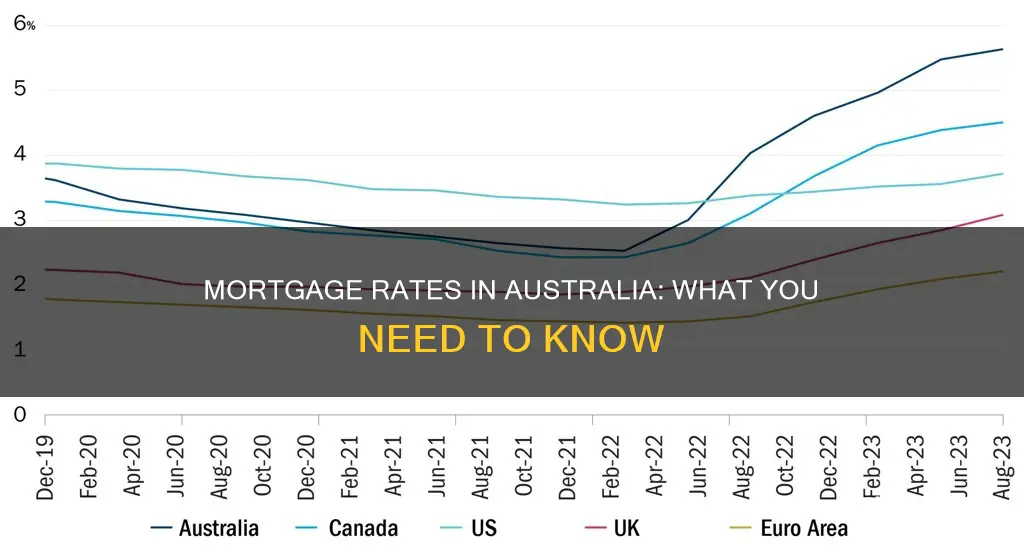

Australia's mortgage rates are influenced by various factors, including loan type, lender, and market conditions. The two primary types of home loans in Australia are owner-occupied and investment loans, with rates varying based on the loan-to-value ratio and the borrower's credit rating. While the Big Four banks are the largest mortgage lenders, they may not always offer the best rates, and borrowers can choose between fixed and variable interest rates. With the official cash rate unchanged, lenders are starting to lower their rates, and borrowers are actively seeking out the lowest rates.

| Characteristics | Values |

|---|---|

| Home loan interest rates | From 4.94% |

| Home loan comparison rates | From 5.14% p.a. |

| Interest rates | Fixed or variable |

| Lender's mortgage insurance | Charged on some home loans with less than a 20% deposit |

| Home loan types | Owner-occupied, investment, fixed-rate, variable-rate, and split |

| Best lenders | Not a single best lender for everyone, but there is a best home loan for each individual |

Explore related products

What You'll Learn

![]()

Fixed vs variable interest rates

When taking out a home loan in Australia, you can choose between a fixed-rate loan and a variable-rate loan. Fixed-rate home loans lock in a set interest rate for a specified amount of time, usually for the first one to five years of your mortgage, after which it reverts to a standard variable interest rate. In rare cases, banks may allow a fixed rate for the first ten years. Variable-rate home loans have a rate that moves in line with the standard variable interest rate.

Fixed-rate loans can be beneficial if you expect interest rates to rise in the future, as they offer certainty and predictable repayments. However, if interest rates fall, you will not benefit from any reductions, and you may have to pay break or exit fees if you decide to end the fixed period of your loan early. Additionally, fixed-rate loans often have fewer features, such as limited access to redraw and offset account options, and you may not be able to make extra repayments.

On the other hand, variable-rate loans offer more flexibility, as you can take advantage of falling interest rates, which will reduce your repayments. Variable rates can also be lower than fixed rates at the time of settlement. However, if interest rates rise, your repayments will also increase. Variable-rate loans require more flexibility from the borrower due to the unpredictability of cash flow over the long term.

It is worth noting that the majority of Australians opt for variable-rate mortgages, as variable rates often have lower interest rates than fixed rates, and there is a lack of demand for long-term fixed rates. Additionally, Australia's debt market is not developed enough to easily allow lenders to sell bundles of long-term fixed-rate mortgages to investors.

Ultimately, when deciding between a fixed or variable interest rate, it is essential to consider your financial situation, needs, and expectations of interest rate movements. You may also choose to split your home loan into multiple accounts, taking advantage of both fixed and variable rates to balance predictability and flexibility.

Converting Euros to Australian Dollars: How Much Is It?

You may want to see also

Explore related products

![]()

Owner-occupied vs investment loans

Owner-occupied and investment loans are two different types of home loans available in Australia. The type of loan one takes depends on what they intend to do with the property. If the buyer intends to live in the property, they will need an owner-occupied home loan. If they plan to rent it out to tenants, they will need an investment loan.

Owner-occupied home loans are considered a "safer" option by lenders than investment loans. This is because owner-occupied properties are used as the owner's main residence, and the loan is repaid with the owner's regular income, which is usually more stable. Hence, owner-occupied loans have lower interest rates than investment loans. In Australia, owner-occupied loans usually require a 20% cash deposit for the borrower to avoid paying lenders' mortgage insurance (LMI). For example, a $500,000 property would require a $100,000 deposit.

On the other hand, investment loans are mortgages designed for buyers obtaining a property as an asset for the purpose of generating rental income. These loans are usually issued to people who are already homeowners. Investment loans are used as a way to build wealth through real estate. They usually have higher interest rates and fees than owner-occupied loans because lenders consider them riskier. Investors use the money they make from renting out properties to pay back these loans, but this income can be unpredictable. Hence, a larger down payment may be required for an investment loan, resulting in a higher loan-to-value ratio (LVR).

It is important to note that the original purpose of the loan is less important than how the borrowed funds are used. If the loan is used to purchase a property that generates rental income, the interest paid on the loan is deductible as an expense. Additionally, investment properties come with important tax implications. Any income earned from the investment property must be recorded and declared with the Australian Taxation Office. Investment properties also come with tax deductions such as advertising, management fees, council rates, and interest.

Airlines Departing from Perth, Australia: A Comprehensive Guide

You may want to see also

Explore related products

![]()

How to compare home loans

When comparing home loans, it is important to consider a range of factors, including interest rates, fees, and charges. Here are some key things to keep in mind when comparing home loans in Australia:

Types of Home Loans

There are two main types of home loans in Australia: owner-occupied and investment home loans. Owner-occupied home loans are for those who intend to live in the property they are buying, while investment home loans are for those who plan to rent out the property to tenants.

Interest Rates

Interest rates play a significant role in the overall cost of your home loan. You can choose between a variable rate, which may change over time, or a fixed rate, which remains the same for a specified period. It is worth noting that the lowest available interest rate may not always be the best option, as loans with slightly higher interest rates may offer more flexibility or additional features that could save you money in the long run.

Comparison Rates

Comparison rates are designed to help you understand the 'true' cost of a loan by incorporating the interest rate, fees, and charges into a single percentage figure. While this can be useful for comparing loans, it is important to remember that it is a hypothetical calculation and may not reflect your unique financial situation.

Mortgage Brokers

Mortgage brokers can provide valuable advice and recommendations tailored to your financial objectives and needs. They can help you navigate the wide range of home loan options and find the most suitable loan for your circumstances. However, it is important to be aware that mortgage brokers may have limited access to loan products and may receive commissions from lending institutions, so their advice may not always be completely unbiased.

Lender's Criteria

When deciding whether to approve your loan application, lenders will consider your credit rating and loan-to-value ratio (LVR). Your credit score indicates your level of financial responsibility, with a higher score improving your chances of approval and giving you access to a wider range of lenders. The LVR is the amount you are borrowing as a percentage of the property's value, and it impacts the interest rate offered by the lender.

Government Schemes

The Australian government offers schemes such as the First Home Guarantee to assist first-time homebuyers in obtaining a loan with a lower deposit requirement. These schemes can help you secure a home loan with a deposit as low as 5%, so it is worth exploring your eligibility for such programs.

By considering these factors and utilising tools such as mortgage calculators and comparison websites, you can make an informed decision when comparing home loans in Australia.

Trademark Application in Australia: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Mortgage brokers

Before seeking a mortgage broker, it is recommended that buyers prepare a wishlist of the features they want in their mortgage, how much they want to borrow, the type of property they want, and where they want to live. Buyers should also ask for a written quote from the broker outlining all the important aspects of the loan, such as the term of the loan, the interest rate, and the cost of mortgage insurance. It is also important to choose a broker who has worked with clients in your state, as different grants and schemes are available in different areas.

In Australia, mortgage brokers must operate under an Australian Credit Licence (ACL) and hold a recognised qualification in finance. They must also be registered with the Australian Securities and Investments Commission (ASIC) and have a membership with the Australian Financial Complaints Authority (AFCA).

Australia's Natural Landscape: A Biome Overview

You may want to see also

Explore related products

![]()

Lender's mortgage insurance

Lenders' Mortgage Insurance (LMI) is a type of insurance that lenders purchase to protect themselves in case a borrower defaults on their home loan and the sale of the property doesn't cover the outstanding loan balance. While LMI primarily insures the lender, it also offers significant benefits to borrowers. It allows them to secure home loans sooner, even without the typical 20% deposit, helping them break the rental cycle. Additionally, LMI can assist borrowers looking to upsize or refinance their home loan, provided they meet the lender's requirements.

LMI is required by lenders when borrowers have a lower deposit, usually less than 20% of the property's value. These high loan-to-value ratio (LVR) loans are riskier for lenders. LMI allows lenders to transfer this risk to a specialised mortgage insurer, enabling more lenders to offer high LVR loans. The cost of LMI is typically passed on by the lender to the borrower as a fee, which can be paid upfront or added to the loan repayments. The cost of LMI depends on the loan size and LVR rather than borrower characteristics such as employment type, location, or credit score.

It's important to note that LMI should not be confused with mortgage protection insurance (MPI), which is an insurance option for borrowers. MPI protects the borrower by making certain mortgage repayments on their behalf or paying off a lump sum of the mortgage in specific circumstances, such as involuntary unemployment, sickness, accident, or death. In the case of LMI, if a borrower can't repay their home loan and the property is sold, the lender can claim the shortfall from the mortgage insurer, who will then pay the lender according to the LMI agreement. The borrower is still liable to pay the shortfall, for example, to the mortgage insurer if the lender claims on LMI.

Borrowers can find out more about LMI and their options by speaking to their lender or financial institution. LMI can help borrowers get into the housing market sooner, but it's important to understand the costs and liabilities involved.

Free Australian Dating Sites: Find Love Without Cost

You may want to see also

Frequently asked questions

As of March 2025, mortgage rates in Australia start from 4.94% to 5.23% p.a. However, these rates are subject to change and vary across lenders.

There are two main types of mortgage rates in Australia: fixed and variable. Fixed rates remain unchanged for a set period, typically 1 to 5 years, offering stability and predictability. Variable rates, on the other hand, fluctuate over time based on the Reserve Bank of Australia's cash rate and economic factors, providing flexibility but with the risk of rate increases.

To get the best mortgage rate, consider factors such as your loan-to-value ratio (LVR) and credit rating. A higher deposit or equity in your home can lead to lower rates, as they are less risky for lenders. Comparison tools and calculators can assist in finding the most suitable rate for your circumstances.

A comparison rate represents the 'true' cost of a mortgage by combining the interest rate with fees and charges, expressed as a single percentage. This simplifies the comparison process and helps borrowers understand the overall cost beyond the advertised interest rate.

Several websites offer comparison tools and calculators to help Australians find the best mortgage rates. These include Money.com.au, Canstar, Mozo, and HSBC. These platforms provide insights into different home loan products, rates, and features, allowing borrowers to make informed decisions based on their specific needs.