The return on Australian government bonds is referred to as the yield. The yield curve for government bonds is an important indicator in financial markets, reflecting economic confidence and investor sentiment. It helps determine how actual and expected changes in the policy interest rate and other monetary policy tools impact a broad range of interest rates in the economy. The yield on Australian government bonds varies depending on the duration, with longer-duration interest rates typically higher than short-duration rates, resulting in a positive spread between longer and shorter bonds. Coupon Interest Rates on Treasury Bonds are fixed when issued and remain constant throughout the bond's life, while the Yield to Maturity fluctuates with changes in price and the remaining term.

| Characteristics | Values |

|---|---|

| Coupon Interest Rate | Set when the bond is first issued by the Australian Government and remains fixed for the life of the bond. |

| Coupon Interest Payments | Paid every six months. |

| Yield | The return an investor expects to receive each year over its term to maturity. |

| Yield Curve | A graph that shows the relationship between interest rates (or yields) and different maturities of debt for a specific borrower, often government bonds. |

| Bond Yield | Reflects the annual cost of borrowing by issuing a new bond. |

| Current Yield on 10-Year Government Bond | Not available. |

Explore related products

What You'll Learn

![]()

The yield curve and its influence on interest rates

A yield curve is a visual representation of the relationship between interest rates and different debt maturities for a specific borrower, often the government. It is an important economic indicator as it reflects market expectations about future interest rates, economic growth and inflation over time. Typically, the yield curve is upward-sloping, with longer-duration interest rates being higher than short-duration rates. This is because lenders and investors who commit for longer periods demand extra compensation for the added uncertainty and the risk of economic shifts over time. This extra compensation is known as the term premium.

The yield curve is a useful benchmark for other debts in the financial market, such as mortgage rates and bank lending rates. It is also used by investors to make investment decisions based on the likely direction of bond rates. For instance, a steep yield curve, indicating strong economic growth, may encourage investors to choose riskier assets, while a flat or inverted yield curve may signal a defensive strategy.

The yield curve is influenced by changes in monetary policy, such as negative interest rates or forward guidance. For example, during the Global Financial Crisis, the Federal Reserve's quantitative easing policy depressed the term premium. Additionally, the yield curve itself can influence interest rates in the economy. When households, firms, or governments borrow funds by issuing bonds, the cost of borrowing depends on the level and slope of the yield curve.

The slope of the yield curve is a leading indicator of future economic growth and inflation. A normal, upward-sloping curve indicates economic expansion, while a downward-sloping curve, which is rare, signals an economic recession. A flat yield curve implies an uncertain economic situation, where investors are unsure about the future direction of interest rates and the economy.

Tantalum Sources in Australia: Exploring Local Deposits and Mines

You may want to see also

Explore related products

![]()

Coupon Interest Rates and Coupon Interest Payments

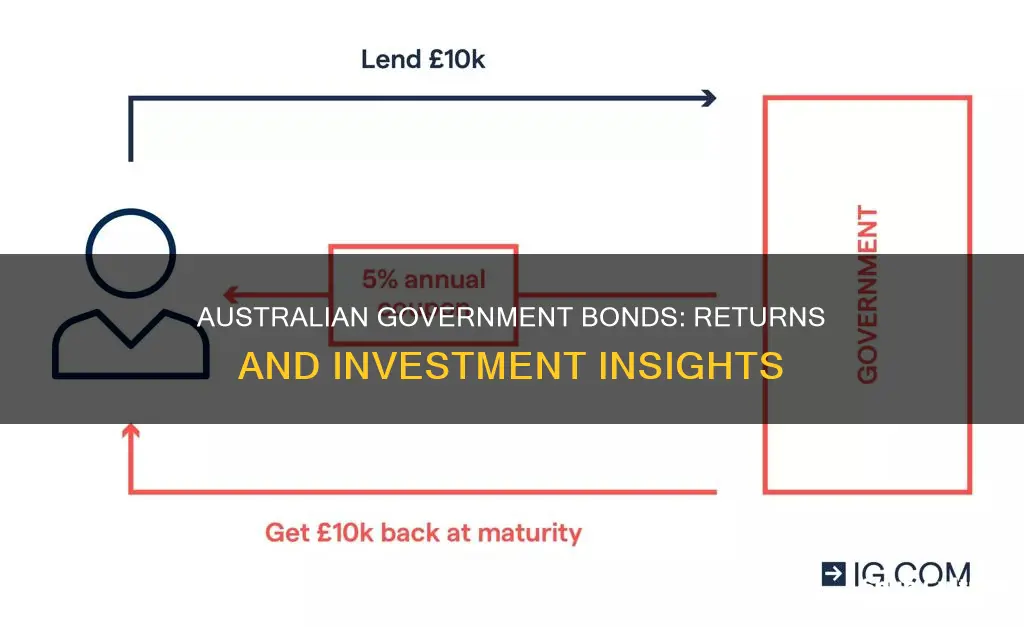

The Coupon Interest Rate on a Treasury Bond is set when the bond is first issued by the Australian Government and remains fixed for the life of the bond. For example, a Treasury Bond with a 5% coupon interest rate will pay investors $5 a year per $100 face value in instalments of $2.50 every six months. These instalments are called Coupon Interest Payments. The Coupon Interest Rate is different from the Yield to Maturity, which is the rate of return on a bond if it is purchased at the current market price and held until the maturity date. The Yield to Maturity will vary over time with changes in the price and remaining term to maturity of the bond.

Coupon Interest Payments for Exchange-Traded Treasury Bonds (eTBs) are paid every six months. If the Coupon Interest Payment date is not a business day, the payment is made on the next business day. The Australian Government's preferred method of payment to investors is by direct credit into an Australian dollar bank account with a financial institution in Australia.

The Coupon Interest Rate is an important factor in determining the overall return on a bond. It represents the regular interest payments made to the investor over the term of the bond. The yield curve, which shows the relationship between interest rates and different maturities of debt, is also an important indicator in financial markets. It helps determine how changes in the policy interest rate and other monetary policy tools will impact a range of interest rates in the economy.

The yield on a bond is the return an investor expects to receive each year over its term to maturity. For the investor, the bond yield represents the overall return, including interest payments and the principal they will receive, relative to the price of the bond. A higher coupon interest rate will result in a higher yield, assuming all other factors remain constant.

It is important to note that the coupon interest rate and yield are not the same as the return on a bond. The return on a bond will depend on various factors, including the price paid for the bond, the coupon interest rate, the yield to maturity, and the remaining term to maturity. Additionally, the credit rating of the issuer and the overall economic conditions can impact the return on a bond.

Controlling Aphid Populations: Australia's Natural Predators

You may want to see also

Explore related products

![]()

How bond prices and yields are related

As of late April 2023, the yield on 10-year Australian government bonds is approximately 3.7%. This indicates the current return or interest rate paid on these securities, offering a benchmark for understanding the relationship between bond prices and yields.

Understanding the inverse relationship between bond prices and yields is essential in the context of Australian government bonds. When the price of a bond goes up, its yield decreases, and vice versa. This relationship stems from the fact that a bond's yield is essentially the return an investor earns over the life of the bond. This yield is calculated by taking the sum of the interest payments and any capital gains or losses over the bond's lifetime and expressing it as a percentage of the bond's price.

When a bond is initially issued, its price is typically set at a face value, often $100 or $1,000. The yield at this point is known as the coupon rate, which is fixed and does not change over the bond's lifetime. However, once the bond is issued and starts trading in the secondary market, its price can fluctuate, which in turn impacts the yield. If the demand for a particular bond increases, its price goes up. Consequently, the yield decreases because the fixed interest payments remain the same, but the percentage return relative to the higher price goes down.

Conversely, if the demand for a bond decreases and its price falls in the secondary market, the yield will increase. This is because an investor can purchase the bond at a lower price while still receiving the same fixed interest payments, resulting in a higher yield relative to the lower price. This relationship between bond prices and yields is crucial for investors when assessing the potential returns and risks associated with investing in bonds. It also highlights the impact of market forces and interest rate expectations on bond prices and yields.

The relationship between bond prices and yields has a significant impact on investment strategies. For example, when interest rates are expected to rise, bond prices often fall to compensate for the higher yields that will be available on newly issued bonds. This can prompt investors to sell their existing bonds, driving down prices further. Conversely, when interest rates are expected to fall, bond prices tend to rise as investors seek to lock in the higher yields available on existing bonds. This dynamic can create opportunities for investors to profit from buying or selling bonds based on their expectations of future interest rate movements.

Understanding how bond prices and yields are related is crucial for investors, particularly in the context of Australian government bonds. This knowledge enables investors to make informed decisions about buying, selling, or holding bonds, taking into account factors such as interest rate expectations, market demand, and the potential impact on their investment portfolios. By considering the inverse relationship between bond prices and yields, investors can effectively navigate the bond market and make strategic choices to meet their financial goals.

Australia's Government: A Guide to its System

You may want to see also

Explore related products

![]()

The cost of borrowing for the Australian government

The Coupon Interest Rate on a Treasury Bond is set when the bond is first issued by the Australian Government and remains fixed for the life of the bond. For example, a Treasury Bond with a 5% Coupon Interest Rate will pay investors $5 a year per $100 face value in instalments of $2.50 every six months. These instalments are called Coupon Interest Payments. The Coupon Interest Rate is usually different from the Yield to Maturity, which is the rate of return on a bond if it is purchased at the current market price and held until the maturity date. The Yield to Maturity will vary over time with changes in the price and remaining term to maturity of the bond.

The yield curve for government bonds is a graph that shows the relationship between interest rates (or yields) and different maturities of debt. It typically plots yields on the y-axis and maturities on the x-axis, ranging from short-term to long-term bonds. Normally, longer-duration interest rates are higher than short-duration rates, so the yield curve usually slopes upward as duration increases. The yield curve can also influence the interest rate on savings products with a fixed term, such as term deposits.

The price of a bond in the market can change after it is issued. If a bond's price increases, it becomes more expensive for a potential new investor to buy, and the bond's yield will then fall because the expected return from purchasing this bond is now lower. Conversely, when interest rates fall, existing bonds become more valuable to investors because they offer higher interest payments compared to new bonds. As a result, the price of existing bonds will increase.

United's Newark-Australia Direct Flight Options Explored

You may want to see also

Explore related products

![]()

Economic confidence and investor sentiment

Government bond yields are critical indicators of economic confidence and investor sentiment. The yield curve for government bonds is an important indicator in financial markets. It helps determine how actual and expected changes in the policy interest rate, along with changes in other monetary policy tools, affect a broad range of interest rates in the economy. A yield curve is a graph that shows the relationship between interest rates (or yields) and different maturities of debt for a specific borrower, often government bonds. It typically plots yields on the y-axis and maturities on the x-axis, ranging from short-term to long-term bonds.

The yield curve for longer-duration bonds usually slopes upward, indicating that interest rates are higher than for shorter-duration bonds. This means that the spread or yield difference between a longer and a shorter bond should be positive. The yield curve influences the interest rates on savings products with fixed terms, such as term deposits, and is important for sectors such as Australian households that borrow using fixed-rate mortgages.

The Coupon Interest Rate on a Treasury Bond is set when the bond is first issued by the Australian Government and remains fixed for the life of the bond. For example, a Treasury Bond with a 5% Coupon Interest Rate will pay investors $5 a year per $100 face value in instalments of $2.50 every six months. These instalments are called Coupon Interest Payments. The Yield to Maturity, or the rate of return on a bond, will vary over time with changes in the price and remaining term to maturity of the bond.

The price of a bond in the market can change after it is issued and traded with other investors. If a bond's price increases, it becomes more expensive for a potential new investor to buy, and the bond's yield will then fall because the expected return from purchasing this bond is now lower. Conversely, when interest rates fall, existing bonds become more valuable to investors because they offer higher interest payments compared to new bonds, so the price of existing bonds will increase.

Unique Australian Delights: What Makes Australia So Special?

You may want to see also

Frequently asked questions

The current return on Australian government bonds depends on the type of bond. The Coupon Interest Rate on a Treasury Bond is set when the bond is first issued and remains fixed for the life of the bond. For example, a Treasury Bond with a 5% Coupon Interest Rate will pay investors $5 a year per $100 face value. The yield on three-year Australian government bonds was 0.25% as of recently. The Australia 10-Year Government Bond currently offers a yield of -.--%.

The Coupon Interest Rate is the interest rate set when the Australian government first issues a Treasury Bond. It remains fixed for the life of the bond.

The Yield to Maturity is the rate of return on a bond if it is purchased at the current market price and held until the maturity date. It is expressed as an annual rate. The calculation assumes that all Coupon Interest Payments are reinvested at the same rate.

The yield curve for government bonds is an important indicator in financial markets. It helps determine how changes in the policy interest rate and other monetary policy tools feed through to a broad range of interest rates in the economy. Normally, longer-duration interest rates are higher than short-duration rates, so the yield curve slopes upward as duration increases.