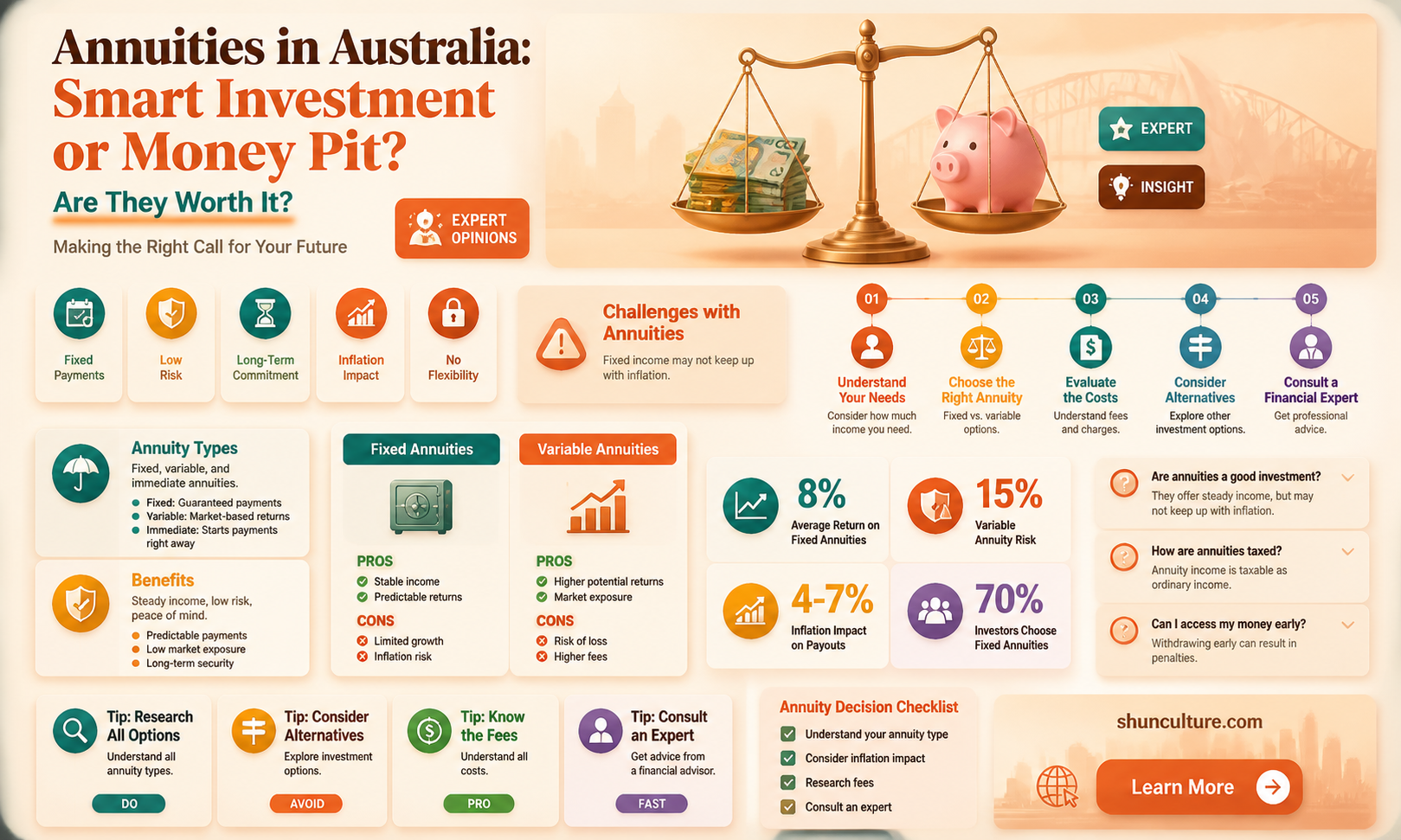

Annuities are a form of retirement income product that provides a steady income stream in retirement. They are not very popular in Australia, with less than 4% of retired Australians investing in them. However, they can be a good option for those seeking income security and peace of mind. Annuities are typically offered by superannuation and insurance companies, and they guarantee regular payments for either a fixed term or life. While annuities provide stability, they lack flexibility, and it is challenging to withdraw funds early. This piece will explore the benefits and drawbacks of annuities as an investment option for Australians and how they compare to other retirement income products.

| Characteristics | Values |

|---|---|

| Popularity in Australia | Annuities are not very popular in Australia compared to other countries like the US and UK. Less than 4% of retired Australians invest in annuities, while more than 80% use account-based pensions. |

| Benefits | Annuities provide a guaranteed, regular income for a fixed period or lifetime, protecting against longevity risk. They are stable and secure, unaffected by market volatility or crashes. |

| Drawbacks | Annuities lack flexibility, with funds typically locked in and early withdrawal incurring penalties. They may provide lower income than market-linked investments and are complex with varying product conditions. |

| Types | Fixed Term or Lifetime Annuities, Conventional Annuities, Investment-Linked Annuities, and more. |

| Considerations | Annuities may not suit those with lower wealth or poor health. Seek independent financial advice and compare products. |

Explore related products

What You'll Learn

![]()

Annuities vs. account-based pensions

Annuities and account-based pensions are two different types of retirement income products. Annuities are a form of insurance that provides a guaranteed income stream, while account-based pensions are an investment product that provides a flexible income stream.

With an annuity, you typically purchase it with a lump sum, and it provides a guaranteed income for a fixed period or your lifetime. The income payments may be adjusted for inflation, and you can choose to have a beneficiary continue receiving payments after your death. Annuities are less flexible than account-based pensions, but they offer greater certainty about future income. They are also less affected by market performance, making them a more stable option.

On the other hand, account-based pensions are a common choice for retirement income. They offer regular, flexible, and tax-effective income from your superannuation. You can choose how your fund invests your money, and there are flexible payment options. However, unlike annuities, account-based pensions are not a guaranteed income for life and can be depleted to zero before the end of your life. Account-based pensions are also more exposed to market risks, which can result in higher returns or potential losses.

Both options have their advantages and disadvantages, and it is essential to consider your personal needs and circumstances before making a decision. Some people choose a hybrid approach, including both annuities and account-based pensions in their retirement income portfolio. It is always recommended to seek independent financial advice to determine which option is best suited to your circumstances.

Huel's Australian Shipping: Is It Available?

You may want to see also

Explore related products

![]()

Pros and cons of annuities

Annuities are a form of retirement income product, providing a stream of income in retirement years. They are generally bought from a life insurance provider or a super fund. Annuities are almost universally described as "guaranteed", meaning that a market crash won't affect retirement income.

Pros of Annuities

Annuities can provide a reliable, secure, and steady income for either the rest of your life or a fixed period. This is especially useful if you want to ensure a steady income for everyday costs throughout your retirement. Annuities can be structured to return your investment earnings at the end of the agreed term, in regular payments over the agreed term, or your life, or a combination of these. Annuities can also be customised to match the buyer's needs, such as a death benefit provision or a joint and survivor annuity.

Cons of Annuities

Annuities often have high fees compared to mutual funds, ETFs, and other investments. There is also a risk of losing your money if the insurance company goes broke. There is very little flexibility with annuities, and you may be locked into the product and unable to withdraw any funds early. There may be significant penalties for withdrawing your money as a lump sum. Your payments might not keep up with inflation, and there may be high surrender fees if you need to withdraw money before a certain period of time has elapsed.

Central Australia's Unique Plant Life

You may want to see also

Explore related products

$40 $74

![]()

Investment-linked annuities

Annuities are a form of retirement income product that provides a steady income stream during retirement years. They are purchased from a life insurance provider or a super fund. While annuities are not very popular in Australia, they are a very good fit for retirement income. Investment-linked annuities are a new breed of retirement income product in Australia, providing longevity protection and a choice of investments to support that income.

With an investment-linked annuity, the retiree's annual income moves up or down to reflect changes in the value of a selected investment option. This is in contrast to a conventional annuity, where regular payment amounts are not affected by market performance and are instead guaranteed for the term of the annuity. With an investment-linked annuity, each year's income varies based on the performance of a selected investment option, rather than as a specific dollar amount of income. This gives retirees the opportunity to benefit from market growth over time.

The initial level of payment specified by the investment-linked annuity is set based on the retiree's life expectancy at the time the annuity is purchased. The investment-linked annuity provider guarantees the longevity risk (i.e., to ensure the retiree's payments continue for life) but not the investment risk (the price of units will vary in line with underlying investment performance). This means that the retiree's income will move up and down over time based on the investment fund unit price at the time of each payment.

Arizona to Australia: How Far Is It?

You may want to see also

Explore related products

![]()

Annuities and tax

Annuities are a form of retirement income product, providing a stream of income in your retirement years. They are typically purchased from a life insurance provider or a super fund. Annuities can be structured to return your investment earnings at the end of the agreed term, in regular payments over the agreed term or your life, or a combination of these.

In Australia, the tax treatment of annuities depends on the age at which they are purchased and the source of the funds. If you buy an annuity with super money, any money you receive from it is tax-free from the age of 60. If you are between 55 and 59, any annuity payment may have a taxable and non-taxable component.

For annuities purchased with non-super money, only the income component is taxable, not any return of capital. The tax table you use depends on the period over which the annuity is paid, e.g. weekly or fortnightly. The Australian Taxation Office provides resources to help calculate the withholding amount for an annuity payment purchased with non-super money.

When you buy an annuity, you can nominate a beneficiary, known as the "reversionary beneficiary", who will receive your income payments for the rest of their life, usually at a reduced level. Alternatively, you can choose a guaranteed period option, where a minimum payment period is set. If you die within this period, your beneficiary will receive your payments as a lump sum or income stream without any reductions.

An Easy Guide to Legally Changing Your Last Name in Australia

You may want to see also

Explore related products

![]()

How to buy an annuity

Annuities are a form of retirement income product that provides a stream of income in your retirement years, similar to an account-based pension. Unlike an account-based pension, annuities generally pay a fixed amount at set intervals. This can be useful if you want to ensure a steady income for everyday costs throughout your retirement.

Annuities are typically purchased from a life insurance provider or a super fund, and they are designed to provide income payments that can be made monthly, quarterly, half-yearly, or yearly. When buying an annuity, you can choose the payment frequency and whether you want the payments to last for a fixed term or your lifetime.

- Consult a financial advisor: Before purchasing an annuity, it is essential to seek independent financial advice to ensure that it is the best option for your circumstances. A financial advisor can help you understand the different types of annuities available and how they fit into your overall retirement plan.

- Assess your financial needs: Consider your income requirements during retirement. Do you need a guaranteed income stream to cover your basic expenses? Are you comfortable with the level of risk associated with market-linked investments, or do you prefer the stability of a fixed income?

- Choose the type of annuity: There are two main types of annuities: conventional annuities and investment-linked annuities. Conventional annuities provide guaranteed income payments that are not affected by market performance. On the other hand, investment-linked annuities offer the potential for higher returns but link your income payments to the performance of underlying investments.

- Decide on the payment structure: You can choose how often you receive payments (monthly, quarterly, half-yearly, or yearly). Additionally, consider whether you want your annuity to increase each year in line with inflation or by a fixed percentage.

- Select a reputable provider: Research and compare different annuity providers in the market. Consider their reputation and financial stability and the specific terms and conditions of their annuity products.

- Understand the costs and risks: Annuities typically have fees and charges associated with them, so make sure you understand all the costs involved. Additionally, be aware of the risks, including the possibility of early withdrawal penalties and the impact of inflation on your purchasing power over time.

- Finalise the purchase: Once you have selected a provider and annuity type, work with the provider to finalise the purchase. This will involve agreeing on the payment terms, including the payment amount and frequency. You will also need to provide the lump sum payment to purchase the annuity.

Remember, purchasing an annuity is a significant financial decision, and it is important to carefully consider your options before committing. It is always recommended to seek professional financial advice to ensure that an annuity is suitable for your retirement planning needs.

Grow Your Own Mushrooms at Home: An Australian Guide

You may want to see also

Frequently asked questions

An annuity is a form of retirement income product that provides a stream of income in your retirement years, similar to an account-based pension. Annuities are offered by superannuation and insurance companies.

With an annuity, you provide an upfront investment of cash and then receive a guaranteed, regular income for a fixed period of time or until you die. The payment you receive is locked in when you purchase the annuity and remains the same regardless of what happens with investment returns.

Annuities can be a good investment in Australia for those looking for income security. However, they are not for everyone and may be poor value for people with lower levels of wealth or those who are not in good health. Less than 4% of retired Australians invest in annuities, while more than 80% use account-based pensions.

Annuities provide a guaranteed income, regardless of how investment markets are performing. This can give retirees peace of mind and help them plan their retirement.

Annuities are not designed to be flexible, and it may be hard to take your money out as a lump sum if you need it. Your money is typically 'locked in' to the annuity until it ends. Annuities may also provide lower income payments than other investments, especially if purchased in a period with low-interest rates.