The Reserve Bank of Australia (RBA) is responsible for adjusting the official cash rate to prevent runaway inflation and create conditions for price stability. After years of hikes, the RBA finally cut rates in February 2025, but opinions are divided on whether further cuts can be expected. This article will explore the latest forecasts and projections for Australian interest rates, including the impact of economic factors such as inflation, GDP growth, and consumer spending. We will also examine the predictions made by economists and financial institutions to provide insight into the potential trajectory of interest rates in Australia.

Explore related products

What You'll Learn

![]()

The role of the Reserve Bank of Australia (RBA)

The Reserve Bank of Australia (RBA) is Australia's central bank. Its role is set out in the Reserve Bank Act 1959. The RBA is responsible for conducting the nation's monetary policy and issuing its currency. The RBA seeks to foster financial system stability and promote the safety and efficiency of the payments system. It also offers banking services to the Australian government.

The RBA's monetary policy decisions are made with the goal of achieving price stability and maintaining full employment in Australia. The RBA achieves this by setting the cash rate, which is the interest rate on overnight loans in the money market. These decisions have a ripple effect on other market and institutional interest rates. For example, when the RBA raised the official cash rate in May 2022 to curb rising inflation, Australian banks and lenders followed suit, increasing the interest rates charged on variable-rate home loans.

The RBA also plays a role in maintaining the stability of the financial system as a whole. It collaborates with other financial regulators, such as the Australian Prudential Regulation Authority, the Australian Securities and Investment Commission, and the Australian Treasury, to identify and address risks in the financial system. In extreme cases, the RBA can provide liquidity support to sound financial institutions facing temporary difficulties.

Additionally, the RBA operates the payment system that facilitates the movement of money between banks in Australia. It continuously explores innovations to enhance the efficiency and security of payments. For instance, the RBA collaborated with banks to develop the New Payments Platform, enabling near-real-time transactions around the clock.

The RBA is a body corporate wholly owned by the Commonwealth of Australia. The Reserve Bank Board, consisting of up to nine members, makes the monetary policy decisions. This includes the RBA Governor (Chair), the Deputy Governor (Deputy Chair), and the Secretary to the Treasury as ex officio members. The Board has substantial independence from the government to set policies promoting economic prosperity and the welfare of Australians.

Free University Education: Australia's Future Advantage

You may want to see also

Explore related products

![]()

The impact of inflation

Interest rates and inflation are deeply intertwined. Inflation affects interest rates in Australia, and the RBA's decisions on interest rates are influenced by inflation forecasts.

The RBA sets the 'cash rate target', which is the rate on overnight loans between banks. This influences the interest rates set by lenders, banks, and financial institutions across the country. The RBA aims to keep inflation within an annual target range of 2-3%. When inflation is high, the RBA typically raises interest rates to curb consumer spending. Higher interest rates discourage spending and incentivize saving, reducing demand and allowing prices to stabilize.

On the other hand, when the RBA lowers interest rates, consumers are more inclined to spend and take out loans. This increases demand for goods and services, potentially leading to businesses raising prices to take advantage of the market.

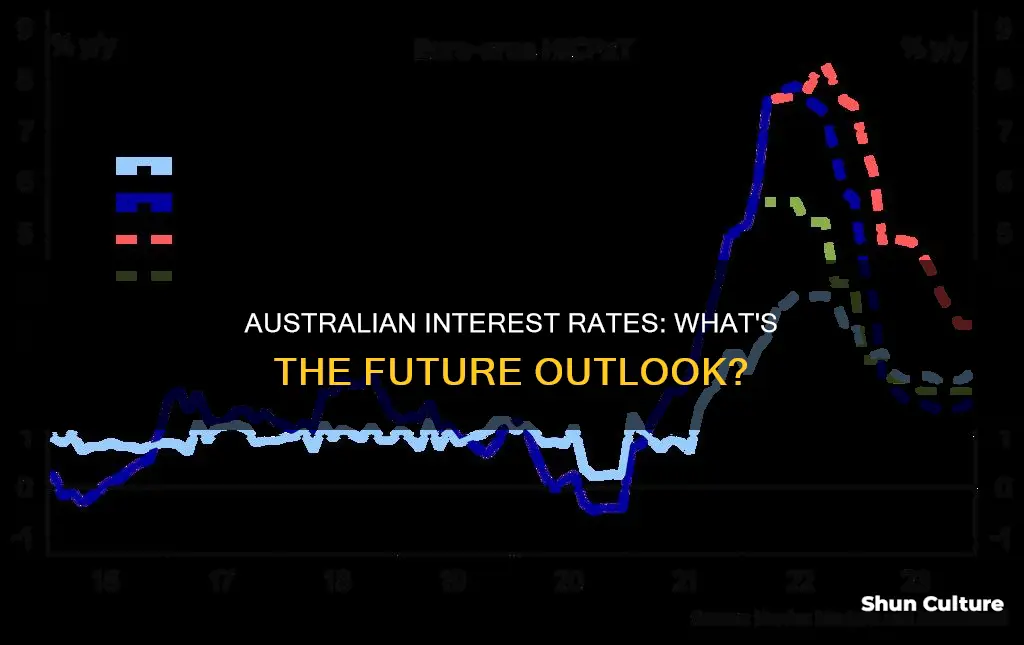

In May 2022, the RBA raised the cash rate to tackle rising inflation, and it has continued to rise since then, with the RBA governor Philip Lowe suggesting the possibility of further hikes. However, in May 2025, underlying inflation fell below 3% for the first time in three years, raising expectations of interest rate cuts.

Banks initially benefit from higher interest rates through higher Net Interest Margin (NIM). However, severe inflation may lead to reduced volumes and increased costs. The Australian banking sector is generally well-capitalized, but the current high inflation environment is unprecedented in the last decade of declining interest rates.

Australia's Violent Crime Rates: A Troubling Trend

You may want to see also

Explore related products

![]()

The effect on homeowners and investors

The impact of interest rate changes in Australia has been varied for homeowners and investors. The RBA's decision to hold the cash rate steady at 4.1% in April 2025 provided a temporary relief for mortgage holders, but the high-interest rate environment has been challenging for many. Homeowners with variable-rate mortgages have faced significantly higher costs compared to the start of 2022, and some have turned to interest-only repayments to retain their homes.

The RBA's rate hikes have been aimed at tackling inflation, which has embedded itself in the expectations of individuals and companies, distorting decision-making. The central bank has a challenging task, as it must balance controlling inflation and supporting economic growth. The RBA has warned of the consequences of failing to return to target inflation levels, which may require even higher interest rates in the future.

For investors, the high-interest rate environment has presented opportunities. Seasoned property investors with long-term views can benefit from less competition as they strategically enter the market, anticipating that rate cuts will eventually reignite price growth. However, some investors may struggle with the current rates, and refinancing may not be an option for those already servicing debt.

Looking ahead, predictions for interest rates in 2025 vary. Some economists expect rate cuts as early as May 2025, while others foresee gradual cuts throughout the year or a delay until late 2025 or early 2026. The RBA has pushed back its timeline for returning to target inflation, and its actions will depend on factors like inflation control, economic growth, and employment.

Homeowners can consider options like making extra repayments, utilising offset accounts, or refinancing to manage their loans. The impact of interest rates on investors' portfolios and strategies will depend on their risk appetite and ability to weather the current financial climate.

The Unique Nature of Australian Flying Foxes

You may want to see also

Explore related products

![]()

The influence of the global economic outlook

The global economic outlook is expected to have a significant influence on Australian interest rates. Global growth is predicted to be subdued over the next two years, which will likely result in slower growth in demand for Australian goods and services. This is partly due to tighter monetary policies and slower GDP growth in advanced economies.

The outlook for global economic growth remains uncertain, with risks tilted to the downside. Weaker global consumer and investor confidence will further dampen demand for Australian exports. Additionally, the expected slowing of China's growth creates uncertainty around the demand for commodities, including Australia's key exports. The outlook for household consumption in China remains weak, which could negatively impact Australia's education and tourism exports.

However, China's economic stimulus package has led to increased demand for mineral ores, benefiting Australian exports. This has also resulted in a surge in mining commodity prices, particularly for iron ore, contributing to the overall growth of private non-financial corporations in Australia.

The depreciation of the Australian dollar can also play a role in adjusting to negative foreign shocks or increased global risk aversion, improving Australia's international competitiveness and boosting export demand.

Overall, the global economic outlook is expected to contribute to softer economic growth in Australia, with slower demand growth and potential impacts on interest rates.

Converting Euros to Australian Dollars: 45 Euro Equals?

You may want to see also

Explore related products

![]()

The possibility of further rate hikes or cuts

The decision to raise or cut interest rates is influenced by the RBA's mandate to prevent runaway inflation and create conditions for "price stability." The RBA's official cash rate is a crucial tool in achieving this goal, impacting the interest rates offered by banks and other lenders. In February 2025, the RBA cut the official cash rate by 25 basis points to 4.10%first rate reduction since November 2020. This move was expected by markets, and the RBA adopted a wait-and-see approach, citing easing inflation and evolving underlying price pressures.

Opinions are divided on the possibility of further rate cuts. Some economists and banks predict additional rate cuts in 2025, with a slow easing cycle expected. HSBC Chief Economist Paul Bloxham, for example, forecasts two cuts as the RBA supports the economy. On the other hand, AMP Chief Economist Shane Oliver anticipates three rate cuts in 2025. These predictions are based on factors like trade policy changes, the potential impact of Trump tariffs, and the RBA's cautious approach to normalising the cash rate.

However, it's important to recognise that forecasting is challenging, as evidenced by the 'big four' banks having to push back their estimates of rate cuts multiple times in 2024. Additionally, the Australian economy's growth has slowed down, which bolsters the case for further rate cuts in mid-2025. A robust economy supported by GDP growth typically justifies lowering interest rates. The RBA also forecasts a recovery in consumer spending, stabilising at the estimated historical trend growth rate by the end of 2025, but at a softer rate than previously predicted.

While the RBA's priority is to return inflation to the target range of 2-3%, they must also consider the potential impact on unemployment. As governor Philip Lowe stated, "if high inflation were to become entrenched in people's expectations, it would be very costly to reduce later, involving even higher interest rates and a larger rise in unemployment." Therefore, the RBA must carefully navigate the path of achieving a "soft landing" for the economy while managing inflation expectations.

Earning Virgin UK-Australia Miles: The Long-Haul Reward

You may want to see also

Frequently asked questions

As of July 2023, the interest rate in Australia is 4.10%, which was set in June 2023.

The forecast for Australian interest rates in 2025 is divided. Some believe there will be continued easing, with rates dropping below 3.5%. However, others predict short-term rate hikes if inflation increases.

The RBA is responsible for preventing runaway inflation and creating conditions for price stability. It uses the official cash rate as a tool to influence the interest rates offered by banks and lenders. The RBA also considers factors such as inflation, economic growth, consumer spending, and employment numbers when making decisions about interest rates.

Changes in the RBA's interest rates can impact homeowners and investors in different ways. Homeowners with variable-rate mortgages may see their repayments increase or decrease. Property investors may also be affected by changes in borrowing power. Equity investors may experience fluctuations in the value of their stock portfolios due to RBA rate adjustments.