Brazil's economy, the largest in Latin America and the ninth-largest globally, has shown resilience despite facing significant challenges in recent years. Following a deep recession in 2015-2016 and the economic fallout from the COVID-19 pandemic, the country has experienced a gradual recovery, driven by rising commodity prices, increased agricultural exports, and cautious fiscal reforms. However, persistent issues such as high inflation, unemployment, and public debt continue to weigh on growth. Structural challenges, including a complex tax system, bureaucratic inefficiencies, and infrastructure gaps, also hinder long-term competitiveness. While Brazil remains a key player in global markets, particularly in agriculture and natural resources, its economic trajectory will depend on sustained policy reforms, political stability, and the ability to address inequality and diversify its industrial base.

Explore related products

$13.55 $44.99

What You'll Learn

![]()

GDP growth trends and recent performance

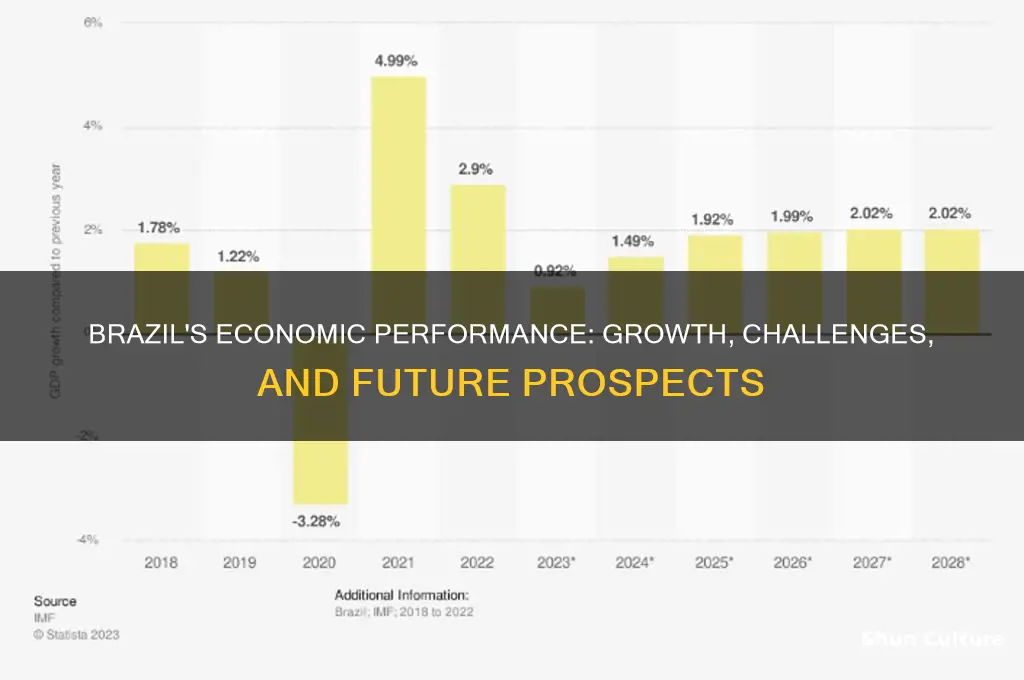

Brazil's GDP growth has been a rollercoaster in recent years, reflecting the country's struggle to regain economic momentum after a severe recession in 2015-2016. The economy contracted by 3.5% in 2015 and 3.3% in 2016, marking one of the deepest downturns in its history. Since then, recovery has been sluggish, with annual growth rates hovering around 1% to 2% until the COVID-19 pandemic struck in 2020, causing another sharp contraction of 3.3%. Despite a rebound of 4.6% in 2021, driven by commodity exports and fiscal stimulus, growth slowed to 2.9% in 2022 as global headwinds and domestic challenges took their toll. This uneven trajectory highlights Brazil’s vulnerability to external shocks and its struggle to achieve sustained, robust growth.

Analyzing the drivers of Brazil’s GDP performance reveals a heavy reliance on commodity exports, particularly agricultural products and minerals, which account for a significant portion of its GDP and trade surplus. For instance, in 2022, soybean and iron ore exports were key contributors to economic growth, benefiting from high global prices. However, this dependence on commodities makes the economy susceptible to price volatility and global demand fluctuations. On the domestic front, high inflation, which peaked at 10.1% in 2022, has eroded purchasing power and dampened consumer spending. The Central Bank’s aggressive monetary tightening, with the benchmark interest rate reaching 13.75% in 2022, has helped curb inflation but at the cost of slowing investment and credit growth.

A comparative perspective underscores Brazil’s underperformance relative to its emerging market peers. While countries like India and Indonesia have consistently achieved growth rates above 5%, Brazil has lagged, partly due to structural issues such as low productivity, cumbersome bureaucracy, and inadequate infrastructure. For example, Brazil ranks 124th out of 190 countries in the World Bank’s Doing Business report, reflecting the challenges businesses face in operating efficiently. Additionally, public debt, which surpassed 80% of GDP in 2022, limits the government’s ability to invest in critical areas like education, healthcare, and infrastructure, further constraining long-term growth potential.

To improve GDP growth trends, Brazil must address these structural bottlenecks. One practical step is to advance pension and tax reforms to enhance fiscal sustainability and free up resources for public investment. For instance, the 2019 pension reform is expected to save the government over $200 billion in a decade, but further measures are needed to streamline the tax system and reduce compliance costs for businesses. Another critical area is infrastructure, where public-private partnerships can play a key role in modernizing transportation, energy, and digital networks. For businesses, investing in technology and innovation can boost productivity, while policymakers should focus on improving the ease of doing business to attract foreign investment.

In conclusion, Brazil’s GDP growth trends reflect a mix of resilience and fragility. While the economy has shown the ability to recover from shocks, structural weaknesses continue to hinder its potential. By addressing fiscal imbalances, improving the business environment, and investing in productivity-enhancing measures, Brazil can lay the foundation for more sustained and inclusive growth. The challenge lies in implementing these reforms amidst political and economic constraints, but the payoff—a more dynamic and competitive economy—is well worth the effort.

Exploring Bachata's Presence in Brazil: Do They Dance It?

You may want to see also

Explore related products

![]()

Unemployment rates and labor market conditions

Brazil's unemployment rate has been a rollercoaster over the past decade, reflecting broader economic volatility. After peaking at 14.7% in early 2017, it dropped to 11.2% by late 2019, only to spike again during the pandemic, reaching 14.9% in mid-2020. As of 2023, the rate hovers around 8.5%, a significant improvement but still above pre-pandemic levels. This fluctuation underscores the labor market’s sensitivity to economic shocks and policy shifts, making it a critical indicator of Brazil’s economic health.

Digging deeper, the labor market’s recovery isn’t uniform across sectors or demographics. Informal employment, which accounts for over 40% of the workforce, has been a safety net during downturns but offers little job security or benefits. Youth unemployment remains disproportionately high, with rates exceeding 25% in some regions, stifling long-term productivity. Conversely, sectors like agriculture and technology have shown resilience, driven by global demand for commodities and digital transformation. Policymakers must address these disparities to ensure sustainable growth.

To tackle unemployment effectively, Brazil needs a multi-pronged strategy. First, invest in reskilling programs tailored to high-demand sectors like renewable energy and IT. Second, incentivize formal employment through tax breaks for small businesses, which employ the majority of workers. Third, strengthen social safety nets to support vulnerable groups during transitions. For individuals, staying adaptable is key—acquiring digital skills or certifications can enhance employability in a rapidly evolving job market.

Comparatively, Brazil’s labor market challenges mirror those of other emerging economies but with unique complexities. Unlike India, where a young population drives demand, Brazil faces an aging workforce, increasing pressure on pensions and healthcare. Unlike Mexico, its economy is less integrated with global supply chains, limiting job creation in manufacturing. Learning from peers, Brazil could prioritize export-oriented industries and labor reforms to boost competitiveness.

In conclusion, while Brazil’s unemployment rate is declining, structural issues persist. Addressing informality, demographic imbalances, and sectoral gaps requires targeted policies and individual initiative. By fostering a more inclusive and dynamic labor market, Brazil can turn its economic recovery into lasting prosperity.

Experiencing Brazil: Culture, Vibes, and Daily Life in a Vibrant Nation

You may want to see also

Explore related products

![]()

Inflation levels and monetary policy impact

Brazil's inflation rate has been a rollercoaster in recent years, with the Central Bank of Brazil (BCB) walking a tightrope to balance economic growth and price stability. In 2021, inflation surged to 10.06%, exceeding the upper limit of the BCB's target range, primarily driven by supply chain disruptions, rising commodity prices, and a weak exchange rate. To combat this, the BCB adopted an aggressive monetary policy stance, raising the benchmark Selic rate from 2% in March 2021 to 13.75% in August 2022. This swift action demonstrates the BCB's commitment to anchoring inflation expectations and restoring price stability.

Consider the following scenario: a Brazilian family earning the monthly minimum wage of R$1,212 (approximately $230) in 2021 would have experienced a significant erosion in their purchasing power due to the high inflation rate. For instance, the cost of a basic food basket in São Paulo increased by 18.3% in 2021, according to the Dieese research institute. This example highlights the tangible impact of inflation on households and the urgency for effective monetary policy interventions.

The BCB's monetary policy decisions have had a ripple effect throughout the economy. As interest rates rose, credit became more expensive, leading to a slowdown in consumption and investment. This, in turn, helped ease inflationary pressures, with the rate dropping to 5.35% in March 2023, within the target range of 3.25% (with a tolerance interval of 1.5 percentage points on either side). However, the tight monetary policy also contributed to a decline in GDP growth, which slowed to 0.9% in 2022 from 4.7% in 2021. This trade-off between inflation control and economic growth is a delicate balance that central banks worldwide grapple with.

To navigate this complex landscape, the BCB employs a data-driven approach, closely monitoring key economic indicators such as inflation expectations, unemployment rates, and exchange rate movements. For example, the BCB's Focus survey, which gathers forecasts from market analysts, is a crucial tool for assessing inflation expectations. As of May 2023, the survey projected an inflation rate of 4.16% for 2023, indicating that market participants expect the BCB to successfully steer inflation towards the target range.

A comparative analysis of Brazil's monetary policy with other emerging markets reveals both similarities and differences. Like Brazil, countries such as Mexico and Chile have also raised interest rates to combat inflation. However, Brazil's monetary policy has been more aggressive, reflecting the severity of its inflation problem. This comparison underscores the importance of tailoring monetary policy to the specific circumstances of each economy. As Brazil continues to navigate its economic challenges, a nuanced understanding of inflation dynamics and the impact of monetary policy will be crucial for informing future decisions and promoting long-term economic stability.

Brazil Nuts: Unlocking Their Essential Nutrients and Health Benefits

You may want to see also

Explore related products

![Brazil (The Criterion Collection) [4K UHD]](https://m.media-amazon.com/images/I/81L2MkCaFQL._AC_UY218_.jpg)

![]()

Trade balance and export-import dynamics

Brazil's trade balance has been a cornerstone of its economic resilience, with a consistent surplus since 2015. In 2022, the country recorded a trade surplus of $61.4 billion, driven primarily by exports of agricultural products, minerals, and oil. Soybeans, iron ore, and crude petroleum dominate the export basket, accounting for over 30% of total exports. This surplus has been instrumental in stabilizing the Brazilian Real and bolstering foreign exchange reserves, which stood at $350 billion as of late 2023. However, this reliance on commodities exposes Brazil to global price volatility, as seen in 2020 when a drop in oil prices significantly reduced export revenues.

To mitigate risks and diversify its export base, Brazil has been actively pursuing trade agreements and fostering industrial sectors. The Mercosur-EU trade deal, though still pending ratification, promises to open new markets for Brazilian manufactured goods and services. Additionally, the government has launched initiatives like the *Novo Mercado de Gás* to modernize the natural gas sector, aiming to increase exports and reduce domestic costs. Despite these efforts, manufactured goods still represent only 35% of total exports, compared to 50% in Mexico, highlighting the need for further industrialization.

Imports, on the other hand, have been steadily rising, driven by demand for machinery, chemicals, and electronics, which are critical for Brazil’s industrial and agricultural sectors. In 2022, imports reached $215 billion, up 25% from 2020. This increase reflects both economic recovery and the need for intermediate goods to sustain production. However, the surge in imports has narrowed the trade surplus, raising concerns about long-term sustainability. Policymakers must balance import growth with export diversification to maintain a healthy trade balance.

A comparative analysis reveals Brazil’s trade dynamics differ significantly from peers like China and India. While China’s trade surplus is driven by high-tech manufacturing, Brazil remains heavily dependent on raw materials. India, meanwhile, has made strides in services exports, an area where Brazil lags. To emulate these successes, Brazil could invest in technology and innovation, particularly in sectors like aerospace and pharmaceuticals, which offer high export potential. For instance, Embraer, Brazil’s aircraft manufacturer, already contributes significantly to exports but could expand further with targeted government support.

In conclusion, Brazil’s trade balance is a strength but also a vulnerability. While the surplus provides stability, over-reliance on commodities and insufficient diversification pose risks. Practical steps include accelerating industrial modernization, leveraging trade agreements, and investing in high-value sectors. By doing so, Brazil can transform its trade dynamics, ensuring sustained economic growth and resilience in an increasingly competitive global market.

Brazil vs. France: Analyzing Performance, Tactics, and Key Moments in the Match

You may want to see also

Explore related products

![Brazil [Blu-ray]](https://m.media-amazon.com/images/I/71shoUBJ1iL._AC_UY218_.jpg)

![]()

Public debt and fiscal health overview

Brazil's public debt has been a central concern in its economic narrative, with gross debt hovering around 80% of GDP in recent years. This figure, while high, reflects a stabilization after a sharp rise during the 2020 pandemic. The government’s reliance on domestic financing has insulated it somewhat from external shocks, but it also ties up local capital that could otherwise fuel private investment. The debt-to-GDP ratio remains a critical metric for investors and policymakers alike, as it signals the government’s ability to manage fiscal obligations without crowding out economic growth.

To understand Brazil’s fiscal health, consider the primary deficit—the gap between government revenue and expenditure excluding interest payments. In 2023, efforts to reduce this deficit focused on spending caps and tax reforms, yet challenges persist due to rigid constitutional spending requirements. For instance, nearly 90% of federal expenditures are mandated for areas like social security and public sector salaries, leaving little room for discretionary spending. This structural rigidity complicates deficit reduction, even as the government aims to meet its fiscal targets.

A comparative lens reveals Brazil’s position relative to peers. Unlike countries with similar debt levels, Brazil’s debt is predominantly denominated in local currency, reducing exchange rate risk. However, its interest payments consume a larger share of revenue compared to regional counterparts like Chile or Mexico. This inefficiency underscores the urgency of fiscal reforms to lower borrowing costs and redirect resources toward productive investments in infrastructure and education.

Practical steps to improve fiscal health include accelerating pension reforms, as Brazil’s aging population threatens to balloon social security costs. The 2019 pension overhaul was a start, but further adjustments are needed to ensure long-term sustainability. Additionally, enhancing tax efficiency—such as broadening the tax base and reducing exemptions—could boost revenue without increasing rates. These measures, combined with disciplined spending, are essential to stabilize debt and restore investor confidence.

In conclusion, Brazil’s public debt and fiscal health are at a crossroads. While recent efforts have prevented a debt spiral, structural challenges remain. Policymakers must balance short-term economic support with long-term fiscal discipline, ensuring that debt stabilization does not come at the expense of growth. For investors and observers, the trajectory of Brazil’s fiscal health will be a key indicator of its economic resilience in the coming years.

Brazil's Duality: Exploring Its Strengths and Weaknesses as a Nation

You may want to see also

Frequently asked questions

Brazil's GDP growth has been modest, with fluctuations due to global economic conditions, domestic political instability, and commodity price volatility. In recent years, growth has averaged around 1-2%, with occasional setbacks during crises like the COVID-19 pandemic.

Agriculture is a cornerstone of Brazil's economy, accounting for about 5-6% of GDP and a significant portion of exports. Brazil is a global leader in producing commodities like soybeans, coffee, sugar, and beef, making it a key player in the global food supply chain.

Inflation has been a persistent challenge in Brazil, with rates often exceeding the central bank's target range. High inflation erodes purchasing power, increases borrowing costs, and creates uncertainty for businesses and consumers, though recent monetary policy measures have aimed to stabilize prices.

Brazil's public debt is high, standing at around 80-90% of GDP, largely due to years of fiscal deficits and economic downturns. The government has implemented reforms to improve fiscal sustainability, but challenges remain in balancing spending and revenue.

Brazil's unemployment rate has been elevated, often hovering around 10-12%, with underemployment also a significant issue. Economic slowdowns, informal labor markets, and structural challenges have contributed to persistent joblessness, though recent recovery efforts have shown some improvement.

![Brazil (The Criterion Collection) [Blu-ray]](https://m.media-amazon.com/images/I/81CO0e4BKQL._AC_UY218_.jpg)