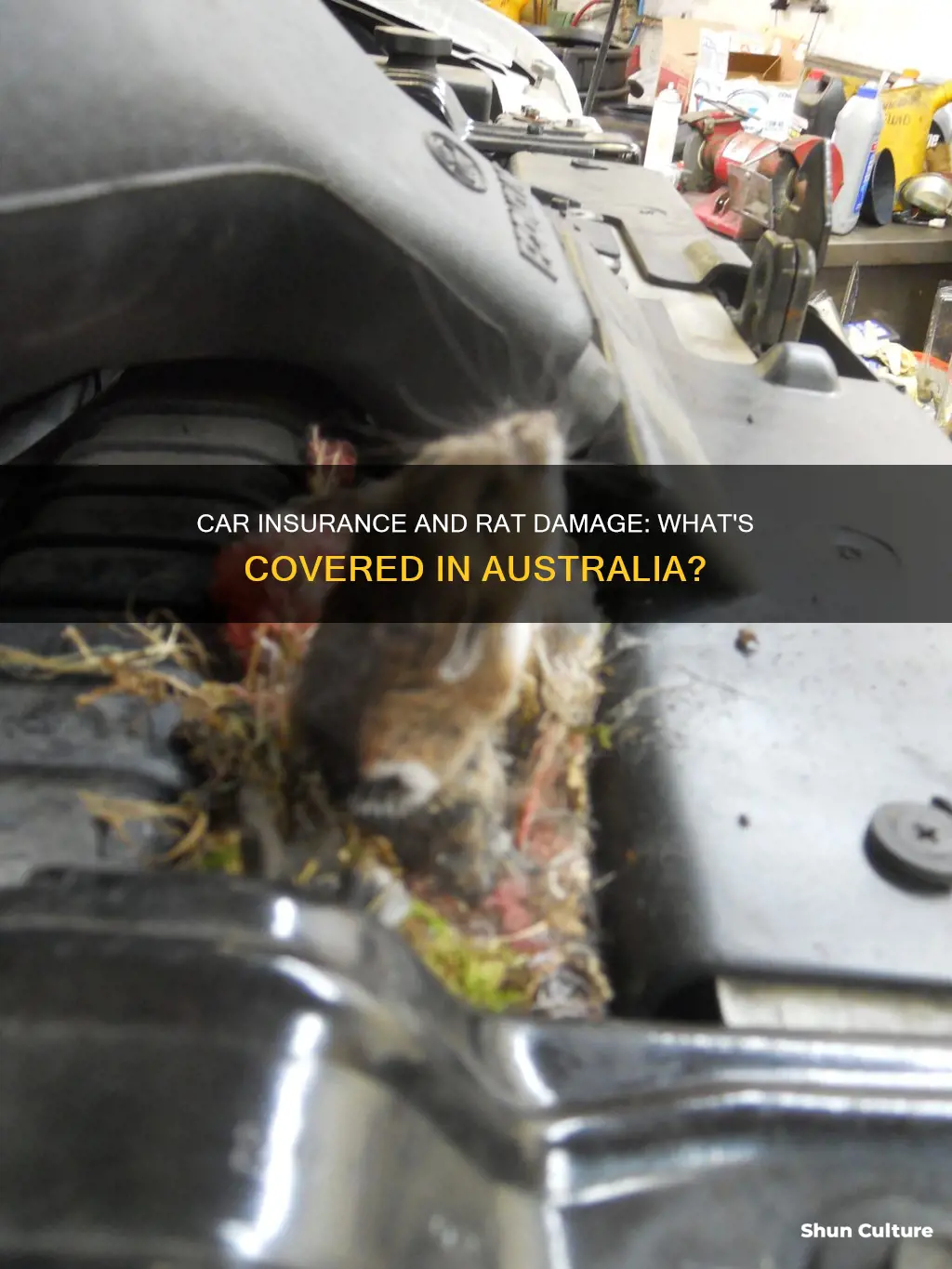

Rats and mice are responsible for about 200 insurance claims a year in Australia, with the rodents chewing through plastic parts and electrical wires under the bonnet. They also sometimes get inside the car and eat through seatbelts and upholstery. So, does car insurance cover rat damage in Australia? Well, it depends on the type of car insurance you buy and the rules of the specific policy you are sold. Most incidents involving animal damage, including rodents chewing on wires, are covered by comprehensive auto insurance. However, damage from rodents is generally not covered by homeowners or renters insurance, and some policies exclude vermin damage altogether.

| Characteristics | Values |

|---|---|

| Insurance coverage for rat damage in Australia | Not covered by home, renters, or homeowners insurance. May be covered by comprehensive car insurance. |

| Common types of rat damage to cars | Chewed wiring, damage to seatbelts and upholstery, airbag and warning lights, air conditioning, brakes, and vehicle acceleration. |

| Ways to prevent rat damage | Use "rodent tape" or chemical deterrents with bitter or sour sprays. Move your car regularly to prevent rats from moving in. |

| What to do if your insurance claim is rejected | Contact the insurance provider in writing and explain why your claim was unsuccessful. If you're not happy with their answer, follow the provider's internal dispute resolution process. If you're still unsatisfied, make a complaint to the car insurance ombudsman. |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Comprehensive car insurance

Some insurance companies cover rat damage under comprehensive car insurance. Rat attacks can cause electrical malfunction due to the biting of electrical wiring, which is considered unforeseen accidental damage. However, some insurers may deem rat damage as long-term damage and deny the claim. It is important to note that each insurer has different policies, and it is essential to familiarise yourself with the coverage before purchasing.

When it comes to other types of damage, comprehensive car insurance usually covers vandalism, such as scratches or graffiti on your vehicle. It also covers accidental damage to your windscreen and may waive the vehicle excess if the glass can be repaired. Additionally, if your car is stolen, comprehensive insurance will likely provide a similar rental car until your stolen vehicle is found or your claim is resolved.

Exploring Australia's Vast Second-Largest State

You may want to see also

Explore related products

![]()

Deductibles

In Australia, comprehensive car insurance policies typically cover damage caused by rat attacks that lead to electrical malfunctions. This includes rats chewing on electrical wiring, which is a common issue. However, it's important to note that third-party insurance does not usually cover such incidents.

When it comes to deductibles, it's important to understand that they represent your "percentage of risk" in an auto insurance policy. While having a higher deductible is not inherently negative, it's crucial to ensure that you can afford it in case of an unforeseen event. For instance, if the cost of repairing wire damage caused by rats is lower than your deductible, you will be responsible for the entire bill.

The necessity of paying a deductible depends on the extent of the damage and the specific terms of your comprehensive insurance policy. If the damage is deemed "sudden and accidental," it may be covered by your policy. However, if the damage is considered long-term, your claim might be rejected, and you would need to bear the cost of repairs yourself.

It's worth noting that insurance companies may deny claims if they believe the infestation resulted from poor vehicle maintenance, risky storage practices, or negligence in upkeep. Therefore, it's essential to regularly inspect and maintain your vehicle, especially during winter when rodent infestations are more prevalent.

Additionally, understanding your insurance coverage is crucial. While comprehensive insurance typically covers rat-inflicted damage, it is not automatically included in all auto insurance policies. It may need to be added as an add-on, similar to collision insurance. Reviewing your policy documents and consulting your insurance provider can help clarify what is covered and what falls under your deductible.

Tinder in Australia: Is It Really Free to Use?

You may want to see also

Explore related products

![]()

Home and contents insurance

While standard home insurance policies in Australia generally exclude rat damage, some companies offer specialised pest control insurance or specific rodent insurance. These policies can provide coverage for the costs of rat removal and repairing damage caused by rats, which can be substantial due to their ability to chew through various materials, including metal, PVC pipes, drywall, and wood.

To prevent rat infestations, it is essential to take proactive measures. Rats can enter homes through very small openings, so blocking potential entry points, maintaining good housekeeping practices, and regularly inspecting your property for signs of infestation are crucial steps in rat prevention.

It is important to carefully review your home insurance policy to understand what is covered and excluded regarding animal damage. Some policies may provide coverage for damage caused by wild animals that accidentally become trapped inside your home. Additionally, damage caused by pets may be covered under certain circumstances, such as under 'Fire (including bushfire)' or 'Escape of liquid'.

In summary, while standard home and contents insurance in Australia typically excludes rat damage, there may be specific scenarios or additional coverage options that provide some protection. Preventative measures and a thorough understanding of your insurance policy are key to safeguarding your home against rat infestations and their potential financial implications.

Australian Sea Lion Diet: What Do They Eat?

You may want to see also

Explore related products

![]()

Prevention

Rats and mice are responsible for about 200 insurance claims a year in Australia, according to an investigation by WhichCar. Rats are the prime culprits, chewing on plastic parts under the bonnet and causing extensive damage. They also tend to nest under the bonnet, and their droppings can be found in the engine compartment.

- Regularly check your vehicle for signs of rodent damage or infestation. These signs may include chewed wires, droppings under the vehicle's bonnet or interior, or nesting materials in the same location.

- If you notice any damage or droppings in the engine compartment, leave your hood up at night for the first 1-2 weeks and then 2-3 times a week thereafter. This eliminates the engine compartment as a potential nesting ground by reducing warmth and increasing moisture and light.

- Use snap traps to block off the entrances that rodents use to enter the car, such as climbing up the tread of the tires.

- If you suspect a rodent problem, wear protective rubber gloves and inspect and clean the car's exterior. Rodents can carry diseases, so it is important to take precautions when handling any nesting materials or droppings.

- Spray any nests or signs of infestation with a disinfectant (not bleach) and let it sit for five minutes. Then, wear disposable gloves and use paper towels to remove the nest or droppings. Clean the area again and wash your hands before and after removing the gloves.

- If you find rodents or droppings in the vehicle's air intake, dispose of and replace the air filter.

- Honda's "Motor Tape," infused with capsaicin, can deter rodents from chewing through wires. While it is not cheap to install, it is less expensive than installing a new electric system.

- Rats are cautious and will be deterred from unfamiliar places or situations. They also tend to follow the same paths and eat in the same places. You can use this knowledge to block their paths or disrupt their familiar eating places.

Plumbing in Australia: A Lucrative Career Choice?

You may want to see also

Explore related products

![]()

What to do if your claim is rejected

While car insurance is meant to cover you in case of accidents, theft, or damage, there are certain exclusions. These exclusions vary depending on the type of car insurance you buy and the rules of the specific policy you are sold. If your claim is rejected, here are some steps you can take:

Understand the reason for rejection

First, it is important to understand why your claim was rejected. You will typically receive a denial letter from your insurer, which will include supporting evidence for the decision. Common reasons for claim denial include failure to pay your insurance premium on time, lack of coverage, or policy exclusions.

Review your policy documents

Carefully review your policy documents, including your schedule and product disclosure statement. This will help you understand what you are covered for and what is excluded from your coverage. If you have trouble understanding your policy or feel that the wording is unfair or confusing, consider seeking legal advice.

Contact your insurance provider

If you feel that your claim was rejected unfairly, you can contact your insurance provider in writing to explain why your claim was unsuccessful. They may have additional information or evidence that influenced their decision. It is important to understand their reasoning before proceeding further.

Use the internal dispute resolution process

If you are not satisfied with your insurance provider's response, you can utilize their internal dispute resolution (IDR) process. This process should be outlined on their website and in their documentation. It provides an avenue to dispute the insurer's decision and potentially reach a resolution.

Complain to the Australian Financial Complaints Authority (AFCA)

If you are still not satisfied with the outcome, you can escalate the matter to the Australian Financial Complaints Authority (AFCA). AFCA handles complaints by individuals against car insurers. They will review your case and may compel your insurance provider to pay your claim if your complaint is successful.

Seek legal advice

If all else fails, you may consider seeking suitably qualified legal advice. A lawyer can help you understand your rights and explore other options, such as applying to a tribunal or taking the matter to court. However, keep in mind that there may be costs involved, and you may have to pay the other side's legal fees depending on the outcome.

Transfer Money from Australia to a UK Bank Account

You may want to see also

Frequently asked questions

It depends on your insurance policy. Comprehensive auto insurance generally covers rat damage, but not all insurance policies include this coverage. If you have a high deductible, the cost of repairs may be lower than your deductible, and insurance won't cover you.

Rats and mice are known to chew on plastic parts, seatbelts, upholstery, and wiring in cars. They also like to nest under the bonnet. This can cause warning lights to go on, air conditioning to stop working, brakes to fail, and vehicles to be unable to accelerate.

If your insurance claim is rejected, you can contact the insurance provider in writing to explain why your claim was unsuccessful. If you are still not satisfied with their response, you can use the provider's internal dispute resolution process, and if necessary, contact the Australian Financial Complaints Authority (AFCA).