Low-interest rates have been a significant driver of housing demand and price growth. However, as interest rates rise, borrowing becomes more expensive, potentially pricing some buyers out of the market. A series of interest rate hikes could cool down the market and even lead to a correction if not managed carefully. The RBA's actions and statements are closely watched for clues about the future direction of the housing market.

In summary, predicting the burst of a housing bubble is a complex task, but these economic indicators offer a framework for assessment. A combination of factors, including affordability, debt levels, rental market dynamics, economic growth, and monetary policy, can provide a comprehensive view of the Australian housing market's health. While a bubble burst is not inevitable, monitoring these indicators can help policymakers, investors, and homebuyers make informed decisions and prepare for potential market shifts.

Delicious Australian Red Crabs: Are They Edible?

You may want to see also

Explore related products

![]()

Impact of Rising Interest Rates

The impact of rising interest rates on the Australian housing market is a critical factor in assessing when the housing bubble might burst. As the Reserve Bank of Australia (RBA) increases the cash rate to combat inflation, the cost of borrowing for homebuyers rises significantly. This directly affects mortgage repayments, particularly for those with variable-rate loans, which constitute a substantial portion of Australian mortgages. Higher repayments reduce disposable income, leaving households with less money to spend on other goods and services. This shift can lead to a slowdown in consumer spending, which in turn may dampen economic growth and increase the risk of a recession.

For homeowners, especially those who purchased properties at the peak of the market with large loans, rising interest rates can lead to mortgage stress. Mortgage stress occurs when a significant portion of a household’s income is allocated to mortgage repayments, leaving little room for other expenses or savings. In extreme cases, this can result in defaults and forced property sales, increasing the supply of homes on the market. An oversupply, coupled with reduced demand due to higher borrowing costs, can put downward pressure on property prices, potentially triggering a correction in the housing market.

Investors, who play a significant role in the Australian property market, are also affected by rising interest rates. Higher borrowing costs reduce the attractiveness of property as an investment, as rental yields may no longer cover mortgage expenses. This could lead to a wave of investor sell-offs, further exacerbating the supply-demand imbalance and accelerating price declines. Additionally, tighter lending standards imposed by banks in response to higher rates can make it harder for investors to secure financing, reducing their ability to sustain or expand their property portfolios.

The broader economic impact of rising interest rates extends beyond individual homeowners and investors. A housing market downturn can have a ripple effect on related industries, such as construction, real estate, and financial services. Reduced property values and construction activity can lead to job losses and decreased economic output. Furthermore, falling home prices can erode household wealth, reducing consumer confidence and spending. This negative feedback loop can deepen an economic downturn, making it harder for the RBA to achieve a soft landing for the economy while addressing inflation.

Finally, the timing and magnitude of interest rate increases play a crucial role in determining the severity of the housing market correction. If rates rise gradually, households and investors may have time to adjust their finances and mitigate the impact. However, rapid or aggressive rate hikes could overwhelm borrowers, leading to a sharper and more sudden decline in property prices. Historical data suggests that prolonged periods of low-interest rates, such as those seen in Australia over the past decade, often precede significant housing market corrections when rates eventually rise. As such, the current trajectory of interest rates will be a key indicator of whether and when the Australian housing bubble might burst.

Hungry Australians: What Percentage of the Population?

You may want to see also

Explore related products

![]()

Oversupply in Major Cities

The Australian housing market has long been a subject of debate, with many speculating about the potential bursting of its perceived bubble. One critical factor contributing to this discussion is the oversupply in major cities, which has become a significant concern for economists, investors, and homeowners alike. Major cities like Sydney, Melbourne, and Brisbane have experienced rapid population growth over the past decade, driving a construction boom to meet housing demand. However, recent data suggests that the supply of new apartments and houses has outpaced population growth, leading to an oversupply situation. This imbalance is particularly evident in inner-city areas, where high-rise apartment developments dominate the skyline. As a result, vacancy rates have risen, putting downward pressure on rental yields and property prices.

The consequences of oversupply are already manifesting in softening property prices and reduced investor confidence. In cities like Melbourne and Sydney, apartment prices have stagnated or declined in certain areas, particularly where supply is most concentrated. This trend is concerning for investors who purchased off-the-plan properties, as they now face challenges in settling their purchases due to valuation shortfalls. Banks have also become more cautious, tightening lending criteria for apartments in oversupplied areas, which further restricts demand. If left unaddressed, this oversupply could contribute to a broader correction in the housing market, potentially accelerating the bursting of the bubble.

Addressing oversupply in major cities requires a multi-faceted approach. Local governments must reassess development approvals to align with current and projected demand, avoiding further exacerbation of the issue. Incentives for affordable housing and urban renewal projects could help absorb excess supply while addressing housing affordability challenges. Additionally, policies to stimulate population growth, such as targeted immigration programs, could help restore balance between supply and demand. For investors and homeowners, diversification away from oversupplied areas and a focus on properties with strong fundamentals, such as proximity to amenities and employment hubs, is advisable.

In conclusion, oversupply in major cities is a critical factor in the ongoing debate about the Australian housing bubble. The mismatch between supply and demand, driven by excessive development and shifting buyer preferences, poses risks to property prices and market stability. While the situation is not uniform across all cities or property types, the concentration of oversupply in inner-city areas is a clear warning sign. Proactive measures from policymakers, developers, and investors are essential to mitigate the impact and prevent a broader market downturn. As the housing market continues to evolve, monitoring oversupply trends will be key to understanding when and how the bubble might burst.

Where Does Australia's Money Go?

You may want to see also

Explore related products

![]()

Government Policies and Market Stability

The Australian housing market has long been a subject of debate, with many speculating about the possibility of a housing bubble and its potential burst. Government policies play a pivotal role in maintaining market stability and preventing drastic fluctuations that could lead to a bubble bursting. One of the key measures is the implementation of macroprudential policies, which aim to mitigate risks in the financial system. These policies often include tighter lending standards, such as higher loan-to-value ratios (LVRs) and stricter income verification processes. By ensuring that borrowers are more creditworthy, the government can reduce the likelihood of widespread defaults that could destabilize the housing market.

Another critical aspect of government intervention is the regulation of interest rates. The Reserve Bank of Australia (RBA) has historically used monetary policy to influence housing demand. Lower interest rates can stimulate borrowing and increase property prices, while higher rates can cool down an overheating market. However, the RBA must balance these adjustments carefully to avoid triggering a sudden market correction. For instance, a rapid increase in interest rates could lead to a surge in mortgage repayments, potentially causing financial distress for homeowners and a subsequent decline in property values.

Fiscal policies also contribute significantly to market stability. The Australian government has introduced various schemes to support homeownership, such as the First Home Owner Grant and the First Home Loan Deposit Scheme. While these initiatives aim to improve housing affordability, they can inadvertently inflate demand and drive up prices if not carefully calibrated. Policymakers must ensure that such programs are targeted and temporary to avoid exacerbating market imbalances. Additionally, addressing supply-side constraints through zoning reforms and infrastructure investments can help align housing supply with demand, reducing upward pressure on prices.

Taxation policies are another tool in the government’s arsenal to stabilize the housing market. Changes to capital gains tax, negative gearing, and stamp duty can influence investor behavior and overall market dynamics. For example, reforms to negative gearing could discourage speculative investment, while reductions in stamp duty might stimulate transaction activity. However, any tax policy changes must be implemented gradually to avoid shocking the market. A sudden shift could lead to a rapid withdrawal of investors, causing property prices to plummet and potentially triggering a bubble burst.

Finally, transparency and data-driven decision-making are essential for effective government intervention. Regular monitoring of housing market indicators, such as price-to-income ratios, debt-to-income levels, and vacancy rates, allows policymakers to identify emerging risks early. By staying informed and responsive, the government can implement timely measures to prevent market overheating or collapse. Collaboration between federal, state, and local authorities is also crucial, as housing markets vary significantly across regions, requiring tailored solutions. In conclusion, government policies are instrumental in maintaining the stability of the Australian housing market, and their careful design and execution are vital to avoiding a potential bubble burst.

Bras Down Under: Smallest Australian Cup Size

You may want to see also

Explore related products

![]()

Global Economic Influences on Housing

The Australian housing market has long been a subject of debate, with many speculating about the potential bursting of its perceived bubble. While domestic factors like supply and demand, interest rates, and government policies play a significant role, global economic influences are equally critical in shaping the trajectory of Australia's housing market. One of the most significant global factors is the international monetary policy, particularly that of major central banks like the U.S. Federal Reserve. When global interest rates rise, as they have in recent years to combat inflation, it often leads to higher borrowing costs in Australia. This is because Australian banks rely on international funding markets, and tighter global liquidity conditions can increase the cost of credit domestically. Higher interest rates can dampen housing demand by making mortgages less affordable, potentially cooling the market and contributing to a correction.

Another key global influence is the strength of the Australian dollar (AUD), which is closely tied to commodity prices and global economic sentiment. Australia’s economy is heavily reliant on exports, particularly minerals and energy resources. When global demand for these commodities is high, the AUD tends to strengthen, making imports cheaper and potentially easing inflationary pressures. However, a strong AUD can also attract foreign investment into the housing market, driving up prices. Conversely, a weakening AUD, often driven by global economic downturns or reduced demand for commodities, can deter foreign buyers and reduce investment inflows, putting downward pressure on housing prices.

Global economic growth and geopolitical events also play a pivotal role in Australia’s housing market. Strong global growth typically boosts demand for Australian exports, strengthens the economy, and supports higher housing prices. However, global recessions or economic slowdowns, such as those triggered by events like the COVID-19 pandemic or geopolitical tensions, can reduce demand for Australian goods and services, weaken the economy, and lead to job losses. This, in turn, can reduce household income and confidence, causing a decline in housing demand and prices. For instance, a global recession could lead to a wave of mortgage defaults and forced property sales, accelerating a potential housing market correction in Australia.

Inflation and global supply chain disruptions are additional factors that influence the Australian housing market. Global inflationary pressures, driven by supply chain bottlenecks, rising energy costs, and increased commodity prices, can lead to higher construction costs in Australia. This makes new housing supply more expensive, exacerbating affordability issues and potentially cooling demand. Moreover, if global inflation persists, central banks worldwide may adopt more aggressive monetary tightening policies, which could spill over into Australia’s economy and housing market. Higher inflation also erodes purchasing power, making it harder for households to afford mortgages, even if interest rates remain stable.

Finally, global investor sentiment and capital flows significantly impact Australia’s housing market. During periods of global economic uncertainty, investors often seek safe-haven assets, and Australian real estate has historically been viewed as a stable investment. This can drive up property prices, particularly in major cities like Sydney and Melbourne. However, if global investor sentiment shifts—for example, due to more attractive opportunities elsewhere or concerns about an Australian housing bubble—capital outflows could occur, leading to a rapid decline in property prices. Thus, the interplay between global economic conditions and investor confidence remains a critical determinant of the Australian housing market’s stability and the likelihood of a bubble bursting.

In conclusion, while domestic factors are central to the Australian housing market, global economic influences are equally important in determining its future. International monetary policy, currency movements, global economic growth, inflation, and investor sentiment all interact to shape housing demand, affordability, and prices in Australia. Understanding these global dynamics is essential for predicting when—or if—the Australian housing bubble might burst. As the global economy continues to evolve, its impact on Australia’s housing market will remain a key area of focus for policymakers, investors, and homeowners alike.

A Guide to Applying for ISBN in Australia

You may want to see also

Frequently asked questions

Predicting when a housing bubble will burst is highly speculative and depends on various economic factors such as interest rates, employment, supply and demand, and government policies. While some experts warn of a potential correction, others argue the market is supported by strong fundamentals. There is no definitive timeline, and it’s essential to monitor economic indicators closely.

Key indicators include rapidly rising interest rates, declining affordability, oversupply of housing, increasing unemployment, and a significant drop in buyer demand. Additionally, a surge in distressed sales or defaults could signal trouble. However, these factors often occur in combination, and their impact varies across regions.

To mitigate risks, ensure you have a manageable mortgage with a buffer for higher repayments, maintain a diversified investment portfolio, and avoid over-leveraging. Renting instead of buying could be a safer option in an uncertain market. Staying informed about economic trends and seeking professional financial advice is also crucial.

![Crash [4K UHD]](https://m.media-amazon.com/images/I/61jWrMRaC8S._AC_UY218_.jpg)

![Crash [DVD]](https://m.media-amazon.com/images/I/91vI1JyeFpL._AC_UY218_.jpg)

![Crash [4K UHD]](https://m.media-amazon.com/images/I/71ljRZS73xL._AC_UY218_.jpg)