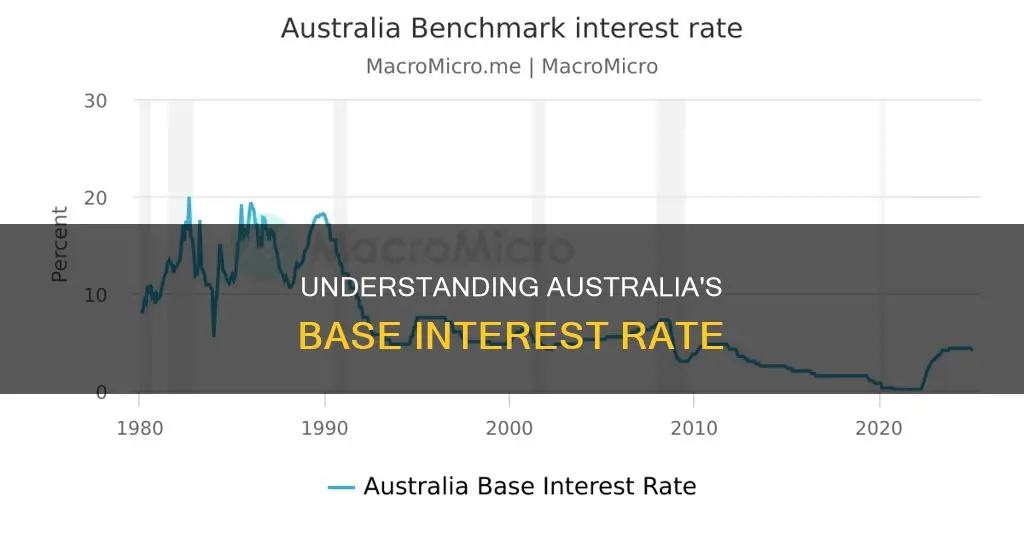

The Reserve Bank of Australia (RBA) sets a cash rate that influences the interest rates set by lenders and banks. The RBA Board meets eight times a year to decide whether to alter the cash rate, taking into account economic factors such as inflation, employment, economic growth, and global financial conditions. The RBA aims to keep inflation between 2% and 3% and achieve sustained full employment to maximize the economic welfare of Australians. The cash rate set by the RBA is the interest rate paid on overnight loans between banks, which then impacts the rates offered to customers.

| Characteristics | Values |

|---|---|

| Official Name | Official Cash Rate (OCR) |

| Setting Authority | Reserve Bank of Australia (RBA) |

| Frequency of Setting | 8 times per year |

| Considerations | Inflation, employment, economic growth rate, global financial conditions |

| Inflation Goal | 2-3% |

| Unemployment Impact | Lower interest rates to stimulate spending and investment |

| Basis for Default Interest Calculation | Reserve Bank Cash Rate + 6% |

| Home Loan Base Criteria | $500,000 loan amount over 30 years |

| Car Loan Base Criteria | $30,000 loan over 5 years |

| Personal Loan Base Criteria | $20,000 loan over 5 years |

Explore related products

What You'll Learn

![]()

Official Cash Rate (OCR)

The official cash rate (OCR) is the term used in Australia and New Zealand for the bank rate. It is the interest rate that the central bank, the Reserve Bank of Australia, charges on overnight loans between commercial banks. The OCR is set by the Reserve Bank of Australia to influence the Interbank Overnight Cash Rate (also known as the Cash Rate) on unsecured loans between banks.

The OCR is a tool used by the Reserve Bank to influence inflation. It does this by adjusting the interest rates that apply in the economy. The OCR is reviewed regularly, usually once a month in Australia. The Reserve Bank issues its dealing intentions at the start of each day, and banks and other financial institutions will act prior to the actual rate being achieved.

The OCR influences the price of borrowing money in Australia. A decreased OCR could mean lower home loan rates for borrowers, but it can also mean lower savings and term deposit rates for savers. The OCR also affects the rates on housing and other loans within a matter of days or weeks.

The OCR cannot be changed by transactions between financial institutions as this does not change the supply of money, only its location. Only transfers between the central bank and an institution can affect the OCR. The central bank can regulate the rate paid for cash by the sale or buyback of bonds and other government-issued securities, known as domestic market operations. As the sale or purchase of bonds affects the supply of money, the interest rate will change to reflect its availability.

Birds' Appetite for Olives in Australia: What's the Verdict?

You may want to see also

Explore related products

![]()

Reserve Bank of Australia's (RBA) influence

The Reserve Bank of Australia (RBA) has a significant influence on the country's base interest rate, also known as the cash rate target. The RBA's primary role is to promote the economic prosperity and welfare of Australians by ensuring price stability, full employment, and the stability of the financial system.

One of the RBA's key responsibilities is setting monetary policy, which includes determining the cash rate or the base interest rate. The RBA's decisions on the cash rate target influence other interest rates in the economy, including those on loans, savings accounts, and term deposits. A higher cash rate set by the RBA generally benefits savers but can be disadvantageous to borrowers. The RBA's monetary policy aims to smooth out fluctuations in the economy by adjusting interest rates, keeping inflation stable, and maintaining high employment levels.

The RBA's influence on the base interest rate is driven by its mandate to promote economic stability and growth. By adjusting the cash rate, the RBA can influence people's spending and investment decisions, affecting economic activity. Additionally, the RBA's actions can impact the exchange rate and the value of assets, such as homes or shares.

The RBA's quantitative easing program, initiated in March 2020, is another example of its influence on the overnight rate. Through this program, the RBA purchased a significant amount of government bonds, injecting money into the market and driving the overnight rate close to 0%. This action had consequences for the Australian government's debt and the tax bills of full-time workers.

Furthermore, the RBA's role in the payment system and its position as the banker for the Australian Government gives it additional influence. The RBA facilitates transactions between different banks and has developed innovative payment systems, such as the New Payments Platform, enabling real-time payments. The RBA's operations contribute to the efficiency and stability of the payment system, supporting its overall influence on the financial landscape and interest rates in Australia.

Chickens Eating Ticks: An Australian Solution?

You may want to see also

Explore related products

$125.98 $159.99

![]()

Factors affecting interest rates

Interest rates in Australia are influenced by a multitude of factors, which can be grouped into two broad categories: economic factors and financial factors.

Economic factors include the health of the Australian economy, as well as international economic conditions. The Reserve Bank of Australia (RBA) monitors these conditions to guide its monetary policy decisions. The RBA aims to keep consumer price inflation between 2% and 3% and to achieve sustained full employment. When the economy is strong and inflation is under control, interest rates tend to be lower. Conversely, when the economy is weak or inflation is high, the RBA may raise interest rates to encourage saving and reduce spending.

Financial factors include the cash rate, which is the interest rate charged by the RBA to financial institutions. The cash rate influences lending and deposit rates, which in turn affect the cost of borrowing for businesses and consumers. The RBA can adjust the cash rate to manage the growth of the economy and control inflation. When the cash rate is low, it encourages borrowing and spending, which can stimulate economic growth. However, when the cash rate is high, it discourages borrowing and can lead to reduced spending and slower economic growth.

Another financial factor is the exchange rate. When interest rates are low, it encourages capital outflow, as investors sell Australian dollars to buy foreign assets. This can lead to a depreciation of the Australian dollar, making imports more expensive and exports more competitive. The exchange rate also affects the current account deficit, with higher net exports leading to a decrease in the deficit.

Budget surpluses are also a consideration. Surpluses can lead to lower interest rates, which in turn can stimulate higher output and greater capacity to retire debt or purchase assets. However, this dynamic assumes that fiscal policy remains stable and surpluses continue to increase, which may not always be the case in practice.

Additionally, the interest rates offered to businesses can affect their financial decisions. Higher interest rates provide an incentive for businesses to borrow funds and may encourage them to lend money for longer periods. This can impact their cash flow and influence their investment decisions.

Applying for CPA in Australia: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Home loan base criteria

Age is a significant factor in determining home loan eligibility. Lenders consider the applicant's age to assess their repayment capacity and determine the loan tenure. Younger borrowers generally qualify for longer-term loans, resulting in lower monthly payments but a higher overall interest rate. Conversely, older borrowers may opt for shorter tenures to repay the loan earlier.

The applicant's financial position and income are also crucial factors. Lenders evaluate the individual's net monthly income to gauge their repayment capacity and determine the loan amount they qualify for. It is important to note that a higher salary does not always guarantee better chances of loan approval. Other financial obligations, such as existing loans or EMIs, can negatively impact an individual's credibility for a home loan.

Credit history and credit score play a vital role in assessing an individual's creditworthiness. Lenders may use tools like the CIBIL score (Credit Information Bureau (India) Limited) to determine an applicant's credit history. This 3-digit score ranges from 300 to 900, with higher scores indicating better creditworthiness. It takes time and consistent financial responsibility to obtain a satisfactory credit score.

Other factors that may influence home loan eligibility include employment status, property value, and debt-to-income ratio. By using home loan eligibility calculators provided by lenders, individuals can assess their qualification for a loan and make informed decisions about their home purchase journey.

Exploring Italy: The Long-Haul Flight Challenge

You may want to see also

Explore related products

![]()

Interest rates and inflation

The Reserve Bank of Australia (RBA) is Australia's central bank and is responsible for setting monetary policy to maintain price stability and full employment, contributing to the efficiency and stability of the payments system, and the stability of the financial system. One of the RBA's primary tools for achieving these objectives is setting the cash rate, also known as the interest rate. The cash rate is the rate that banks charge each other to borrow money overnight, and it influences other interest rates in the economy, such as loan rates and savings rates.

The RBA adjusts the cash rate to smooth out fluctuations in the economy. For example, in a growing economy with rising inflation, the RBA may increase the cash rate to curb spending and borrowing, helping to stabilise prices. On the other hand, in a slowing economy with falling inflation, the RBA may decrease the cash rate to encourage spending and investment, stimulating economic growth.

Inflation is a key factor considered by the RBA when making interest rate decisions. Inflation refers to the general increase in the price of goods and services over time and is measured by the Consumer Price Index (CPI). A moderate level of inflation is generally considered healthy for an economy as it indicates economic growth. However, when inflation rises too high, it can erode purchasing power and destabilise the economy.

In recent years, Australia has experienced relatively low inflation, with the annual inflation rate falling to 2.8% in September 2025, according to the Australian Bureau of Statistics. This was slightly lower than economist predictions of 2.9%. The underlying inflation rate, which excludes volatile items and is known as the trimmed mean, was higher at 3.5% but still lower than the previous quarter. The RBA focuses on this underlying inflation measure when deciding whether to adjust interest rates.

The impact of inflation on interest rates is complex. Typically, in a high-inflation environment, central banks like the RBA will increase interest rates to curb inflation and stabilise prices. Higher interest rates make borrowing more expensive, discouraging spending and investment, which can help slow down economic activity and ease inflationary pressures. However, in some cases, the RBA may choose to keep interest rates low, even in a high-inflation environment, to stimulate economic growth and maintain full employment. This delicate balance between inflation and interest rates is a critical aspect of monetary policy and requires careful consideration of various economic indicators and factors.

Rats in Australia: An Invasive Species

You may want to see also

Frequently asked questions

The base interest rate in Australia, also known as the cash rate, is determined by the Reserve Bank of Australia (RBA). The RBA sets this rate based on whether the economy needs stimulating or slowing down.

The RBA Board meets eight times per year to decide whether to alter the cash rate or keep it steady.

The RBA considers various key economic factors, including inflation, employment levels, the economic growth rate of the Australian economy, and global financial conditions.

The RBA has a flexible annual inflation goal of keeping inflation between 2% and 3%.

The cash rate set by the RBA influences the interest rates on loans and deposits in the economy. Lenders source funds from various markets, and the cost of these funds is influenced by the cash rate. When the cost of sourcing funds increases, lenders often pass these costs on to customers by raising interest rates on loans.