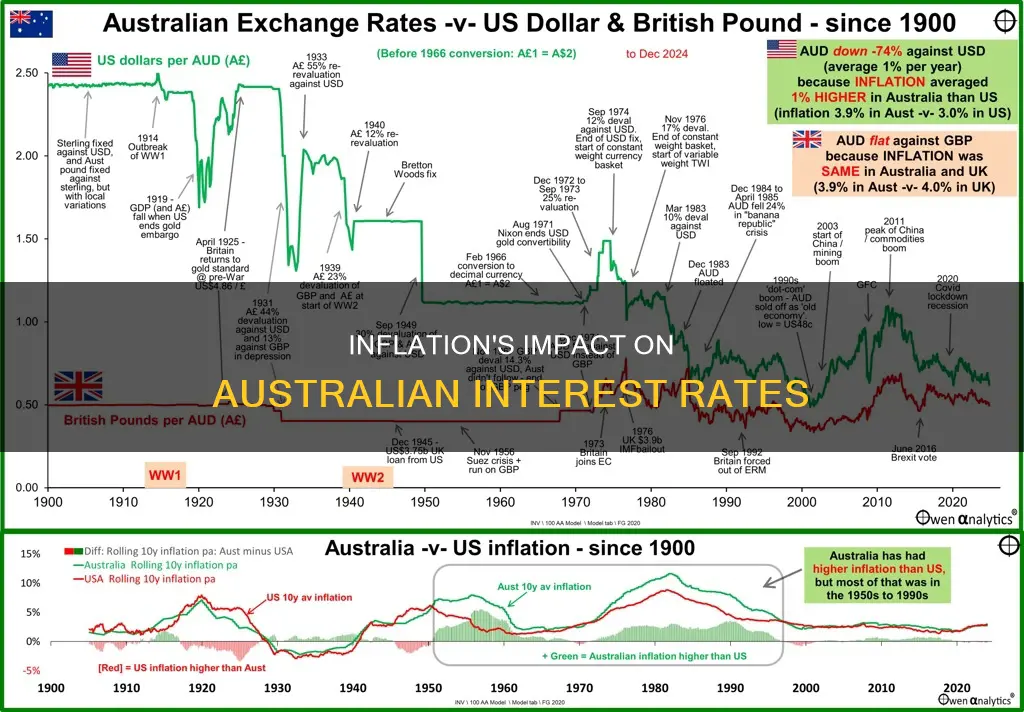

Inflation and interest rates are interconnected and can have a significant impact on each other in the Australian economy. Inflation influences investment decisions, as higher inflation reduces the real return on investments. It can also affect the real interest paid by borrowers to lenders, with higher inflation reducing the purchasing power of interest earnings. Interest rates, on the other hand, can be used to maintain steady inflation by influencing the spending power of the public. In Australia, the Reserve Bank (RBA) adjusts interest rates to control inflation, aiming to keep it within a target range of 2% to 3%. However, when inflation rises above this target, the RBA typically responds by raising interest rates, which can have both positive and negative effects on households, businesses, and the overall economy.

| Characteristics | Values |

|---|---|

| How inflation is measured | Consumer Price Index (CPI) |

| CPI calculation | Tracks cost of goods and services over time, with prices for thousands of items grouped into 87 categories and 11 groups |

| CPI increase | 0.9% this quarter, 2.4% over the twelve months to the March 2025 quarter |

| Inflation target | RBA annual target of 2%–3% |

| Inflation in 2022 | Averaged an expected 6.4% for the calendar year, underlying inflation averaged 4.8% |

| Interest rates and inflation | Interest rates are typically raised during times of high inflation and lowered when inflation slows |

| Interest rates and consumer spending | Higher interest rates lead to reduced consumer spending and increased savings |

| Interest rates and homeownership | Raising interest rates increases the cost of homeownership |

| Interest rates and businesses | Higher interest rates can cause businesses to lower prices |

Explore related products

What You'll Learn

![]()

The Reserve Bank of Australia's role in managing inflation

The Reserve Bank of Australia (RBA) is Australia's central bank and banknote-issuing authority. It has had this role since 14 January 1960, when the Reserve Bank Act 1959 removed the central banking functions from the Commonwealth Bank. The RBA's primary objective, as set out in the Reserve Bank Act 1959, is to maintain price stability.

The RBA uses monetary policy tools, primarily through adjusting the official cash rate, to influence short-term interest rates and help control inflation and support economic growth. The RBA sets the 'cash rate target'—the rate on overnight loans between banks. This then influences the interest rates set by lenders, banks, and financial institutions across the country. The RBA's Monetary Policy Board is responsible for making decisions about monetary policy. The Board meets eight times a year to determine the appropriate monetary policy settings.

If inflation is expected to be higher than the target for a prolonged period, the RBA would typically tighten monetary policy, such as by increasing the cash rate. If inflation is expected to be lower than the target for a sustained period, the RBA would typically loosen monetary policy, such as by lowering the cash rate. The RBA has an inflation target of 2–3% to achieve the goals of price stability, full employment, and the prosperity and welfare of the Australian people. A moderate level of inflation within the target range promotes price stability, which is desirable because it allows consumers and businesses to plan their economic decisions with confidence.

In 2022, the RBA shifted to a phase of aggressive monetary policy tightening to constrain inflation. The RBA Board commenced this phase of monetary policy tightening in May 2022 in response to higher inflation.

Gypsum's Geological Journey: Exploring Australia's Natural Deposits

You may want to see also

Explore related products

![]()

Monetary policy tightening

In 2022, Australia experienced surging inflation, with underlying inflation averaging an expected 4.8%, well above the RBA's target. In response, the RBA Board initiated a phase of monetary policy tightening, aiming to stabilise prices. This involved increasing the 'cash rate target', which is the rate on overnight loans between banks. As a result, interest rates set by lenders, banks, and financial institutions across the country also increased.

The impact of monetary policy tightening is far-reaching. Higher interest rates discourage consumer spending and encourage saving. This decrease in demand can cause businesses to lower their prices, helping to stabilise inflation. However, it also leads to higher costs for borrowers, including those with variable-rate mortgages. Additionally, tighter monetary policies can constrain investment, impacting labour markets and potentially leading to negative wage growth.

While monetary policy tightening can help curb inflation, it also has cost-of-living ramifications. Higher interest rates contribute to budgetary constraints for households, as they face higher mortgage repayments and increased costs for essentials like petrol and groceries. This results in a reduction in disposable income and can put a strain on household budgets.

It's important to note that economics is a complex field, and central banks consider various factors beyond inflation when making decisions about interest rates. These factors include cost of production, raw material costs, employment figures, GDP, and wage growth. Additionally, monetary policy changes can take time to affect the economy, and central banks must carefully consider the potential short-term and long-term impacts of their decisions.

Australian Government Bonds: Safe Investment or Risky Business?

You may want to see also

Explore related products

![]()

How inflation affects consumer spending

Inflation has a significant impact on consumer spending in Australia. When inflation is high, the Reserve Bank of Australia (RBA) typically raises interest rates to curb consumer spending and stabilise the inflation rate. Higher interest rates discourage consumers from spending and taking out loans, as they are more likely to save money. This decrease in demand causes businesses to lower their prices, which helps to stabilise inflation.

On the other hand, when inflation is low, the RBA may lower interest rates to encourage consumer spending. Lower interest rates make borrowing more attractive, increasing demand for goods and services. Businesses may respond by raising prices to take advantage of the high demand.

The RBA's interest rate decisions are based on their target inflation rate of 2-3%. If inflation deviates from this target for a prolonged period, the RBA will adjust monetary policy to correct it. For example, in 2022, when inflation surpassed 7% in the September quarter, the RBA began tightening monetary policy.

However, the relationship between inflation and consumer spending is complex and influenced by various factors. For instance, during the COVID-19 pandemic, high savings rates contributed to strong consumption and inflation in 2021/22. Additionally, wage growth relative to inflation can impact household budgets and spending behaviour. If wages rise slower than inflation, households may feel the financial strain, potentially reducing their spending.

Furthermore, inflation can affect consumer spending indirectly by influencing investment decisions. Higher inflation reduces the real return on investments, discouraging spending and investment, which may negatively impact economic growth.

Ugg Australia: Ethical and Stylish?

You may want to see also

Explore related products

![]()

The impact of inflation on investment decisions

Inflation has a significant impact on investment decisions in the Australian economy. Firstly, a higher inflation rate reduces the real return on investments. This is because inflation erodes the purchasing power of money over time, decreasing the value of future cash flows from investments. As a result, investors may be discouraged from investing, particularly in long-term projects with returns that are further diminished by inflation.

Secondly, inflation influences the cost of borrowing and lending. When inflation is high, central banks like the Reserve Bank of Australia (RBA) typically raise interest rates to curb consumer spending and lending. Higher interest rates make borrowing more expensive, reducing demand for loans and discouraging businesses from investing in new projects. Conversely, lower interest rates during low inflation periods can encourage investment by making borrowing cheaper and more accessible.

The relationship between inflation and interest rates also affects the real interest paid by borrowers to lenders. If inflation is higher than expected when a loan agreement is made, the lender will effectively receive less than anticipated due to the reduced purchasing power of the interest earnings. This dynamic can impact investment decisions, as lenders may become more cautious about lending for certain projects or adjust their expectations for returns.

Additionally, high inflation rates can increase economic uncertainty and affect a country's international competitiveness. Uncertainty about the future direction of the economy may discourage investment, as businesses and investors become more cautious. Moreover, if a country's inflation rate is higher than its trading partners, the goods and services it produces become relatively more expensive, potentially reducing demand and investment in that country.

Finally, monetary policy responses to inflation can directly impact investment decisions. The RBA uses monetary policy tools, such as adjusting interest rates or quantitative easing, to influence economic activity and keep inflation within its target range of 2% to 3%. These policies can affect the availability and cost of credit, impacting businesses' investment plans. For example, tighter monetary policy and higher interest rates may constrain investment by making credit less accessible, as seen in Australia's recent shift towards monetary policy tightening.

Federal Government Services: What Australia Offers Its Citizens

You may want to see also

Explore related products

![]()

The relationship between inflation and interest rates

Inflation and interest rates are closely connected, and changes in one can have a significant impact on the other. Inflation in Australia is measured by the Consumer Price Index (CPI), which tracks the cost of goods and services over time. The Reserve Bank of Australia (RBA) is responsible for overseeing the process of raising or lowering interest rates to maintain a target inflation rate of 2-3%.

When inflation is high, the RBA typically raises interest rates to curb consumer spending. Higher interest rates make borrowing more expensive, which discourages individuals and businesses from taking out loans. This leads to reduced demand for goods and services, causing businesses to lower their prices, which helps stabilize inflation. Additionally, higher interest rates incentivize saving, further reducing consumer spending.

On the other hand, when inflation is low, the RBA may lower interest rates to stimulate the economy. Lower interest rates encourage spending and investment, increasing demand and potentially leading to higher prices. Lower interest rates also make borrowing more attractive, which can further boost economic activity.

In recent years, Australia has experienced surging inflation, partly due to the post-COVID-19 economic environment and global factors such as the war in Ukraine. In response, the RBA has implemented tighter monetary policies, including raising interest rates, to curb inflation and manage the cost-of-living crisis. However, these measures have also contributed to higher mortgage repayments and budgetary constraints for households.

Smoking in Australia: A Declining Trend?

You may want to see also

Frequently asked questions

Inflation and interest rates are closely linked. When inflation is high, the Reserve Bank of Australia (RBA) typically raises interest rates to reduce consumer spending. This makes borrowing more expensive and saving more appealing, which lowers demand for goods and helps to stabilise inflation.

The RBA has an annual target inflation rate of 2-3%. If inflation is expected to be higher than this for a prolonged period, the RBA will typically tighten monetary policy and increase the cash rate.

Inflation can cause a cost-of-living crisis when it rises faster than wages. Inflation can also lead to higher mortgage repayments and increased costs of goods and services.