Brazil, unlike many developed economies, has not traditionally adopted quantitative easing (QE) as a monetary policy tool due to its unique economic and institutional framework. The country’s central bank, Banco Central do Brasil, has historically focused on inflation targeting and maintaining currency stability, particularly given the Brazilian real’s vulnerability to external shocks. However, during the COVID-19 pandemic, Brazil implemented measures akin to QE, albeit indirectly, by expanding its balance sheet through the purchase of government bonds and private sector assets to inject liquidity into the economy. This approach, often referred to as QE-lite, aimed to mitigate the economic impact of the crisis while avoiding the risks of direct currency devaluation and inflationary pressures. Despite these actions, Brazil’s adoption of QE-like policies remains cautious, reflecting its cautious stance toward unconventional monetary measures and the need to balance fiscal sustainability with economic recovery.

Explore related products

What You'll Learn

- Central Bank's Role: Banco Central do Brasil's decision-making process in implementing quantitative easing measures

- Economic Crisis Trigger: How Brazil's economic downturns prompted the need for unconventional monetary policies

- Bond Purchase Mechanism: Details of government bond purchases to inject liquidity into the economy

- Inflation Management: Balancing inflation risks while stimulating economic growth through quantitative easing

- Impact on Currency: Effects of quantitative easing on the Brazilian Real's value and exchange rates

![]()

Central Bank's Role: Banco Central do Brasil's decision-making process in implementing quantitative easing measures

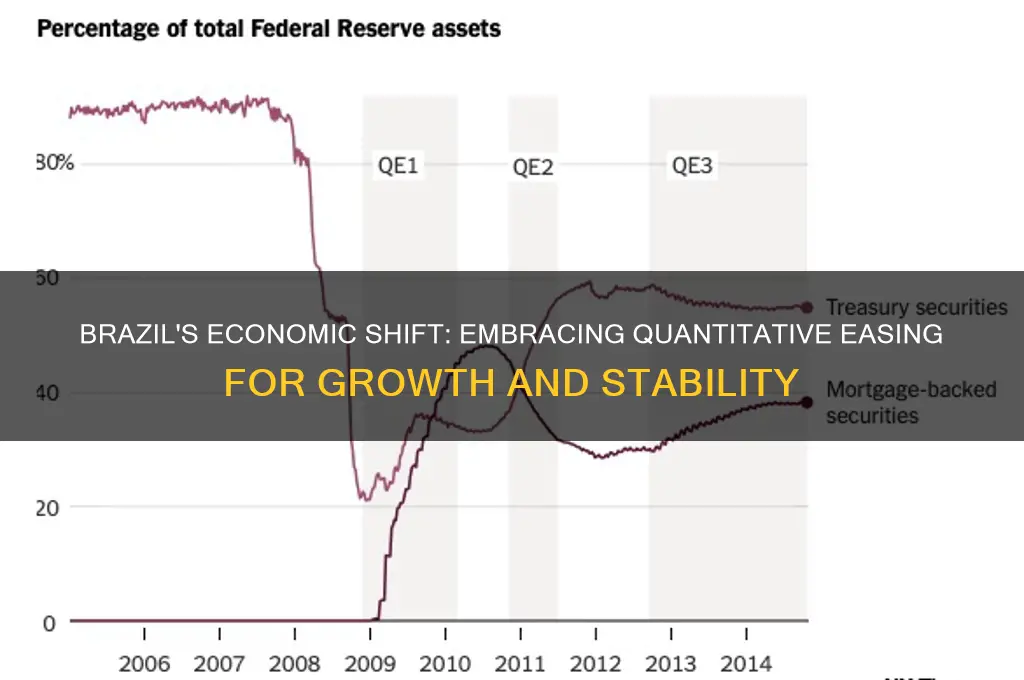

Brazil's adoption of quantitative easing (QE) measures has been a nuanced process, shaped by the Banco Central do Brasil's (BCB) cautious and context-specific decision-making. Unlike the Federal Reserve or the European Central Bank, the BCB has historically prioritized inflation targeting and currency stability, making its approach to QE distinct. The institution's decision to implement QE-like measures, such as purchasing government bonds and private sector assets, was driven by the economic fallout from the COVID-19 pandemic, which necessitated unconventional monetary policies to stimulate liquidity and credit flow.

The BCB's decision-making process begins with a thorough assessment of economic indicators, including inflation rates, unemployment, and GDP growth. During the pandemic, Brazil faced a sharp economic contraction, with GDP declining by 3.3% in 2020. This prompted the BCB to act swiftly, cutting the benchmark Selic rate to a historic low of 2% by August 2020. However, with interest rates nearing their effective lower bound, the BCB explored additional tools, including asset purchases, to inject liquidity into the economy. The bank's communication strategy was critical, as it aimed to signal its commitment to price stability while addressing immediate liquidity needs.

A key aspect of the BCB's QE implementation was its focus on local conditions. Brazil's high public debt and fragile fiscal position constrained the scale and scope of asset purchases. Unlike the Fed's large-scale Treasury and mortgage-backed securities purchases, the BCB primarily targeted government bonds and, to a limited extent, private sector assets like agribusiness receivables certificates. This selective approach aimed to avoid exacerbating inflationary pressures or distorting financial markets. For instance, the BCB's purchases of agribusiness receivables were capped at R$10 billion, reflecting a targeted rather than blanket intervention.

The BCB's decision-making also involved balancing risks, particularly those related to currency depreciation and inflation. Brazil's reliance on commodity exports and its history of hyperinflation made these concerns paramount. To mitigate risks, the BCB coordinated closely with the Ministry of Economy, ensuring that monetary and fiscal policies were aligned. Additionally, the bank maintained a forward guidance framework, emphasizing its commitment to inflation targeting and readiness to adjust policies as needed. This dual focus on stability and flexibility allowed the BCB to navigate the challenges of implementing QE in an emerging market economy.

In conclusion, the Banco Central do Brasil's adoption of quantitative easing measures reflects a pragmatic and tailored approach to monetary policy. By prioritizing local economic conditions, managing risks, and maintaining clear communication, the BCB has effectively utilized QE-like tools to support Brazil's economy during unprecedented times. While the scale of its interventions may pale in comparison to advanced economies, the BCB's strategic decision-making underscores the importance of context in shaping central bank actions. This experience offers valuable insights for other emerging markets considering unconventional monetary policies in response to crises.

Discover Brazil's Surprising Secrets: Facts You Never Knew Before

You may want to see also

Explore related products

![]()

Economic Crisis Trigger: How Brazil's economic downturns prompted the need for unconventional monetary policies

Brazil's economic history is marked by recurrent crises that have forced policymakers to rethink traditional monetary strategies. The 2014–2016 recession, for instance, saw GDP contract by 7%, unemployment surge to 13%, and inflation spike above 10%. These conditions eroded consumer confidence, stifled investment, and depleted foreign reserves. Conventional tools like interest rate adjustments proved insufficient to stimulate demand or stabilize prices, leaving the Central Bank of Brazil (BCB) with few options. This dire scenario set the stage for exploring unconventional measures, including quantitative easing (QE), though Brazil’s approach would differ significantly from developed economies like the U.S. or Japan.

Unlike the U.S. Federal Reserve’s direct asset purchases, Brazil’s adoption of QE-like policies was constrained by structural challenges. High public debt, currency volatility, and a shallow financial market limited the BCB’s ability to expand its balance sheet aggressively. Instead, Brazil employed indirect methods, such as reducing reserve requirements for banks and purchasing private sector assets to inject liquidity. For example, during the COVID-19 crisis, the BCB launched a program to buy corporate bonds and financial bills, aiming to unfreeze credit markets. While not a textbook example of QE, these actions mirrored its spirit by targeting specific sectors to alleviate economic distress.

The decision to adopt such policies was not without risks. Critics argued that increasing the money supply could exacerbate inflation, already a chronic issue in Brazil. However, the BCB prioritized short-term stabilization over long-term inflationary pressures, recognizing that a deeper recession would be more damaging. This pragmatic approach underscores a key takeaway: unconventional monetary policies in emerging markets must be tailored to address unique vulnerabilities, such as currency depreciation and external debt exposure. Brazil’s experience highlights the importance of balancing liquidity support with fiscal discipline to avoid unintended consequences.

A comparative analysis reveals that Brazil’s QE-like measures were more targeted and cautious than those in advanced economies. While the Fed’s asset purchases totaled trillions of dollars, Brazil’s interventions were smaller in scale and focused on specific sectors like small businesses and exporters. This precision was necessary given the country’s fragile fiscal position and reliance on foreign capital. Policymakers also had to navigate political headwinds, as unorthodox policies often face public skepticism in a country with a history of hyperinflation. Despite these challenges, Brazil’s incremental approach demonstrated that unconventional tools can be adapted to emerging market contexts, albeit with careful calibration.

In practical terms, Brazil’s experiment with QE-like policies offers lessons for other developing nations facing similar crises. First, central banks must assess the depth and liquidity of their financial markets before implementing large-scale asset purchases. Second, coordination with fiscal authorities is essential to ensure that monetary expansion does not undermine debt sustainability. Finally, clear communication is critical to manage expectations and maintain credibility. For Brazil, the journey toward unconventional monetary policies was not just a response to economic downturns but also a test of institutional resilience in the face of unprecedented challenges.

Donna Brazile's Book Deal: Unveiling the Financial Details and Impact

You may want to see also

Explore related products

![]()

Bond Purchase Mechanism: Details of government bond purchases to inject liquidity into the economy

Brazil's adoption of quantitative easing (QE) through its bond purchase mechanism is a strategic move to stimulate economic activity by increasing liquidity. Unlike traditional monetary policies that primarily adjust interest rates, QE involves the central bank directly purchasing government bonds from financial institutions. This process injects cash into the banking system, encouraging lending and investment. For instance, during the 2020 economic downturn caused by the COVID-19 pandemic, the Central Bank of Brazil (BCB) initiated a series of bond purchases totaling over R$1 trillion, aiming to stabilize financial markets and support credit flow to businesses and households.

The mechanics of Brazil’s bond purchase mechanism are straightforward yet impactful. The BCB buys government bonds, such as those issued by the National Treasury, from banks and other financial institutions. These purchases are funded by crediting the sellers’ reserve accounts, effectively increasing the money supply. The scale and pace of these purchases are critical; during crises, the BCB has accelerated its buying to provide immediate liquidity. For example, in 2020, the BCB conducted weekly bond auctions, purchasing a mix of short-term and long-term securities to ensure broad market impact. This approach not only lowers long-term interest rates but also signals the central bank’s commitment to economic stability.

One key consideration in Brazil’s QE strategy is the choice of bonds to purchase. The BCB focuses on federal government bonds, which are considered low-risk and highly liquid. This ensures that the injected liquidity reaches the broader economy efficiently. Additionally, the BCB has occasionally included private sector securities, such as debentures, to directly support corporate financing. However, this expansion comes with risks, as it requires careful assessment of credit quality to avoid moral hazard. The BCB’s selective approach ensures that QE remains a tool for macroeconomic stabilization rather than a bailout mechanism.

Critics argue that Brazil’s bond purchase mechanism could lead to inflationary pressures or currency devaluation if not managed carefully. To mitigate these risks, the BCB has implemented safeguards, such as sterilizing operations, where it sells short-term securities to absorb excess liquidity. Moreover, the BCB closely monitors inflation expectations and adjusts the pace of bond purchases accordingly. For instance, as economic conditions improved in late 2021, the BCB gradually reduced its bond-buying program, signaling a return to conventional monetary policy. This calibrated approach highlights the importance of flexibility and vigilance in QE implementation.

In conclusion, Brazil’s bond purchase mechanism is a powerful tool for injecting liquidity into the economy, particularly during crises. By purchasing government bonds, the BCB effectively lowers borrowing costs, stimulates lending, and supports economic recovery. However, the success of this strategy hinges on careful execution, including the selection of securities, the pace of purchases, and the management of potential risks. As Brazil continues to navigate economic challenges, its QE framework serves as a model for emerging markets seeking to balance growth with stability.

Properly Storing Soaked Brazil Nuts: Tips for Freshness and Crunch

You may want to see also

Explore related products

![]()

Inflation Management: Balancing inflation risks while stimulating economic growth through quantitative easing

Brazil's adoption of quantitative easing (QE) presents a delicate dance between fostering economic growth and taming inflationary pressures. While QE injects liquidity into the economy by purchasing government bonds, its effectiveness hinges on meticulous management to avoid overheating.

A key challenge lies in calibrating the dosage. Excessive bond purchases can flood the market with money, driving up prices and eroding purchasing power. Brazil's Central Bank must carefully assess the economy's absorptive capacity, considering factors like existing debt levels, inflation expectations, and the transmission mechanism of monetary policy.

Unlike developed economies with deeper financial markets, Brazil's QE implementation requires a nuanced approach. Direct purchases of private sector assets, such as corporate bonds, could be explored to stimulate investment and credit flow to businesses. This targeted approach can mitigate inflationary risks by channeling liquidity towards productive sectors rather than fueling speculative bubbles.

A crucial aspect of successful QE in Brazil is clear communication. The Central Bank must transparently communicate its objectives, targets, and exit strategy to anchor inflation expectations and maintain market confidence. Regular updates and data-driven adjustments are essential to navigate the dynamic economic landscape.

Ultimately, Brazil's QE journey demands a vigilant and adaptive approach. By carefully managing the dosage, exploring targeted asset purchases, and fostering transparent communication, the Central Bank can harness the growth-stimulating potential of QE while effectively managing inflation risks, paving the way for a more resilient and prosperous economy.

Taylor's Brazil Incident: Unraveling the Shocking Events and Aftermath

You may want to see also

Explore related products

![]()

Impact on Currency: Effects of quantitative easing on the Brazilian Real's value and exchange rates

Brazil's adoption of quantitative easing (QE) measures has been a cautious and context-specific approach, influenced by its historical struggles with inflation and currency volatility. Unlike advanced economies, Brazil’s central bank, Banco Central do Brasil, has not engaged in large-scale asset purchases akin to the U.S. Federal Reserve or the European Central Bank. Instead, Brazil’s QE-like policies have focused on targeted liquidity injections, such as reducing reserve requirements for banks and providing credit facilities to specific sectors during crises, like the COVID-19 pandemic. These measures aim to stimulate lending without directly flooding the economy with excess liquidity, a critical distinction given Brazil’s sensitivity to inflationary pressures.

The impact of these QE-like policies on the Brazilian Real (BRL) has been multifaceted. On one hand, increased liquidity can weaken the currency by diluting its value relative to foreign currencies, particularly if investors perceive the measures as inflationary. For instance, during the pandemic, the Real depreciated significantly against the U.S. Dollar, partly due to global risk-off sentiment but also because of concerns about Brazil’s fiscal health and the potential inflationary effects of monetary easing. On the other hand, targeted QE measures can stabilize the currency by ensuring financial market liquidity and preventing credit crunches, which could otherwise exacerbate economic downturns and further devalue the Real.

A comparative analysis with other emerging markets reveals that Brazil’s currency response to QE-like policies is shaped by its unique macroeconomic environment. Unlike countries with stronger institutional frameworks or more diversified economies, Brazil’s reliance on commodity exports makes the Real particularly vulnerable to external shocks. QE measures that boost domestic liquidity can temporarily support economic activity but may also widen the current account deficit if imports surge, putting additional downward pressure on the currency. This dynamic underscores the delicate balance Brazil must strike between monetary stimulus and currency stability.

Practical takeaways for investors and policymakers include monitoring inflation expectations and fiscal sustainability as key determinants of the Real’s performance during QE periods. For instance, if QE-like measures are accompanied by credible fiscal consolidation efforts, the negative impact on the currency can be mitigated. Additionally, investors should watch for signals from Banco Central do Brasil regarding the duration and scale of liquidity injections, as prolonged easing could erode confidence in the Real. Hedging strategies, such as currency forwards or options, may be advisable for those exposed to BRL volatility during such periods.

In conclusion, while Brazil’s QE-like policies have provided a necessary buffer against economic shocks, their impact on the Real’s value and exchange rates hinges on a complex interplay of domestic and external factors. Policymakers must navigate this terrain carefully, ensuring that liquidity support does not undermine the currency’s stability or reignite inflationary pressures. For market participants, understanding these dynamics is crucial for managing risks and capitalizing on opportunities in Brazil’s evolving monetary policy landscape.

Exploring Brazil's Rich Cultural Traditions: Festivals, Food, and Celebrations

You may want to see also

Frequently asked questions

Quantitative easing is a monetary policy tool where a central bank purchases long-term securities to increase the money supply and stimulate economic activity. Brazil has not formally adopted QE as practiced by countries like the U.S. or Japan. Instead, the Central Bank of Brazil (BCB) has used other tools, such as adjusting interest rates and reserve requirements, to manage liquidity and inflation.

Brazil has not adopted QE due to concerns about inflation, currency devaluation, and the potential for financial instability. The country’s history of high inflation makes unconventional policies like QE risky. Additionally, Brazil’s economy relies heavily on foreign investment, and QE could lead to capital outflows and weaken the Brazilian real.

While QE remains unlikely in Brazil, the Central Bank could consider it in extreme economic crises. Currently, Brazil relies on traditional monetary policies, such as adjusting the Selic rate (benchmark interest rate), and fiscal measures to stabilize the economy. The BCB also focuses on maintaining credibility in its inflation-targeting regime to avoid the need for unconventional measures like QE.