Brazil operates under a worldwide taxation system, meaning Brazilian citizens and residents are subject to income tax on their global earnings, regardless of where the income is generated. This includes salaries, business profits, and other forms of income earned in foreign countries. However, Brazil has established tax treaties with several nations to prevent double taxation, allowing taxpayers to claim credits for taxes paid abroad. Despite these treaties, navigating the complexities of international taxation requires careful consideration of both Brazilian tax laws and the regulations of the country where the income is earned, making professional guidance often essential for compliance.

| Characteristics | Values |

|---|---|

| Tax Residency | Brazil taxes its residents on their worldwide income, regardless of where it is earned. |

| Non-Resident Taxation | Non-residents are taxed only on Brazilian-sourced income. |

| Tax Year | Calendar year (January 1 to December 31). |

| Progressive Tax Rates | Tax rates range from 0% to 27.5% on income earned abroad, depending on the amount. |

| Foreign Tax Credit | Brazil allows a foreign tax credit to avoid double taxation, limited to the Brazilian tax due on the foreign income. |

| Reporting Requirements | Residents must declare all foreign income and assets in their annual tax return. |

| Controlled Foreign Corporations (CFC) | Income from controlled foreign corporations may be subject to taxation in Brazil if certain conditions are met. |

| Tax Treaties | Brazil has tax treaties with several countries to prevent double taxation and facilitate tax cooperation. |

| Penalties for Non-Compliance | Failure to report foreign income can result in fines, interest, and other penalties. |

| Recent Updates (as of latest data) | No significant changes in 2023; however, taxpayers should monitor updates from Receita Federal (Brazilian tax authority). |

Explore related products

What You'll Learn

- Tax Residency Rules: Criteria defining who is considered a tax resident in Brazil

- Double Taxation Agreements: Treaties preventing dual taxation on foreign-earned income

- Reporting Requirements: Obligations for declaring foreign income to Brazilian authorities

- Progressive Tax Rates: How Brazil’s tax brackets apply to worldwide income

- Exemptions and Deductions: Allowances for foreign taxes paid or specific income types

![]()

Tax Residency Rules: Criteria defining who is considered a tax resident in Brazil

Brazil's tax residency rules are pivotal in determining whether individuals are subject to taxation on their worldwide income. The primary criterion for tax residency is physical presence: spending more than 183 days in Brazil within a 12-month period automatically classifies an individual as a tax resident. This rule is straightforward but requires meticulous tracking of days spent in the country, especially for those frequently traveling across borders. For expatriates and digital nomads, this threshold is critical, as exceeding it triggers the obligation to report and pay taxes on all global income to Brazilian authorities.

Beyond the 183-day rule, Brazil also considers the center of vital interests when determining tax residency. This includes factors such as the location of family, economic activities, and permanent residence. For instance, if an individual maintains a home, conducts business, or has dependents in Brazil, they may be deemed a tax resident even if they spend fewer than 183 days in the country. This criterion is more subjective and requires a case-by-case analysis, making it essential for individuals to consult tax professionals to avoid unintended tax liabilities.

A lesser-known aspect of Brazil’s tax residency rules is the treatment of government officials and employees of Brazilian companies working abroad. Even if these individuals spend the majority of their time outside Brazil, they may still be considered tax residents if their work is directly tied to Brazilian interests. This exception highlights the extraterritorial reach of Brazil’s tax laws and underscores the importance of understanding the nuances of tax residency, especially for those in diplomatic or corporate roles.

For dual citizens or individuals with ties to multiple countries, Brazil’s tax residency rules can create complexities. Brazil operates under a territorial system for non-residents, taxing only income sourced within the country. However, residents are taxed on their worldwide income, including earnings from abroad. To mitigate double taxation, Brazil has tax treaties with several countries, but these agreements often require proof of tax residency in the other jurisdiction. Navigating these overlapping rules demands careful planning and documentation to ensure compliance without overpaying taxes.

In practice, individuals must proactively manage their tax residency status by maintaining detailed records of their days in Brazil and understanding the broader implications of their personal and professional ties to the country. For example, a Brazilian citizen working remotely from Portugal might mistakenly assume they are no longer a Brazilian tax resident if they stay abroad for more than 183 days. However, if their family and primary assets remain in Brazil, they could still be considered a tax resident. Such scenarios emphasize the need for a holistic approach to tax planning, combining legal advice with practical record-keeping to align with Brazil’s residency criteria.

Is Brazil a First World Country? Exploring Its Global Standing

You may want to see also

Explore related products

$19.99

![]()

Double Taxation Agreements: Treaties preventing dual taxation on foreign-earned income

Brazil, like many countries, operates under a worldwide income taxation system, meaning Brazilian citizens and residents are taxed on their global income, regardless of where it is earned. This raises the critical issue of double taxation—when the same income is taxed both in the country where it is earned and in Brazil. To mitigate this, Brazil has established Double Taxation Agreements (DTAs) with numerous countries, ensuring that individuals and businesses are not unfairly burdened by paying taxes twice on the same income.

DTAs are bilateral treaties designed to allocate taxing rights between two countries, providing clarity on which country can tax specific types of income. For instance, if a Brazilian citizen works in Germany, the DTA between Brazil and Germany will determine whether the income is taxed in Germany, Brazil, or both, and at what rates. These agreements typically follow the OECD Model Tax Convention, which serves as a framework for negotiating tax treaties globally. Key provisions in DTAs include rules for residency, permanent establishment, and withholding taxes, ensuring that income is taxed only once or at reduced rates.

One practical example is the Brazil-United Kingdom DTA, which stipulates that employment income is taxable only in the country where the work is performed, provided the individual spends less than 183 days in the other country. Similarly, dividends, interest, and royalties are often subject to reduced withholding tax rates under these treaties. For instance, dividends paid by a UK company to a Brazilian resident may be taxed at a maximum rate of 15% in the UK, instead of the standard 20%, with the remaining tax liability in Brazil adjusted accordingly.

Navigating DTAs requires careful planning and documentation. Taxpayers must claim treaty benefits by providing a certificate of residence and other relevant documents to the tax authorities in both countries. Failure to do so may result in higher tax liabilities or penalties. Additionally, Brazil’s controlled foreign corporation (CFC) rules may still apply to income earned abroad, even under a DTA, if the income is deemed passive or artificially shifted to low-tax jurisdictions.

In conclusion, DTAs are essential tools for Brazilian citizens earning foreign income, offering relief from double taxation while ensuring compliance with international tax standards. Understanding the specific provisions of these treaties and seeking professional advice can help individuals and businesses optimize their tax obligations and avoid pitfalls in cross-border taxation.

Discover Brazil's Country Code: A Quick and Easy Guide

You may want to see also

Explore related products

![]()

Reporting Requirements: Obligations for declaring foreign income to Brazilian authorities

Brazilian residents are subject to taxation on their worldwide income, a principle that extends to earnings generated outside the country. This means that if you're a Brazilian citizen or a foreign national residing in Brazil, you must declare all foreign-sourced income to the Brazilian tax authorities, known as Receita Federal. The reporting requirements are stringent, and failure to comply can result in substantial penalties, including fines and legal consequences.

To declare foreign income, taxpayers must complete the annual Adjusted Annual Income Tax Return (DIRPF). This form requires a detailed breakdown of all income sources, including salaries, investments, and capital gains earned abroad. It's essential to maintain accurate records and supporting documentation, such as bank statements, invoices, and contracts, to substantiate the declared amounts. The deadline for submitting the DIRPF is typically April 30th of each year, covering the income earned in the previous calendar year.

One critical aspect of reporting foreign income is the proper classification of the income type. Brazilian tax law distinguishes between different categories of income, each with its own tax treatment. For instance, employment income is taxed at progressive rates, while investment income may be subject to a flat tax rate. Misclassifying income can lead to incorrect tax calculations and potential audits. Taxpayers should consult the Receita Federal's guidelines or seek professional advice to ensure accurate reporting.

A common challenge for taxpayers is navigating the complex rules surrounding foreign tax credits. Brazil allows residents to claim a credit for taxes paid on foreign-sourced income, but only if the taxes were levied by a country with which Brazil has a double taxation agreement. To claim this credit, taxpayers must provide evidence of the foreign taxes paid, including the tax assessment and payment receipts. It's crucial to carefully review the applicable tax treaties and consult with tax experts to optimize the use of foreign tax credits and minimize double taxation.

In addition to the annual DIRPF, Brazilian residents may also be required to submit periodic reports on their foreign assets, including bank accounts, investments, and real estate holdings. This obligation applies to individuals with aggregate foreign assets exceeding a certain threshold, which is currently set at R$ 1 million (approximately USD 200,000). The reporting requirements for foreign assets are separate from the income tax declaration and involve a distinct set of forms and deadlines. Taxpayers should be aware of these additional obligations to avoid penalties and ensure full compliance with Brazilian tax laws. By staying informed and seeking guidance when needed, individuals can effectively navigate the complexities of reporting foreign income and assets to the Brazilian authorities.

Is Brazil a Communist Country? Unraveling Its Political and Economic System

You may want to see also

Explore related products

$108.92 $229.95

![]()

Progressive Tax Rates: How Brazil’s tax brackets apply to worldwide income

Brazil's tax system operates on a worldwide income basis, meaning Brazilian citizens and residents are taxed on their global earnings, regardless of where the income is generated. This principle is a cornerstone of Brazil's tax legislation, ensuring that all income, whether from domestic or international sources, is subject to Brazilian tax laws. The progressive tax rates in Brazil are designed to tax higher incomes at increasingly higher rates, a system that applies uniformly to both local and foreign-earned income.

Understanding the Tax Brackets

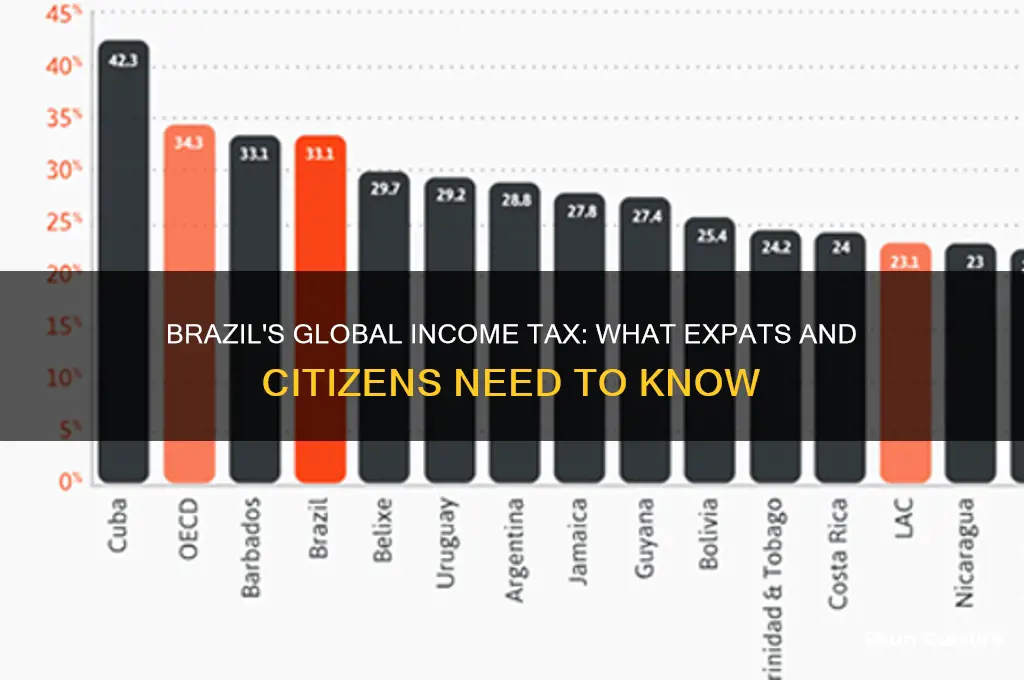

Brazil’s progressive tax rates are structured into five brackets, ranging from 7.5% to 27.5%. For the 2023 tax year, these brackets are as follows:

- 7.5% on annual income up to BRL 28,265.52

- 15% on income between BRL 28,265.53 and BRL 37,687.32

- 22.5% on income between BRL 37,687.33 and BRL 46,643.88

- 27.5% on income above BRL 46,643.88

These rates apply to the total worldwide income of Brazilian taxpayers, including salaries, business profits, dividends, and capital gains earned abroad. For instance, if a Brazilian citizen earns BRL 100,000 annually from a job in Germany, this amount is added to any other income they receive and taxed according to the progressive brackets.

Avoiding Double Taxation

One critical aspect of Brazil’s worldwide income tax system is its approach to double taxation. Brazil allows taxpayers to claim a tax credit for taxes paid on foreign-earned income, provided there is a double taxation treaty in place with the respective country. For example, if a Brazilian resident pays 20% tax in the United States on income earned there, they can deduct this amount from their Brazilian tax liability, ensuring they are not taxed twice on the same income.

Practical Tips for Compliance

For Brazilian citizens earning income abroad, meticulous record-keeping is essential. Maintain detailed documentation of all foreign earnings, taxes paid, and applicable treaties. Use tax software or consult a tax professional to accurately calculate your worldwide income and apply the progressive rates. Additionally, be aware of reporting deadlines: Brazil’s annual tax return (Declaração de Ajuste Anual) must be filed by April 30th, with penalties for late or incorrect submissions.

Comparative Perspective

Compared to countries with territorial tax systems, such as the United States for certain types of income, Brazil’s approach is more comprehensive but also more complex. While it ensures a broader tax base, it requires taxpayers to navigate international tax laws and treaties. For high-earners, the top rate of 27.5% on worldwide income can be a significant consideration, especially when combined with foreign tax obligations.

In summary, Brazil’s progressive tax rates apply uniformly to worldwide income, with mechanisms in place to mitigate double taxation. Understanding the brackets, leveraging tax credits, and staying compliant are key to managing tax obligations effectively for Brazilian citizens earning income abroad.

US Visa Holders from India: Brazil Visa Requirements Explained

You may want to see also

Explore related products

![]()

Exemptions and Deductions: Allowances for foreign taxes paid or specific income types

Brazil's tax system acknowledges the complexities of cross-border income, offering exemptions and deductions to prevent double taxation and provide relief for specific income types. One key mechanism is the foreign tax credit, which allows Brazilian residents to offset taxes paid abroad against their Brazilian tax liability. For instance, if a Brazilian citizen earns income in Germany and pays €20,000 in taxes there, they can claim this amount as a credit when filing their Brazilian tax return, reducing their overall tax burden. This ensures that income is not taxed twice, fostering fairness and compliance.

However, the foreign tax credit is not unlimited. It is capped at the amount of Brazilian tax due on the foreign income. For example, if the Brazilian tax on the German income is R$50,000 and the foreign tax paid is R$60,000, the credit is limited to R$50,000. The excess R$10,000 cannot be carried forward or refunded, making it crucial for taxpayers to carefully calculate their liabilities in both jurisdictions. This limitation underscores the importance of strategic tax planning for those with international income streams.

Beyond foreign tax credits, Brazil also provides exemptions for specific types of foreign income. For instance, income derived from certain international organizations, such as the United Nations, may be exempt from Brazilian taxation. Similarly, pensions and social security benefits received from foreign governments often qualify for exemption, provided they meet specific criteria. These exemptions are designed to align Brazil’s tax policies with international norms and treaties, ensuring that citizens are not disproportionately burdened by their global earnings.

Practical tips for navigating these allowances include maintaining detailed records of foreign taxes paid, as well as documentation supporting the nature and source of foreign income. Taxpayers should also consult Brazil’s tax treaties with other countries, as these agreements often contain provisions for additional exemptions or reduced withholding rates. For example, the Brazil-U.S. tax treaty includes provisions for lower withholding rates on dividends and interest, which can significantly reduce the overall tax burden for individuals with U.S.-sourced income.

In conclusion, while Brazil taxes its citizens on their worldwide income, the system incorporates exemptions and deductions to mitigate the impact of double taxation and recognize the unique nature of certain foreign earnings. By understanding and leveraging these allowances, taxpayers can optimize their tax positions and ensure compliance with both Brazilian and international tax laws. Proactive planning and thorough documentation are essential to maximizing these benefits.

Brazil Visa Cost for Canadians: Fees and Application Guide

You may want to see also

Frequently asked questions

Yes, Brazil taxes its citizens on their worldwide income, including income earned in other countries, under the principle of residency-based taxation.

Yes, Brazil allows foreign tax credits to avoid double taxation. If taxes are paid on foreign income in another country, the amount can be credited against Brazilian tax liability, up to the limit of Brazilian tax due on that income.

Yes, Brazilian citizens living abroad are still required to file annual tax returns in Brazil if they meet the criteria for tax residency, which includes maintaining economic or family ties in Brazil. However, they may qualify for tax exemptions or reductions depending on their situation.

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)