In Australia, determining the appropriate percentage of income that should go towards rent is a critical financial consideration for both renters and policymakers. Traditionally, the 30% rule has been widely accepted as a benchmark, suggesting that individuals or households should allocate no more than 30% of their gross income to housing costs. However, skyrocketing rental prices in major cities like Sydney and Melbourne, coupled with stagnant wage growth, have made this guideline increasingly unattainable for many Australians. As a result, a growing number of renters are spending significantly more than 30% of their income on rent, leading to financial stress and housing insecurity. This disparity highlights the need for a reevaluation of affordability metrics and potential policy interventions to address the housing crisis in Australia.

Explore related products

What You'll Learn

- Affordable Rent Benchmarks: Guidelines for determining a sustainable rent-to-income ratio in Australia

- Regional Variations: How rent percentages differ across major Australian cities and rural areas

- Budgeting Tips: Strategies to manage rent costs within recommended income percentages

- Government Assistance: Available subsidies and programs to ease rental burdens in Australia

- Market Trends: Current rental affordability challenges and their impact on income allocation

![]()

Affordable Rent Benchmarks: Guidelines for determining a sustainable rent-to-income ratio in Australia

When determining a sustainable rent-to-income ratio in Australia, it is essential to consider benchmarks that ensure housing remains affordable without compromising other essential living expenses. A widely accepted guideline is that no more than 30% of gross household income should be allocated to rent. This benchmark, often referred to as the "30% rule," is endorsed by financial experts and housing advocates as a threshold for affordability. Exceeding this ratio can lead to financial stress, making it difficult for individuals and families to cover other necessities like food, healthcare, and utilities. This guideline is particularly relevant in Australia, where housing costs have been rising steadily, outpacing income growth in many regions.

However, the 30% rule is not a one-size-fits-all solution. Regional variations in rental markets and income levels necessitate a more nuanced approach. For instance, in high-cost cities like Sydney and Melbourne, where rents are significantly higher than the national average, households may struggle to stay within the 30% threshold. In such cases, a 25% rent-to-income ratio might be more realistic for long-term financial sustainability. Conversely, in regional areas with lower living costs, a slightly higher ratio, up to 35%, could be manageable, provided it aligns with the household’s overall budget and financial goals.

Another critical factor to consider is the distinction between gross and net income. While the 30% rule typically applies to gross income (pre-tax earnings), households should also assess their net income (take-home pay) to ensure rent remains affordable after taxes and other deductions. For example, if a household’s gross income is $80,000 annually, the 30% rule suggests a maximum rent of $2,000 per month. However, if their net income is significantly lower due to taxes, superannuation contributions, or other deductions, they may need to adjust their rent budget accordingly to avoid financial strain.

For low-income earners and vulnerable populations, the 30% benchmark may still be unattainable. In these cases, 20% or less of income should ideally be spent on rent to ensure financial stability. Governments and housing providers can play a crucial role by offering subsidies, rent assistance programs, or affordable housing initiatives to bridge the gap. Additionally, households should prioritize creating a comprehensive budget that accounts for all expenses, including savings and debt repayments, to determine a rent-to-income ratio that aligns with their unique financial circumstances.

Finally, it is important to monitor and adjust rent-to-income ratios over time. Life circumstances, such as job changes, family expansions, or economic fluctuations, can impact affordability. Regularly reviewing rental expenses in relation to income ensures that housing remains sustainable in the long term. Tools like budgeting apps or financial planners can assist households in tracking their spending and making informed decisions about rent affordability. By adhering to these guidelines, Australians can better navigate the rental market and secure housing that supports their overall financial well-being.

Australian Shoe Size: US 8 Conversion

You may want to see also

Explore related products

![]()

Regional Variations: How rent percentages differ across major Australian cities and rural areas

In Australia, the percentage of income allocated to rent varies significantly across different regions, influenced by factors such as housing demand, local economies, and population density. Major cities like Sydney and Melbourne consistently report higher rent-to-income ratios due to their thriving job markets and limited housing supply. In Sydney, for instance, tenants often spend upwards of 30% of their income on rent, with some households exceeding 40% in highly sought-after suburbs. Melbourne follows closely, with renters typically allocating around 28-32% of their earnings to housing costs. These figures highlight the financial strain on urban dwellers, where the cost of living is among the highest in the country.

In contrast, regional cities like Brisbane, Adelaide, and Perth offer more affordable rental markets, allowing residents to spend a smaller portion of their income on housing. In Brisbane, renters generally allocate about 25-28% of their income to rent, while in Adelaide, this figure drops to around 22-25%. Perth, despite its economic fluctuations, maintains a rent-to-income ratio of approximately 24-27%. These cities benefit from a better balance between housing supply and demand, making them more accessible for middle-income earners.

Rural and remote areas in Australia present a different picture, with rent-to-income percentages varying widely based on local conditions. In some regional towns, particularly those with strong agricultural or mining industries, rental costs can be relatively low, allowing residents to spend as little as 15-20% of their income on housing. However, in areas with limited employment opportunities or seasonal work, renters may face higher proportions due to lower incomes rather than elevated rents. For example, in remote Queensland or Western Australia, tenants might still spend 25-30% of their income on rent despite lower absolute costs, as wages in these areas are often lower.

Tourist-heavy regions, such as the Gold Coast or Tasmania, exhibit unique rental dynamics. During peak seasons, rental prices surge, pushing rent-to-income ratios higher for locals, while off-peak periods may offer more affordable options. On the Gold Coast, renters might spend 28-32% of their income on housing, whereas in Tasmania, the figure ranges from 22-26%. These variations underscore the importance of considering seasonal fluctuations when assessing rental affordability in such areas.

Understanding these regional differences is crucial for individuals planning to relocate or manage their finances effectively. While the general guideline suggests allocating no more than 30% of income to rent, this threshold is often exceeded in major cities, necessitating careful budgeting. In contrast, regional and rural areas may offer more flexibility, but local economic conditions must be factored into housing decisions. By analyzing these variations, Australians can make informed choices about where to live and how to balance their housing expenses with other financial priorities.

Takeaway Treats: Aussies' Favorite Food Orders

You may want to see also

Explore related products

![]()

Budgeting Tips: Strategies to manage rent costs within recommended income percentages

In Australia, financial experts generally recommend that rent should not exceed 30% of your gross income to maintain a balanced budget. This guideline ensures that you have enough funds left for other essential expenses, savings, and leisure. However, with rising rental costs in major cities like Sydney and Melbourne, staying within this threshold can be challenging. To manage rent costs effectively, it’s crucial to adopt strategic budgeting practices that align with this recommended percentage.

One of the most effective strategies is to prioritize location and housing type. Living in high-demand areas often comes with higher rent, so consider suburbs or neighborhoods slightly further from the city center where costs may be lower. Additionally, opting for shared housing or smaller accommodations can significantly reduce rental expenses. For example, renting a room in a shared house instead of a one-bedroom apartment can save hundreds of dollars monthly, making it easier to stay within the 30% income threshold.

Another key tip is to negotiate rent with your landlord. If you’re a reliable tenant with a good payment history, landlords may be willing to lower the rent or offer more favorable terms to retain you. Researching local rental market trends can also strengthen your negotiation position. For instance, if similar properties in the area are listed at lower rates, use this information to request a reduction. Even a small decrease can make a meaningful difference in aligning your rent with the recommended income percentage.

Creating a detailed budget that includes rent as a fixed expense is essential for financial management. Start by calculating 30% of your gross income and ensure your rent does not exceed this amount. Allocate the remaining funds to other necessities like utilities, groceries, transportation, and savings. Tools like budgeting apps or spreadsheets can help track spending and identify areas where you can cut back to accommodate higher rent if necessary. For example, reducing dining out or subscription services can free up additional funds to stay within your rental budget.

Finally, building an emergency fund is a proactive way to manage rent costs during unexpected financial setbacks. Aim to save at least three months’ worth of living expenses, including rent, to provide a safety net in case of job loss or other emergencies. This fund ensures that you can continue meeting your rental obligations without derailing your overall financial stability. By combining these strategies, you can effectively manage rent costs within the recommended income percentages and achieve a more secure financial future.

Remitting Money from India to Australia: A Guide

You may want to see also

Explore related products

$15.99 $15.99

![]()

Government Assistance: Available subsidies and programs to ease rental burdens in Australia

In Australia, it is generally recommended that individuals and families allocate no more than 30% of their gross income to rent to maintain financial stability. However, rising rental costs in many parts of the country have made this challenging for low to moderate-income earners. To address this issue, the Australian government, along with state and territory governments, offers various subsidies and programs aimed at easing rental burdens. These initiatives are designed to ensure that housing remains affordable for vulnerable populations, including low-income families, seniors, and individuals with disabilities.

One of the most significant government assistance programs is Commonwealth Rent Assistance (CRA), a fortnightly payment provided through Centrelink to eligible recipients. CRA is available to those who receive income support payments, such as the Age Pension, Disability Support Pension, or JobSeeker Payment, and who pay rent in the private rental market. The amount of CRA received depends on income, family situation, and the amount of rent paid, with higher payments for those with greater rental expenses. This subsidy helps bridge the gap between income and rental costs, making housing more affordable for those on fixed or low incomes.

At the state and territory level, additional programs complement federal assistance. For example, social housing initiatives, including public housing and community housing, offer subsidised rent to eligible individuals and families. Public housing is managed by state governments and provides long-term, secure housing at reduced rents, typically set at 25-30% of the tenant’s income. Community housing, managed by not-for-profit organisations, operates similarly and often includes support services for tenants. These programs are particularly vital for those who cannot afford market rents and require stable housing solutions.

Another key initiative is the National Rental Affordability Scheme (NRAS), which incentivises investors to build and rent out properties at below-market rates. While NRAS is no longer accepting new properties, existing participants continue to provide affordable rental options for low to moderate-income households. Tenants under NRAS pay rent that is at least 20% below market rates, significantly reducing their housing costs. This program highlights the government’s commitment to increasing the supply of affordable rental properties.

For first-time homebuyers transitioning from renting, the First Home Owner Grant (FHOG) and First Home Loan Deposit Scheme (FHLDS) provide financial assistance to enter the property market. While these programs do not directly reduce rental burdens, they offer a pathway to homeownership, which can alleviate long-term housing costs. Additionally, some states and territories offer rental grants or bonds assistance to help with upfront costs, such as rental bonds, further easing the financial strain of moving into a new property.

Lastly, state-specific programs provide targeted support in regions with acute housing affordability issues. For instance, New South Wales offers the Housing Assistance Program, which includes rent subsidies and support for tenants at risk of homelessness. Similarly, Victoria’s Private Rental Assistance Program (PRAP) provides financial assistance to eligible households to cover rental gaps. These programs demonstrate the tailored approach taken by state governments to address local rental challenges. By leveraging these subsidies and programs, Australians can better manage their rental expenses and maintain financial stability within the recommended 30% income threshold.

Helping Australian Wildlife: Your Donations Count

You may want to see also

Explore related products

![]()

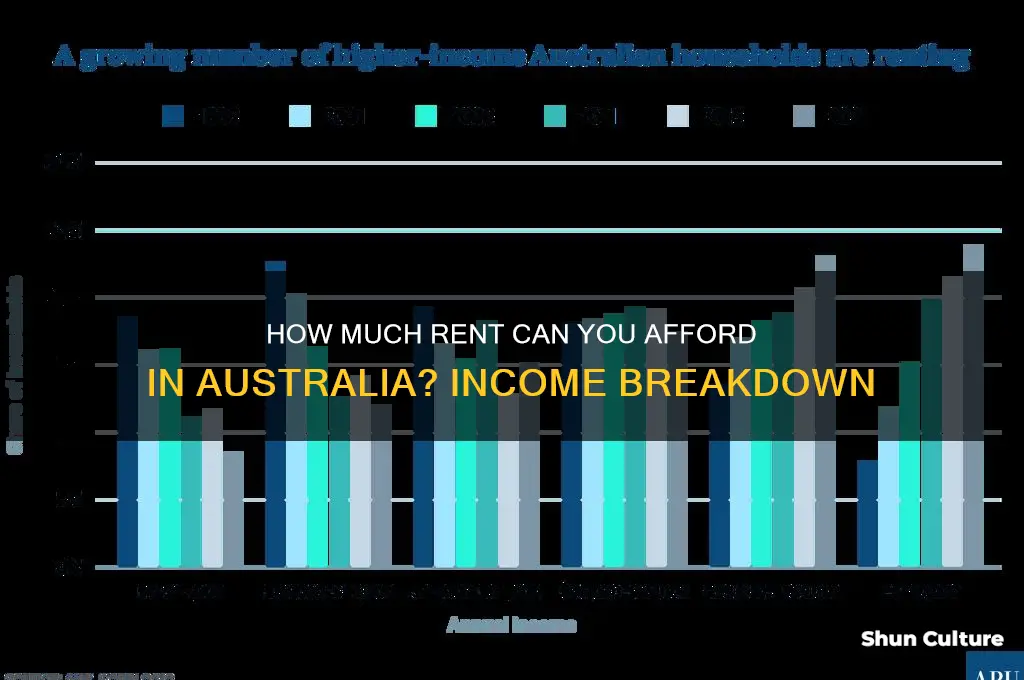

Market Trends: Current rental affordability challenges and their impact on income allocation

The current rental market in Australia is characterized by significant affordability challenges, which are reshaping how individuals and families allocate their income. According to recent guidelines, a commonly recommended benchmark is that no more than 30% of gross income should be spent on rent to maintain financial stability. However, soaring rental prices in major cities like Sydney, Melbourne, and Brisbane are pushing many households beyond this threshold. Data from Domain and SQM Research indicates that rental vacancy rates have hit historic lows, driving up costs and leaving tenants with limited options. As a result, a growing number of Australians are forced to allocate closer to 40-50% of their income to housing, leaving less for essentials like food, healthcare, and savings.

One of the key drivers of this trend is the imbalance between supply and demand. Population growth, particularly in urban areas, has outpaced the construction of new rental properties. Additionally, rising interest rates have discouraged property investors, further reducing the availability of rental stock. This scarcity has empowered landlords to increase rents, often at rates exceeding wage growth. For instance, in Sydney, median weekly rents have surged by over 20% in the past two years, far outstripping the average salary increase. Such disparities are forcing renters to make difficult trade-offs, often at the expense of long-term financial health.

The impact of these challenges is particularly severe for low- to middle-income earners, who are disproportionately affected by rising rents. Many are being priced out of desirable neighborhoods, forced to relocate to more affordable but less convenient areas, or to share housing with others to split costs. This not only affects quality of life but also exacerbates issues like commuting costs and access to services. Furthermore, the increasing share of income allocated to rent reduces the capacity to save for home ownership, perpetuating the cycle of rental dependency and widening the wealth gap.

Another consequence of these market trends is the strain on government resources and social services. As more households struggle to meet rental payments, there is a growing demand for rental assistance programs and social housing. However, these initiatives are often underfunded and unable to keep pace with the scale of the problem. This has led to calls for policy interventions, such as rent caps, incentives for property developers, and reforms to tenancy laws, to address the affordability crisis. Without such measures, the current trajectory risks deepening housing inequality and undermining economic stability.

In conclusion, the current rental affordability challenges in Australia are significantly altering income allocation patterns, with many households spending well above the recommended 30% on rent. These trends are driven by supply shortages, rising costs, and stagnant wage growth, disproportionately affecting lower-income earners. The consequences extend beyond individual financial stress to broader societal issues, including increased reliance on government support and diminished opportunities for home ownership. Addressing these challenges requires a multifaceted approach, combining short-term relief measures with long-term strategies to boost housing supply and ensure equitable access to affordable rentals.

Dasani Water: Australia's Ban Explained

You may want to see also

Frequently asked questions

A common guideline is to spend no more than 30% of your gross income on rent, as recommended by financial experts and housing affordability standards.

No, it’s a general guideline. Individual circumstances, such as location, income level, and lifestyle, may require adjustments to this percentage.

Spending more than 30% on rent can lead to financial stress, reduced savings, and difficulty covering other essential expenses like food, utilities, and transportation.

The 30% rule is a national guideline, but high-cost cities like Sydney and Melbourne may make it challenging to adhere to this rule due to higher rental prices.

Multiply your monthly gross income by 0.30. For example, if your monthly income is $5,000, 30% would be $1,500, which is the maximum recommended rent amount.