Australia's official interest rate, also known as the cash rate, is currently held at a target of 4.10% by the country's central bank, the Reserve Bank of Australia (RBA). The RBA Board meets eight times a year to decide whether to alter the cash rate, taking into account various economic factors, including inflation, employment, economic growth, and global financial conditions. The cash rate influences the interest rates charged on loans, savings accounts, and other financial products. While a high cash rate typically leads to high interest rates on loans and favourable rates for savers, a low cash rate results in more affordable loans and lower returns for savers.

| Characteristics | Values |

|---|---|

| Current cash rate in Australia | 4.10% |

| The rate charged on loans between financial institutions | 4.10% |

| The RBA cash rate at the end of 2022 | 3.1% |

| The RBA cash rate at the end of 2021 | 0.1% |

| The RBA cash rate a decade ago (end of 2012) | 2.5% |

| The average policy rate in the Asia-Pacific region at the end of 2022 | 3.7% |

| The all-time high long-term interest rate | 16.50% pa |

| The record low long-term interest rate | 0.80% pa |

| The short-term interest rate in February 2025 | 4.12% pa |

| The Australian Government Bond Yield in February 2025 | 4.42% pa |

Explore related products

What You'll Learn

![]()

Reserve Bank of Australia (RBA)

The Reserve Bank of Australia (RBA) is Australia's central bank. It is responsible for conducting monetary policy, determining payments system policy, maintaining a stable financial system, issuing the nation's banknotes, operating the core of the payments system, and providing banking services to the government.

The RBA meets eight times per year to decide whether to alter the cash rate, which is Australia's official interest rate. This rate is the one charged on loans between financial institutions, such as banks, and it influences other interest rates in the economy, including those on loans and savings accounts. A high RBA cash rate has historically resulted in high-interest rates on home loans, car loans, and personal loans, whereas a low cash rate results in low-interest rates on these products, benefiting borrowers.

When deciding on where to set the cash rate, the RBA aims to keep inflation low and stable, averaging 2-3%. It also considers the level of employment and wants to keep it as high as possible. These outcomes are deemed essential for a prosperous economy.

The RBA Rate Indicator provides market participants and commentators with a market monitor for official cash rate expectations in Australia. It calculates a percentage probability of an RBA interest rate change based on the market-determined prices in the ASX 30-Day Interbank Cash Rate Futures.

Aussie-Style Roast Lamb: Carving and Serving Perfection

You may want to see also

Explore related products

$16.95 $24.95

![]()

RBA's impact on home loans

As of 2025, Australia's current cash rate is 4.10%, as set by the Reserve Bank of Australia (RBA). This cash rate is the official interest rate, which is determined by the RBA in board meetings eight times per year. The RBA's primary goal is to maintain Australia's economic health, and it does so by managing the country's monetary policy, handling gold and foreign exchange services, and issuing currency.

The cash rate set by the RBA has a significant impact on the interest rates of home loans. When the cash rate increases, the interest rates that banks charge customers for home loans also increase. This is because the cash rate determines how much it costs banks to borrow money from other banks, which is then factored into the interest rates charged to customers. Therefore, a high RBA cash rate results in high-interest rates on home loans, and a low cash rate results in low-interest rates, which is beneficial for borrowers.

Banks and lenders generally follow the cash rate movements when setting their loan interest rates. However, non-bank lenders are not always bound by the RBA's decisions, and their rates may be influenced by other factors such as business costs, market competition, and the costs of funding. Additionally, lenders can decide whether to pass on the increase or reduction of the cash rate to their customers.

While the RBA cash rate is a good indicator of home loan rate movements, lenders consider various other factors before changing their interest rates. These factors include the costs of funding, domestic economic conditions, and the Bank Bill Swap Rate (BBSW). It is important to note that even if your lender has the final say on your interest rate, negotiation for a better rate is possible.

The RBA's decisions on the cash rate are based on the country's economic needs. For example, the RBA may cut interest rates to encourage spending and boost economic growth and employment, or it may increase rates to curb high inflation. The RBA also considers key economic factors such as inflation, employment, economic growth, and global financial conditions when making its decisions.

How Much Is 500 Australian Dollars Worth in USD?

You may want to see also

Explore related products

![]()

RBA's impact on savings accounts

The Reserve Bank of Australia (RBA) sets the official cash rate in Australia, which is currently held at a target of 4.10%. The RBA board meets eight times a year to decide whether to alter the cash rate, taking into account key economic factors such as inflation, employment, economic growth, and global financial conditions. The cash rate is the interest rate on overnight loans between banks, and it has a significant impact on the interest rates of financial products available to consumers, including savings accounts.

A high RBA cash rate typically results in high interest rates on savings accounts, while a low cash rate results in low interest rates on these accounts. The RBA may choose to lower interest rates to stimulate spending and investment and boost economic growth and employment. On the other hand, the RBA may decide to increase interest rates to curb high inflation.

Following the RBA's rate cut announcement in February 2025, many banks, including Westpac, Commonwealth Bank, and St. George, were quick to announce rate cuts on variable home loans but were slower to confirm the changes to savings accounts. However, it was expected that most banks would reduce savings interest rates. As of March 6, 2025, fifty-one banks had cut at least one of their savings rates, with most passing on the full 0.25% percentage point cut. This followed a period of savers earning higher interest on their accounts compared to the record lows during the pandemic.

On the other hand, in July 2022, Macquarie Bank delivered rate increases for savers, including its transaction account, savings accounts, and term deposits. Macquarie's savings account rate increased to 1.75% p.a. for balances up to $50,000, effective July 14, 2022. Additionally, ME increased its savings account rate by 50 basis points to 1.60% p.a. during the same period.

Inland Taipan: Australia's Venomous Snake Habitat Explored

You may want to see also

Explore related products

![]()

RBA's impact on term deposits

As of April 2025, the Reserve Bank of Australia (RBA) has set a cash rate target of 4.10%. This is Australia's base interest rate and it influences the interest rates charged by financial institutions on various financial products, including term deposits.

The RBA meets eight times a year to decide on the cash rate, taking into account key economic factors such as inflation, employment, economic growth, and global financial conditions. The RBA aims to maintain an annual inflation rate of 2-3%. When inflation exceeds this range, the RBA may increase the cash rate to curb rising prices. A higher cash rate makes borrowing more expensive, discouraging spending and slowing down the economy. On the other hand, a higher cash rate encourages savings as people can earn more interest on their term deposits and savings accounts.

Conversely, when the economy is sluggish, the RBA may lower the cash rate to stimulate economic growth. Lower interest rates encourage borrowing and spending, which can lead to increased economic activity and job creation. However, low-interest rates may discourage savings as people earn less interest on their term deposits and savings accounts.

The RBA's impact on term deposits is significant. When the RBA raises the cash rate, banks tend to offer higher interest rates on term deposits, making them more attractive to customers. Conversely, when the RBA lowers the cash rate, interest rates on term deposits also tend to decrease. This can result in lower returns for savers, but it may encourage borrowing as loan rates become more favourable.

Overall, the RBA's decisions on the cash rate have a direct impact on the interest rates offered on term deposits in Australia. The RBA uses these interest rate adjustments to influence economic activity and maintain price stability in the country.

Crows in Australia: Their Habitat and Range

You may want to see also

Explore related products

![]()

RBA's policy rate in 2022

The Reserve Bank of Australia (RBA) is responsible for setting the country's monetary policy, which includes determining the official interest rate, also known as the cash rate. The RBA's monetary policy decisions are aimed at maintaining price stability, fostering full employment, and contributing to the stability and efficiency of the financial system.

The RBA Board meets eight times a year to decide whether to adjust or maintain the cash rate, taking into account key economic indicators such as inflation, employment, economic growth, and global financial conditions. The cash rate is the rate at which banks borrow money from each other overnight, and it influences other interest rates in the economy, including those on loans and savings accounts.

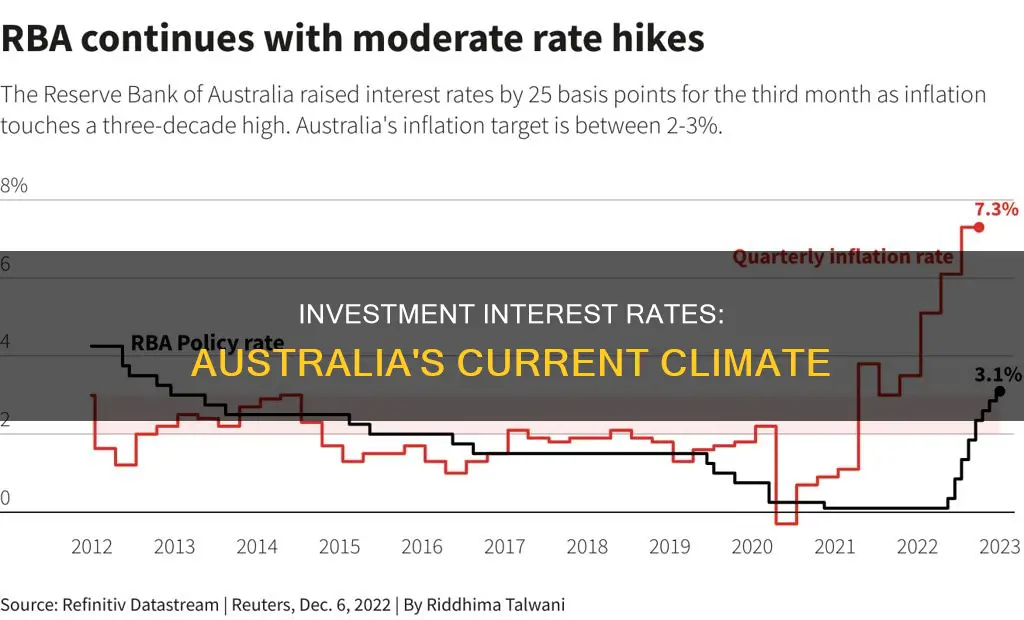

In 2022, the RBA's policy rate decisions were largely influenced by the high inflationary environment in Australia. In December 2022, the RBA Board decided to increase the cash rate target by 25 basis points to 3.10%, with the goal of curbing inflation, which had reached 6.9% over the year to October. This decision built on previous rate increases throughout the year, as the RBA aimed to bring inflation back within its target range of 2-3%.

The RBA's actions in 2022 reflected its mandate to maintain price stability and support economic growth. By adjusting the policy rate, the RBA sought to balance the need to tame inflation while ensuring that the economy grew at a sustainable pace. These rate decisions had a direct impact on the cost of borrowing for individuals and businesses, influencing their spending and investment decisions.

Looking ahead, the RBA expects economic growth to moderate in the coming years, with a central forecast of around 1.5% growth in 2023 and 2024. The labour market remains tight, with a low unemployment rate of 3.4% recorded in October 2022. The RBA will continue to monitor these economic indicators and adjust its policy rate accordingly to achieve its monetary policy objectives.

America's Influence on Australia's Government

You may want to see also

Frequently asked questions

The Reserve Bank of Australia (RBA) has set the official interest rate, also known as the cash rate, at 4.10%. This is the rate at which banks borrow from each other overnight.

The RBA board meets eight times per year to decide whether to alter the cash rate. They consider economic factors such as inflation, employment, economic growth, and global financial conditions.

A high cash rate typically leads to high interest rates on loans and savings accounts, while a low cash rate results in lower interest rates.